USO invests primarily in futures contracts for light, sweet crude oil, other types of crude oil, heating oil, gasoline, natural gas and other petroleum-based fuels that are traded on the NYMEX, ICE Futures or other U.S. and foreign exchanges (collectively, “Oil Futures Contracts”) and to a lesser extent, in order to comply with regulatory requirements, risk mitigation measures (including those that may be taken by USO, USO’s FCMs, counterparties or other market participants), liquidity requirements, or in view of market conditions, other oil-related investments such as cash-settled options on Oil Futures Contracts, forward contracts for oil, cleared swap contracts and OTC swaps that are based on the price of oil, other petroleum-based fuels, Oil Futures Contracts and indices based on the foregoing (collectively, “Other Oil-Related Investments”). For convenience and unless otherwise specified, Oil Futures Contracts and Other Oil-Related Investments collectively are referred to as “Oil Interests” in this quarterly report on Form 10-Q.

USO’s investment objective is not for its NAV or market price of shares to equal, in dollar terms, the spot price of light, sweet crude oil or any particular futures contract based on light, sweet crude oil, nor is USO’s investment objective for the percentage change in its NAV to reflect the percentage change of the price of any particular futures contract as measured over a time period greater than one day. The general partner of USO, United States Commodity Funds, LLC (“USCF”), believes that it is not practical to manage the portfolio to achieve such an investment goal when investing in Oil Futures Contracts and Other Oil-Related Investments.

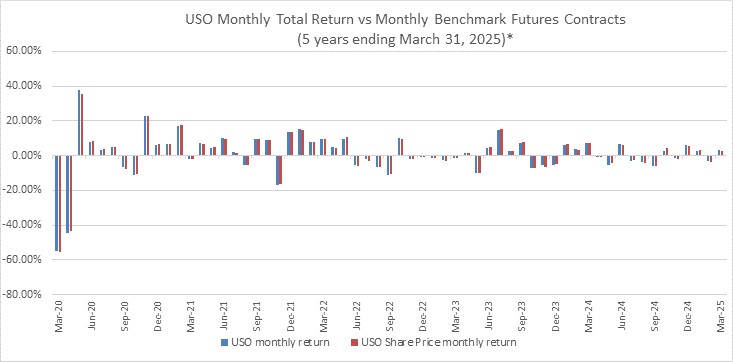

In addition, USCF believes that market arbitrage opportunities will cause daily changes in USO’s share price on the NYSE Arca on a percentage basis to closely track daily changes in USO’s per share NAV. USCF further believes that the daily changes in the price of the Benchmark Oil Futures Contract have historically closely tracked the daily changes in spot prices of light, sweet crude oil. USCF believes that the net effect of these relationships will be that the daily changes in the price of USO’s shares on the NYSE Arca on a percentage basis will closely track the daily changes in the spot price of a barrel of light, sweet crude oil on a percentage basis, plus interest earned on USO’s collateral holdings, less USO’s expenses.

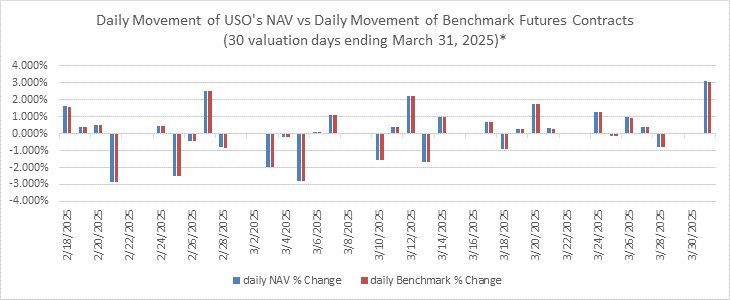

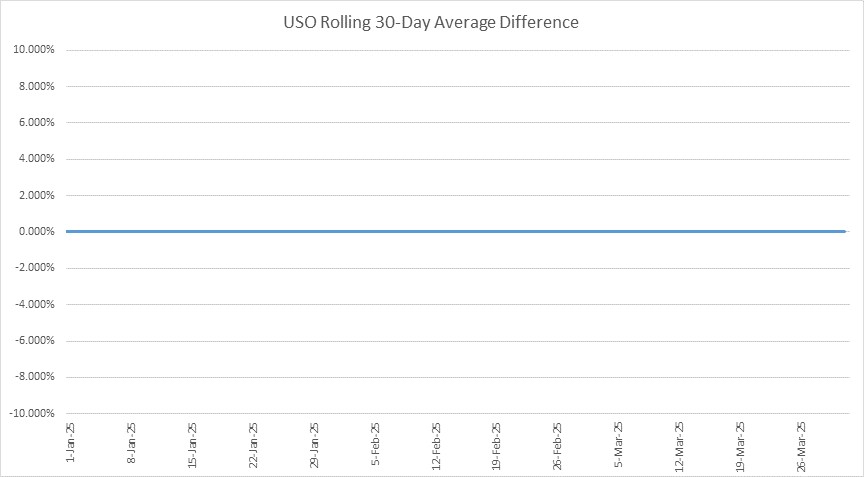

The following chart shows, for the period ending March 31, 2025, the rolling 30-day average difference between USO’s NAV and the Benchmark Oil Futures Contract. This is measured by subtracting the return of the Benchmark Oil Futures Contract from the return on USO’s NAV for each of the last thirty business days, and then averaging those thirty differences. The calculation is repeated daily.

*PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

22