UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

☒

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended March 31, 2025

☐

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ____________ to _____________

Commission file number 001-37568

| |

PDS Biotechnology Corporation

|

|

| |

(Exact name of registrant as specified in its charter)

|

|

|

Delaware

|

|

26-4231384

|

|

(State or other jurisdiction of incorporation or organization)

|

|

(IRS Employer Identification No.)

|

| |

303A College Road East, Princeton, NJ 08540

|

|

| |

(Address of principal executive offices)

|

|

| |

(800) 208-3343

|

|

| |

(Registrant’s telephone number)

|

|

| |

|

|

| |

(Former name, former address and former fiscal year, if changed since last report)

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

|

Trading symbol(s)

|

|

Name of each exchange on which registered

|

|

Common Stock, par value $0.00033 per share

|

|

PDSB

|

|

The Nasdaq Stock Market LLC

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section

232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes

☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth

company. See the definitions of “large accelerated filer”, “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

Non-accelerated filer ☒

|

Smaller Reporting Company ☒

|

|

Emerging growth company ☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares of the registrant’s Common Stock, par value $0.00033 per share, outstanding as of May 7, 2025 was 45,710,000.

PDS BIOTECHNOLOGY CORPORATION

FORM 10-Q FOR THE QUARTER ENDED March 31, 2025

| |

|

|

Page

|

|

Part I — Financial Information

|

|

| |

|

|

|

| |

Item 1.

|

Financial Statements (Unaudited):

|

|

| |

|

|

|

| |

|

|

3

|

| |

|

|

|

| |

|

|

4

|

| |

|

|

|

| |

|

|

5

|

| |

|

|

|

| |

|

|

6

|

| |

|

|

|

| |

|

|

7

|

| |

|

|

|

| |

Item 2.

|

|

17

|

| |

|

|

|

| |

Item 3.

|

|

31

|

| |

|

|

|

| |

Item 4.

|

|

31

|

| |

|

|

|

|

Part II — Other Information

|

32

|

| |

|

|

|

| |

Item 1.

|

|

|

| |

|

|

|

| |

Item 1A.

|

|

32

|

| |

|

|

|

| |

Item 2.

|

|

32

|

| |

|

|

|

| |

Item 3.

|

|

32

|

| |

|

|

|

| |

Item 4.

|

|

32

|

| |

|

|

|

| |

Item 5.

|

|

32

|

| |

|

|

|

| |

Item 6.

|

|

33

|

| |

|

|

|

|

|

33

|

|

|

34

|

|

PART 1.

|

FINANCIAL INFORMATION

|

|

ITEM 1.

|

FINANCIAL STATEMENTS

|

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARY

Condensed Consolidated

Balance Sheets

|

|

March 31, 2025

|

|

|

December 31, 2024

|

|

|

ASSETS

|

|

(unaudited)

|

|

|

|

|

|

Current assets:

|

|

|

|

|

|

|

Cash and cash equivalents

|

|

$

|

39,978,674

|

|

|

$

|

41,689,591

|

|

|

Prepaid expenses and other assets

|

|

|

2,489,965

|

|

|

|

3,364,852

|

|

|

Total current assets

|

|

|

42,468,639

|

|

|

|

45,054,443

|

|

| |

|

|

|

|

|

|

|

|

|

Noncurrent assets:

|

|

|

|

|

|

|

|

|

|

Prepaid expenses

|

|

|

4,270,818 |

|

|

|

– |

|

|

Property and equipment, net

|

|

|

136,561

|

|

|

|

142,020

|

|

Financing lease right-to-use assets

|

|

|

152,524 |

|

|

|

162,194 |

|

| |

|

|

|

|

|

|

|

|

|

Total assets

|

|

$

|

47,028,542

|

|

|

$

|

45,358,657

|

|

| |

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS’ EQUITY

|

|

|

|

|

|

|

|

|

|

Current liabilities:

|

|

|

|

|

|

|

|

|

|

Accounts payable

|

|

$

|

2,859,292

|

|

|

$

|

1,684,868

|

|

|

Accrued expenses

|

|

|

2,846,497

|

|

|

|

2,841,214

|

|

|

Note payable - short term

|

|

|

12,500,000 |

|

|

|

12,500,000 |

|

|

Financing lease obligation-short term

|

|

|

59,556

|

|

|

|

61,119

|

|

|

Total current liabilities

|

|

|

18,265,345

|

|

|

|

17,087,201

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note payable, net of debt discount

|

|

|

6,352,333 |

|

|

|

9,204,755 |

|

|

Financing lease obligation-long term

|

|

|

48,655 |

|

|

|

61,853 |

|

|

|

|

$

|

24,666,333

|

|

|

$

|

26,353,809

|

|

| |

|

|

|

|

|

|

|

|

|

Commitments and contingencies (Note 9)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STOCKHOLDERS’ EQUITY

|

|

|

|

|

|

|

|

|

|

Common stock, $0.00033

par value, 150,000,000 shares authorized at March 31, 2025 and December 31, 2024, respectively; 45,445,851

and 37,987,380 issued and outstanding at March 31, 2025 and December 31, 2024, respectively

|

|

|

14,998

|

|

|

|

12,536

|

|

|

Additional paid-in capital

|

|

|

212,947,177

|

|

|

|

201,103,311

|

|

|

Accumulated deficit

|

|

|

(190,599,966

|

)

|

|

|

(182,110,999

|

)

|

|

Total stockholders’ equity

|

|

|

22,362,209

|

|

|

|

19,004,848

|

|

|

|

|

|

|

|

|

|

|

|

Total liabilities and stockholders’ equity

|

|

$

|

47,028,542

|

|

|

$

|

45,358,657

|

|

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARY

Condensed Consolidated

Statements of Operations and Comprehensive Loss

(Unaudited)

| |

|

Three Months Ended March 31,

|

|

| |

|

2025

|

|

|

2024

|

|

|

Operating expenses:

|

|

|

|

|

|

|

Research and development expenses

|

|

$

|

5,830,999

|

|

|

$

|

6,704,164

|

|

|

General and administrative expenses

|

|

|

3,274,759 |

|

|

|

3,393,463

|

|

|

Total operating expenses

|

|

|

9,105,758

|

|

|

|

10,097,627 |

|

| |

|

|

|

|

|

|

|

|

|

Loss from operations

|

|

|

(9,105,758 |

) |

|

|

(10,097,627 |

) |

| |

|

|

|

|

|

|

|

|

|

Interest income (expenses), net

|

|

|

|

|

|

|

|

|

|

Interest income

|

|

|

377,849 |

|

|

|

668,895 |

|

|

Interest expense

|

|

|

(930,878 |

) |

|

|

(1,174,745 |

) |

|

Interest income (expenses), net

|

|

|

(553,029 |

) |

|

|

(505,850

|

)

|

| |

|

|

|

|

|

|

|

|

Loss before income taxes

|

|

|

(9,658,787 |

) |

|

|

(10,603,477 |

) |

Benefit for income taxes

|

|

|

1,169,820 |

|

|

|

- |

|

|

Net loss and comprehensive loss

|

|

|

(8,488,967

|

)

|

|

|

(10,603,477 |

) |

| |

|

|

|

|

|

|

|

|

|

Per share information:

|

|

|

|

|

|

|

|

|

|

Net loss per share, basic and diluted

|

|

$ |

(0.21 |

) |

|

$ |

(0.30 |

) |

| |

|

|

|

|

|

|

|

|

|

Weighted average common shares outstanding, basic, and diluted

|

|

|

40,521,001 |

|

|

|

34,815,870 |

|

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARY

Condensed Consolidated

Statements of Changes in

Stockholders’ Equity

(Unaudited)

| |

|

Common Stock

|

|

|

|

|

|

|

|

|

|

|

| |

|

Shares

Issued

|

|

|

Amount

|

|

|

Additional

Paid-in

Capital

|

|

|

Accumulated

Deficit

|

|

|

Total

Equity

|

|

|

January 1, 2024

|

|

|

33,094,521

|

|

|

$

|

10,921

|

|

|

$

|

170,620,641

|

|

|

$

|

(144,500,615

|

)

|

|

$

|

26,130,947

|

|

|

Stock-based compensation expense

|

|

|

–

|

|

|

|

–

|

|

|

|

1,630,011

|

|

|

|

–

|

|

|

|

1,630,011

|

|

|

Issuances of common

stock from the Sales Agreement, net

|

|

|

3,428,681

|

|

|

|

1,131

|

|

|

|

19,493,342

|

|

|

|

–

|

|

|

|

19,494,473

|

|

|

Issuances of common stock, from exercise of stock options

|

|

|

156,073 |

|

|

|

52 |

|

|

|

531,039 |

|

|

|

– |

|

|

|

531,091

|

|

|

Net loss

|

|

|

–

|

|

|

|

–

|

|

|

|

–

|

|

|

|

(10,603,477

|

)

|

|

|

(10,603,477

|

)

|

|

Balance - March 31, 2024

|

|

|

36,679,275

|

|

|

$

|

12,104

|

|

|

$

|

192,275,033

|

|

|

$

|

(155,104,092

|

)

|

|

$

|

37,183,045

|

|

| |

|

Common Stock

|

|

|

|

|

|

|

|

|

|

|

| |

|

Shares

Issued

|

|

|

Amount

|

|

|

Additional

Paid-in

Capital

|

|

|

Accumulated

Deficit

|

|

|

Total

Equity

|

|

|

January 1, 2025

|

|

|

37,987,380

|

|

|

$

|

12,536

|

|

|

$

|

201,103,311

|

|

|

$

|

(182,110,999

|

)

|

|

$

|

19,004,848

|

|

|

Stock-based compensation expense

|

|

|

–

|

|

|

|

–

|

|

|

|

1,253,882

|

|

|

|

–

|

|

|

|

1,253,882

|

|

|

Issuance of common stock for consulting agreement

|

|

|

150,000 |

|

|

|

50 |

|

|

|

203,451 |

|

|

|

– |

|

|

|

203,501 |

|

|

Issuances of common

stock from the Sales Agreement, net

|

|

|

205,350 |

|

|

|

68 |

|

|

|

306,047 |

|

|

|

– |

|

|

|

306,115 |

|

Issuances of common stock, net of issuance costs

|

|

|

6,396,787 |

|

|

|

2,111 |

|

|

|

6,919,908 |

|

|

|

– |

|

|

|

6,922,019 |

|

|

Issuance of pre-funded warrants

|

|

|

– |

|

|

|

– |

|

|

|

1,009,969 |

|

|

|

– |

|

|

|

1,009,969 |

|

| Issuance of warrants |

|

|

– |

|

|

|

– |

|

|

|

2,150,771 |

|

|

|

– |

|

|

|

2,150,771 |

|

|

Exercise of pre-funded warrants

|

|

|

706,334 |

|

|

|

233 |

|

|

|

(162 |

) |

|

|

– |

|

|

|

71

|

|

|

Net loss

|

|

|

–

|

|

|

|

–

|

|

|

|

–

|

|

|

|

|

|

|

|

|

|

|

Balance - March 31, 2025

|

|

|

45,445,851

|

|

|

$

|

14,998

|

|

|

|

|

|

|

$

|

(190,599,966

|

)

|

|

|

|

|

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARY

Condensed Consolidated Statements

of

Cash Flows

(Unaudited)

| |

|

Three Months Ended March 31,

|

|

| |

|

2025

|

|

|

2024

|

|

|

Cash flows from operating activities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$

|

(10,603,477

|

)

|

|

Adjustments to reconcile net loss to net cash used in operating activities:

|

|

|

|

|

|

|

|

|

|

Stock-based compensation expense

|

|

|

1,253,882

|

|

|

|

1,630,011

|

|

Issuance of shares in consulting agreements

|

|

|

203,501 |

|

|

|

– |

|

Amortization of debt discount

|

|

|

272,578 |

|

|

|

270,236 |

|

|

Depreciation expense

|

|

|

|

|

|

|

4,735

|

|

|

Finance lease depreciation expense

|

|

|

9,670 |

|

|

|

9,670 |

|

|

Changes in assets and liabilities:

|

|

|

|

|

|

|

|

|

|

Prepaid expenses and other assets

|

|

|

(3,395,931

|

)

|

|

|

443,210

|

|

|

|

|

|

|

|

|

|

(981,993

|

)

|

|

Accrued expenses

|

|

|

(66,872

|

)

|

|

|

(710,581

|

)

|

|

Net cash used in operating activities

|

|

|

|

|

|

|

(9,938,189

|

)

|

|

|

|

|

|

|

|

|

|

| Cash flows from financing activities: |

|

|

|

|

|

|

|

|

|

Proceeds from pre-funded warrants

|

|

|

1,009,969 |

|

|

|

– |

|

|

Proceeds from exercise of pre-funded warrants

|

|

|

71 |

|

|

|

– |

|

| Proceeds from warrants |

|

|

2,150,771 |

|

|

|

– |

|

|

Proceeds from exercise of stock options

|

|

|

– |

|

|

|

531,091 |

|

|

Payments of finance lease obligations

|

|

|

(14,761

|

)

|

|

|

(13,475 |

) |

|

Loan principal repayment

|

|

|

(3,125,000 |

) |

|

|

– |

|

|

Proceeds from issuance of common stock from the Sales Agreement, net

|

|

|

306,115 |

|

|

|

19,494,473 |

|

|

Proceeds from issuance of common stock, net of issuance costs

|

|

|

6,994,174 |

|

|

|

– |

|

|

Net cash provided by financing activities

|

|

|

7,321,339 |

|

|

|

20,012,089

|

|

|

|

|

|

|

|

|

|

|

|

Net increase in cash and cash equivalents

|

|

|

|

|

|

|

10,073,900

|

|

|

Cash and cash equivalents at beginning of period

|

|

|

41,689,591

|

|

|

|

56,560,517

|

|

| |

|

|

|

|

|

|

|

|

| Cash and cash equivalents at the end of period |

|

$ |

39,978,674 |

|

|

$ |

66,634,417 |

|

|

|

|

|

|

|

|

|

|

Supplemental information of cash and non-cash transactions:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$

|

693,989

|

|

|

$

|

1,174,745

|

|

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARY

Notes to Condensed Consolidated Financial Statements (Unaudited)

Note 1 – Nature of Operations

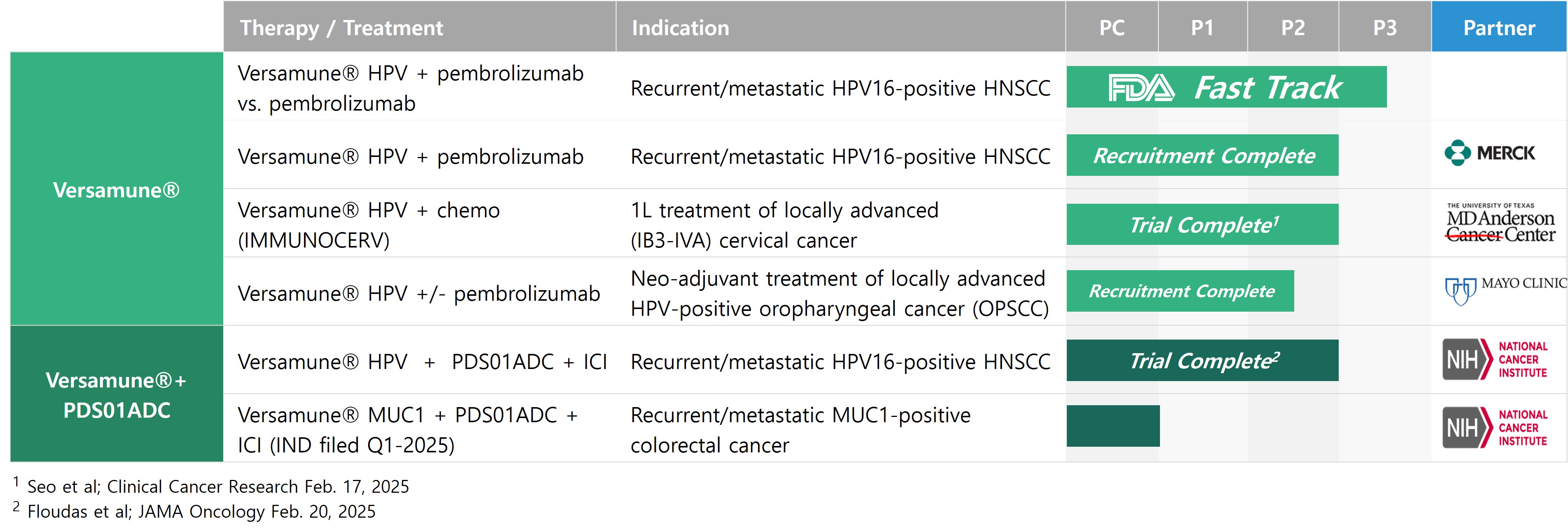

PDS Biotechnology Corporation, a Delaware

corporation (the “Company” or “PDS Biotech”), is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted immunotherapies designed to overcome the limitations of current immunotherapy and

vaccine technologies. The Company develops proprietary platforms designed to train and enable the immune system to attack and destroy disease; Versamune®, and Versamune® in combination with PDS01ADC for treatments in

oncology and Infectimune® for treatments in infectious diseases. When paired with an antigen, which is a disease-related protein that is recognizable by the immune system, Versamune® and Infectimune® have both been shown to

induce, in vivo, large quantities of high-quality, highly

potent polyfunctional CD4 helper and CD8 killer T cells, a specific sub-type of T cell that is more effective at killing infected or target cells. PDS01ADC is a novel investigational tumor-targeting fusion protein of

Interleukin 12 that enhances the proliferation, potency, infiltration and longevity of T cells in the tumor microenvironment and is therefore designed to overcome the limitations of cytokine therapy which today has resulted

in high toxicity and limited therapeutic potential. Infectimune® is also designed to promote the induction of disease-specific neutralizing antibodies. The Company’s immuno-oncology product candidates are of potential

interest for use as a component of combination product candidates (for example, in combination with other therapies such as immune checkpoint inhibitors) to provide more effective treatments across a range of advanced and/or

refractory cancers. The Company is also evaluating its immunotherapies as monotherapies in early-stage disease. The Company is developing targeted product candidates to treat several cancers, including Human Papillomavirus

(HPV) associated cancers, melanoma, colorectal, lung, breast and prostate cancers. The Company’s infectious disease candidate is of potential interest for use in universal influenza vaccines.

Note 2 – Summary of Significant Accounting

Policies

| (A) |

Unaudited interim financial statements:

|

The unaudited financial

statements for all periods presented are referred to as “Condensed Consolidated Financial Statements”, and have been prepared by the Company in United States (“U.S.”) dollars and in accordance with U.S. generally accepted accounting

principles (“U.S. GAAP”) for interim financial reporting and pursuant to the rules and regulations for reporting on Form 10-Q, which do not conform in all respects to the requirements of U.S. GAAP for annual financial statements.

Accordingly, certain information and disclosures required by U.S. GAAP for complete Consolidated Financial Statements are not included herein. Accordingly, these notes to the unaudited Condensed Consolidated Financial Statements should be

read in conjunction with the audited consolidated financial statements prepared in accordance with U.S. GAAP that are contained in the Company’s Annual Report on Form 10-K for the year ended December 31, 2024, filed with the U.S. Securities

and Exchange Commission (“SEC”) on March 27, 2025. The unaudited Condensed Consolidated Financial Statements have been prepared using accounting policies that are consistent with the policies used in preparing the Company’s audited

consolidated financial statements for the year ended December 31, 2024. The unaudited Condensed Consolidated Financial Statements reflect all normal and recurring adjustments necessary for a fair statement of the Company’s financial position and results of

operations for the interim periods. The operating results for the interim periods presented are not necessarily indicative of the results expected for the full year or for any other subsequent interim period.

The preparation of the Condensed Consolidated Financial

Statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the reported amounts of expenses at the date of the Condensed Consolidated Financial

Statements and during the reporting periods, and to disclose contingent assets and liabilities at the date of the Condensed Consolidated Financial Statements. Actual results could differ from those estimates. The most significant estimate

relates to the fair value of securities underlying stock-based compensation.

| (C) |

Significant risks and uncertainties:

|

The Company’s operations are subject to a number of factors that may affect its operating results and

financial condition. Such factors include, but are not limited to: the Company’s ability to complete clinical trials necessary to obtain regulatory product licenses, the regulatory approvals needed to pursue development

of its clinical and product candidates, the Company’s adherence to covenants under its debt agreement, the Company’s ability to preserve its cash resources, the Company’s ability to add clinical and product

candidates to its pipeline, the Company’s ability to protect its intellectual property, competition from products manufactured and sold or being developed by other companies, the price of, and demand for, Company products if

approved for sale, the Company’s ability to negotiate favorable licensing or other manufacturing and marketing agreements for its products, and the Company’s ability to raise capital.

The Company currently has no commercially approved

products. As such, there can be no assurance that the Company’s future research and development programs will be successfully commercialized. Developing and commercializing a product requires significant time and capital and is subject to

regulatory review and approval as well as competition from other biotechnology and pharmaceutical companies. The Company operates in an environment of rapid change and is dependent upon the continued services of its employees, consultants and

key vendors, and obtaining and protecting its intellectual property.

| (D) |

Cash equivalents and concentration of cash balance:

|

The Company considers all highly liquid securities with a

maturity of less than three months to be cash equivalents. The Company’s cash and cash equivalents in bank deposit accounts, at times, may exceed federally insured limits.

| (E) |

Research and development:

|

Costs incurred in connection with research and development

activities are expensed as incurred. These costs include licensing fees to use certain technology in the Company’s research and development projects as well as fees paid to consultants and vendors that perform certain research activities and

testing on behalf of the Company.

Costs for certain development activities, such as clinical

trials, are recognized based on an evaluation of the progress to completion of specific tasks using data, such as patient enrollment, clinical site activations or information provided by vendors about their actual costs incurred. Payments for

these activities are based on the terms of the individual arrangements, which may differ from the timing and pattern of costs incurred.

The Company expenses patent costs as incurred and

classifies such costs as general and administrative expenses in the accompanying Condensed Consolidated Statements of Operations and Comprehensive Loss.

| (G) |

Stock-based compensation:

|

The Company accounts for its stock-based compensation in accordance with ASC Topic 718, Compensation—Stock Compensation

(“ASC 718”). ASC 718 requires all stock-based payments to employees, directors and non-employees to be recognized as expense in the Condensed Consolidated Statements of Operations and Comprehensive Loss based on their grant date fair values.

In order to determine the fair value of stock options on the date of grant, the Company uses the Black-Scholes option-pricing model. Inherent in this model are assumptions related to expected stock-price volatility, option term, risk-free

interest rate and dividend yield. While the risk-free

interest rate and dividend yield are less subjective assumptions that are based on factual data derived from public sources, the expected stock-price volatility and option term assumptions require a greater level of judgment. The

Company expenses the fair value of its stock-based compensation awards to employees and directors on a straight-line basis over the requisite service period, which is generally the vesting period. The Company recognizes stock-based

compensation award forfeitures as they occur.

| (H) |

Net loss per common share:

|

Basic and diluted net loss per common share is determined

by dividing net loss attributable to common stockholders by the weighted average common shares outstanding during the period. For all periods presented, the common shares underlying the stock options and warrants have been excluded from the

calculation because their effect would be antidilutive. Therefore, the weighted average shares outstanding used to calculate both basic and diluted loss per common share is the same.

The potentially dilutive securities excluded from the

determination of diluted loss per share as their effect is antidilutive, are as follows:

|

|

As of March 31,

|

|

| |

|

2025

|

|

|

2024

|

|

|

Stock options to purchase Common Stock

|

|

|

5,347,904

|

|

|

|

5,314,661

|

|

|

Warrants to purchase Common Stock

|

|

|

7,984,034

|

|

|

|

466,112

|

|

|

Total

|

|

|

13,331,938

|

|

|

|

5,780,773

|

|

The Company makes provision for deferred income taxes under the asset and liability method, which requires deferred tax

assets and liabilities to be recognized for the future tax consequences attributable to net operating loss carryforwards and for differences between the financial statement carrying amounts and the respective tax bases of assets and

liabilities. Deferred tax assets are reduced, if necessary, by a valuation allowance if it is more likely than not that some portion or all of the deferred tax assets will not be realized.

|

(J)

|

Fair value of financial instruments:

|

FASB ASC 820, Fair Value Measurement, specifies a hierarchy of valuation techniques based on whether the inputs

to those valuation techniques are observable or unobservable. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect market assumptions. The hierarchy gives the highest priority to

unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurement) and the lowest priority to unobservable inputs (Level 3 measurement).

The three levels of the fair value hierarchy are as follows:

|

● |

Level 1 — Unadjusted quoted prices in active markets for identical assets or liabilities that the reporting entity has the ability to access at the

measurement date. Level 1 primarily consists of financial instruments whose value is based on quoted market prices such as exchange-traded instruments and listed equities.

|

|

● |

Level 2 — Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly (e.g.,

quoted prices of similar assets or liabilities in active markets, or quoted prices for identical or similar assets or liabilities in markets that are not active). Level 2 includes financial instruments that are valued using models

or other valuation methodologies.

|

|

● |

Level 3 — Unobservable inputs for the asset or liability. Financial instruments are considered Level 3 when their fair values are determined using

pricing models, discounted cash flows or similar techniques and at least one significant model assumption or input is unobservable.

|

The Company determines if an arrangement is a lease at inception and recognizes the lease in accordance with ASC 842, Leases (“ASC 842”). Both financing and operating leases are included in right-of-use (“ROU”) assets, lease

obligation-short term and lease obligation-long term in the Company’s Condensed Consolidated Balance Sheets. ROU assets represent the right to use an underlying asset for the lease term and lease liabilities represent the Company’s

obligation to make lease payments arising from the lease. The ROU assets and lease liabilities are recognized at the lease commencement date based on the present value of the lease payments over the lease term. The Company determines the

portion of the lease liability that is current as the difference between the calculated lease liability at the end of the current period and the lease liability that is projected 12 months from the current period.

|

(L)

|

New accounting standards:

|

Recently Adopted Accounting Pronouncements

In November 2023, the FASB issued ASU 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures, which improves the disclosures

required for reportable segments in the Company’s annual and interim financial statements, primarily through enhanced disclosures about significant segment expenses. ASU 2023-07 is effective for annual periods beginning after

December 15, 2023 and interim periods within fiscal years beginning after December 15, 2024. The Company adopted this ASU for the annual period ended December 31, 2024 and the amendments have been applied retrospectively to

all prior periods presented in these Condensed Consolidated Financial Statements by expanding the disclosure of expenses included in segment measures of profitability. Refer to the Company’s segment disclosure in Note 12 –

Segment Reporting for more information.

Recent Accounting

Pronouncements Not Yet Adopted

In December 2023,

the FASB issued ASU 2023-09, Improvements to Income Tax Disclosures, which requires public entities, on an annual basis, to provide disclosures of specific categories in the rate

reconciliation, additional information for reconciling items that meet a quantitative threshold and income taxes paid disaggregated by jurisdiction. ASU 2023-09 is effective for annual periods beginning after December 15,

2024. The Company has evaluated the impact of adopting this standard and does not believe it will have a material impact on the consolidated financial statements and disclosures.

In November 2024, the FASB issued ASU No. 2024-03, Income Statement - Reporting Comprehensive Income - Expense Disaggregation Disclosures (Subtopic 220-40): Disaggregation of Income Statement Expenses. The new guidance requires a public

business entity to provide disaggregated disclosures, in the notes to the financial statements, of certain categories of expenses that are included in expense line items on the face of the Statement of Operations and

Comprehensive Loss. The amendments in this Update are effective for annual reporting periods beginning after December 15, 2026, and interim reporting periods beginning after December 15, 2027. Early adoption is permitted. The

Company is currently evaluating the impact that the new guidance will have on the Company’s consolidated financial statements.

Note 3 – Liquidity and Capital Resources

As of March 31, 2025, the

Company had $40.0 million in cash and cash equivalents. The Company’s primary use of cash is to fund operating expenses, primarily

research and development expenditures. Cash used to fund operating expenses is impacted by the level of activities undertaken, as well as the timing of when the Company pays these expenses, as reflected in the change to the Company’s outstanding accounts payable and

accrued expenses. Since inception, the Company has experienced net losses and negative cash flows from operations each fiscal year. The Company has no revenues and expects to continue to incur operating losses for the foreseeable future and may never become profitable.

The Company funds its operations through equity and/or debt financings such as the following:

In August 2022, the Company filed a shelf registration statement, or the 2022 Shelf Registration Statement, with the SEC

for the issuance of common stock, preferred stock, warrants, rights, debt securities, and units, up to an aggregate amount of $150

million, approximately $97 million of which covers the offer, issuance and sale by the Company of its common stock under the Sales

Agreement and the New Sales Agreement (as discussed below). The 2022 Shelf Registration Statement was declared effective on September 2, 2022.

In August 2022, the Company entered into an At Market Issuance Sales Agreement, or the Sales Agreement, with B. Riley

Securities, Inc. and BTIG, LLC, each an Agent and collectively the Agents, with respect to an at-the-market offering program under which the Company may offer and sell, from time to time at its sole discretion, shares of its common stock,

having an aggregate offering price of up to $50 million, or the Placement Shares, through or to the Agents, as sales agents or

principals. Upon delivery of a placement notice and subject to the terms and conditions of the Sales Agreement, the Agents may sell the Placement Shares by any method permitted by law deemed to be an “at the market” offering as defined in

Rule 415 of the Securities Act of 1933, as amended, including, without limitation, sales made through The Nasdaq Capital Market or on any other existing trading market for the Company’s common stock. The Agents will use commercially

reasonable efforts to sell the Placement Shares from time to time, based upon the Company’s instructions (including any price, time or size limits or other customary parameters or conditions the Company may impose). The Company will pay the

Agents a commission equal to three percent (3%) of the gross sales proceeds of any Placement Shares sold through the Agents under

the Sales Agreement, and the Company has also provided the Agents with customary indemnification and contribution rights. The Company is not obligated to make any sales of its common stock under the Sales Agreement. The offering of

Placement Shares pursuant to the Sales Agreement will terminate upon the earlier of (i) the sale of all Placement Shares subject to the Sales Agreement or (ii) termination of the Sales Agreement in accordance with its terms. In August 2024,

the Company entered into an Amended and Restated At Market Issuance Sales Agreement, or the New Sales Agreement, with B. Riley Securities, Inc. and H.C. Wainwright & Co., LLC, with terms that are substantially consistent with those

included in the original Sales Agreement. The New Sales Agreement superseded and replaced the Sales Agreement. For the year ended December 31, 2024, the Company sold 3,428,681 shares of common stock for a net value of $19.5

million pursuant to the Sales Agreement and 1,108,105 shares of common stock for a net value of $3.2 million pursuant to the New Sales Agreement. During the three months ended March 31, 2025, the Company sold 205,350 shares of common stock for a net value of $0.3

million pursuant to the New Sales Agreement and during the three months ended March 31, 2024, the Company sold 3,428,681 shares

of common stock for a net value of $19.5 million, pursuant to the Sales Agreement.

In August 2022, the Company entered into a venture loan and security agreement, or the Loan and Security Agreement, with

Horizon Technology Finance Corporation, as lender and collateral agent for itself and the other lenders. In total, the Company received $24.6

million in net proceeds under the Loan and Security Agreement. The Company’s indebtedness under the Loan and Security Agreement was satisfied in full and retired in full with a portion of the proceeds received from the Securities

Purchase Agreement, as discussed below.

In April 2024, the Company received approximately $0.9 million from the

net sale of tax benefits to an unrelated, profitable New Jersey corporation pursuant to its participation in the New Jersey Technology Business Tax Certificate Transfer NOL program for tax year 2022.

In January and February 2025, the Company received approximately $1.2 million from the net sale of

tax benefits to two unrelated, profitable New Jersey corporations pursuant to its participation in the New Jersey

Technology Business Tax Certificate Transfer NOL program for tax year 2023.

In February 2025, the Company entered into a Securities Purchase Agreement with certain purchasers, pursuant to which the Company agreed to sell

an aggregate of 6,396,787 shares of common stock, pre-funded warrants to purchase up to an aggregate of 933,334 shares of common stock, and common stock warrants to purchase up to an aggregate of 7,330,121 shares of common stock at a combined purchase price of $1.50

per share and warrant (the “February 2025 Offering”). Two of the Company’s directors participated in the February 2025

Offering and purchased 30,121 shares of common stock in the aggregate at an offering price per share of $1.66 and common stock warrants to purchase 30,121

shares of common stock. The common stock warrants issued to the Company’s directors have an exercise price per share of $1.53,

but are otherwise identical to the common stock warrants issued to all other participants in the February 2025 Offering. Aggregate gross proceeds from the February 2025 Offering were approximately $11 million. Net proceeds to the Company from the February 2025 Offering, after deducting the placement agent fees and other estimated

offering expenses payable by the Company, were approximately $10.05 million. The placement agent fees and offering expenses

were accounted for as a reduction of additional paid in capital. The February 2025 Offering closed on February 28, 2025.

On April 30, 2025, the Company entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with

certain third party lenders and JGB Collateral LLC, as collateral agent. Pursuant to the Securities Purchase Agreement, the Company agreed to sell (i) senior secured convertible debentures in an aggregate principal amount of $22,222,222 (collectively, the “Debentures”) and (ii) warrants to purchase up to 1,000,000 shares of common stock, for an exercise price of $2.52

per share (collectively, the “Warrants”), subject to adjustments as set forth in the Warrants, for a total purchase price of $20,000,000.

Approximately $19 million of the proceeds from the transactions contemplated by the Securities Purchase Agreement were used

to satisfy in full and retire the Company’s indebtedness under the Loan and Security Agreement.

Going Concern

The Company evaluated whether there are any conditions and events, considered in the aggregate, that raise substantial doubt about its

ability to continue as a going concern within one year after the filing of this Quarterly Report on Form 10-Q in accordance with ASC Subtopic 205-40, Going Concern. Since inception, the Company has experienced net losses and negative

cash flows from operations each fiscal year. The Company has no revenues and expects to continue to incur operating losses for the foreseeable future and may never become profitable. In addition, the Debentures allow for the lenders to

call the outstanding balance of the Debentures if the Company fails to maintain minimum cash balances outlined in the Debentures.

The Company’s estimated cash requirements in 2025 and beyond include expenses related to continuing development and clinical trials as

well as payments on its debt. The Company plans to execute its operating plan by obtaining additional capital, principally through issuance of equity through separate offerings or an at-the-market facility, issuance of debt, or by

entering into collaborations, strategic alliances, or license agreements with third parties. However, there is no assurance that sufficient additional capital and/or financing will be available to the Company, and even if available,

whether it will be on terms acceptable to the Company or its existing shareholders. The Company may also enter into government funding programs and consider selectively partnering for clinical development and commercialization. The sale

of additional equity would result in dilution to the Company’s stockholders. Incurring debt financing would result in debt service obligations, and the instruments governing such debt could provide for operating and financing covenants

that would restrict its operations. If the Company is unsuccessful in securing sufficient financing, it may need to delay, reduce, or eliminate its research and development programs, which could adversely affect its business prospects,

grant rights to third parties to develop and market immunotherapies that the Company would otherwise prefer to develop and market itself, or cease operations entirely. Any of these actions could harm its business, results of operations

and prospects. Failure to obtain adequate financing may also adversely affect the Company’s ability to operate as a going concern.

As a result of these uncertainties, the Company has concluded that substantial doubt exists about the Company’s ability to continue as a

going concern for a period of at least 12 months from the date of the issuance of these unaudited Condensed Consolidated Financial Statements on Form 10-Q. The unaudited Condensed Consolidated Financial Statements do not include any

adjustments to the carrying amounts and classifications of assets and liabilities that would result if the Company was unable to continue as a going concern.

Note 4 – Fair Value of Financial Instruments

There were no transfers between Levels 1, 2, or 3 during

the three months ended March 31, 2025 or 2024.

| |

|

Fair Value Measurements at Reporting Date Using

|

|

| |

|

Total

|

|

|

Quoted Prices in

Active Markets

(Level 1)

|

|

|

Quoted Prices in

Inactive Markets

(Level 2)

|

|

|

Significant

Unobservable Inputs

(Level 3)

|

|

|

As of March 31, 2025: (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents

|

|

$

|

39,978,674

|

|

|

$

|

39,978,674

|

|

|

$

|

–

|

|

|

$

|

–

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of December 31, 2024

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents

|

|

$

|

41,689,591

|

|

|

$

|

41,689,591

|

|

|

$

|

–

|

|

|

$

|

–

|

|

The carrying value of the Loan and Security Agreement approximated its fair value as of March 31, 2025 due to its variable interest rate.

Note 5 – Leases

The Company maintains a month-to-month lease for its research facilities at the Princeton Innovation Center BioLabs

located at 303A College Road E, Princeton NJ, 08540.

Financing Lease:

The Company has financed certain

laboratory equipment as follows:

| |

|

As of March 31,

|

|

| |

|

2025

|

|

|

2024

|

|

|

Cash paid for finance lease liabilities

|

|

$

|

17,463

|

|

|

$

|

17,463

|

|

Maturity of the Company’s financing lease liabilities is as follows:

|

Year ended December 31,

|

|

|

|

|

2025

|

|

$

|

52,387

|

|

|

2026

|

|

|

40,108

|

|

|

2027 and after

|

|

|

26,724

|

|

|

Total future minimum lease payments

|

|

|

119,219

|

|

|

Less imputed interest

|

|

|

(11,008

|

)

|

|

Remaining lease liability

|

|

$

|

108,211

|

|

The Company entered into four

financing leases for laboratory equipment with a total cost of $251,959 with four to five-year terms and a capitalized interest rate of

9.15%. Each of the lease agreements include a bargain purchase option to acquire the equipment at the end of the lease term. The

aggregate monthly payments are approximately $6,000.

Note 6 – Accrued Expenses

Accrued expenses consist of the following:

| |

|

As of

March 31, 2025

|

|

|

As of

December 31, 2024

|

|

Accrued research and development

|

|

$

|

1,283,288

|

|

|

$

|

1,267,627

|

|

|

Accrued professional fees

|

|

|

|

|

|

|

657,498

|

|

Accrued board compensation

|

|

|

87,625 |

|

|

|

– |

|

|

Accrued compensation

|

|

|

552,447

|

|

|

|

663,399

|

|

|

Accrued interest on debt

|

|

|

213,932 |

|

|

|

252,322 |

|

| Accrued rent |

|

|

368 |

|

|

|

368 |

|

|

Total

|

|

$

|

2,846,497

|

|

|

|

|

|

Note 7 – Stock-Based Compensation

In 2014, the Company’s stockholders approved the 2014 Equity Incentive Plan (the “Original Plan”) pursuant to which the Company may grant up to 91,367 shares as ISOs, NQs and restricted stock units (“RSUs”), subject to increases as hereafter described (the “Plan Limit”). In addition, on January 1, 2015, and each January 1 thereafter and prior to the

termination of the 2014 Equity Incentive Plan, pursuant to the terms of the Original Plan, the Plan Limit was and shall be increased by the lesser of (x) 4% of the number of shares of Common Stock outstanding as of the immediately preceding December 31 and (y) such lesser number as the Board of Directors (“Board”) may determine in its discretion. In March

2019, the Board adopted and the Company’s stockholders approved the Amended and Restated PDS Biotechnology Corporation 2014 Equity Incentive Plan (the “Prior Plan”) which amended and restated the Original Plan in order to remove the annual

increase component and was limited to 826,292 shares.

On December 8, 2020, the Board adopted and on June 17, 2021, the stockholders approved, the Second Amended and Restated PDS Biotechnology Corporation 2014 Equity Incentive Plan (the “Restated Plan”), which amended and restated the

Prior Plan. The Restated Plan is identical to the Prior Plan in all material respects, except (a) the number of shares of Common Stock authorized for issuance under the Restated Plan was increased from 826,292 shares to 4,165,535

shares, plus the total number of shares that remained available for issuance, that were not covered by outstanding awards issued under the Prior Plan, immediately prior to December 8, 2020; and (b) the Prior Plan was amended to terminate on

December 7, 2030, unless earlier terminated. On May 19, 2023, the Board adopted, subject to stockholder approval, the Third Amended and Restated PDS Biotechnology Corporation 2014 Equity Incentive Plan (the “Third Restated Plan”). At the 2023

annual meeting of stockholders held on July 14, 2023, the stockholders approved the Third Restated Plan, which amended and restated the Restated Plan to increase the total amount of shares authorized for issuance thereunder. The Third

Restated Plan is identical to the Restated Plan in all material respects, except, the number of shares of Common Stock authorized for issuance under the Third Restated Plan increased from 4,165,535 to 6,565,535. As of March 31, 2025 there were 2,306,538 shares available for grant under the Third Restated Plan.

Pursuant to the terms of the Third Restated Plan, stock options have a term of ten years from the date of grant or such

shorter term as may be provided in the option agreement. Unless specified otherwise in an individual option agreement, ISOs generally vest over a four-year

period.

On June 17, 2019, the Board adopted the 2019 Inducement Plan (the “Inducement Plan”). On December 8, 2020, the Company amended the Inducement Plan solely to

increase the total number of shares of common stock reserved for issuance under the Inducement Plan from 200,000 shares to 500,000 shares. On May 17, 2022, the Company further amended the Inducement Plan solely to increase the total number of shares of Common Stock reserved for issuance under the

Inducement Plan from 500,000 shares to 1,100,000 shares. On January 22, 2024, the Company further amended the Inducement Plan solely to increase the total number of shares of Common Stock reserved for issuance under the Inducement Plan from

1,100,000 shares to 2,100,000

shares. The Inducement Plan provides for the grant of non-qualified stock options. The Inducement Plan, and each amendment thereto, was recommended for approval by the Compensation Committee of the Board and subsequently approved and

adopted by the Board without stockholder approval pursuant to Rule 5635(c)(4) of the Nasdaq Listing Rules.

The Inducement Plan is administered by the Compensation Committee of the Board. In accordance with Rule 5635(c)(4) of the Nasdaq Listing Rules, non-qualified stock options under the Inducement Plan may only be

made to an employee who has not previously been an employee of the Company or member of the Board of Directors of the Company (or any parent or subsidiary of the Company), if he or she is granted such non-qualified stock options in

connection with his or her commencement of employment with the Company or a subsidiary and such grant is an inducement material to his or her entering into employment with the Company or such subsidiary. As of March 31, 2025, there

were 962,407 shares available for grant under the Inducement Plan.

The following table summarizes the components of stock-based compensation expense in the Condensed Consolidated Statements of Operations and Comprehensive Loss for the three months ended March 31, 2025 and 2024:

| |

|

Three Months Ended March 31,

|

|

| |

|

2025

|

|

|

2024

|

|

| |

|

(unaudited)

|

|

|

|

|

|

|

|

|

|

Research and development

|

|

$

|

520,527

|

|

|

$

|

551,918

|

|

|

General and administrative

|

|

|

733,355

|

|

|

|

1,078,093

|

|

|

Total

|

|

$ |

1,253,882

|

|

|

$

|

1,630,011

|

|

No options to purchase

shares were granted during the three month period ended March 31, 2025. The Company granted options to purchase 938,648 shares

during the three month period ended March 31, 2024. The fair value of options granted during the three months ended March 31, 2024 was estimated using the Black-Scholes option valuation model utilizing the following

assumptions:

| |

|

Three Months Ended March 31,

|

|

| |

|

2025

|

|

|

2024

|

|

| |

|

Weighted Average

|

|

|

Weighted Average

|

|

| |

|

(unaudited)

|

|

|

|

|

|

n/a

|

|

|

|

145.41

|

%

|

|

Risk-Free Interest Rate

|

|

|

n/a

|

|

|

|

3.98

|

%

|

|

Expected Term in Years

|

|

|

n/a

|

|

|

|

6.08

|

|

| Dividend Rate |

|

|

n/a |

|

|

|

– |

|

|

Fair Value of Option on Grant Date

|

|

|

n/a

|

|

|

$

|

5.22

|

|

The following table summarizes the number of options outstanding and the weighted average exercise price:

| |

|

Number

of Shares

|

|

|

Weighted

Average

Exercise Price

|

|

|

Weighted Average

Remaining

Contractual

Life in Years

|

|

|

Aggregate

Intrinsic Value

|

|

Options outstanding at December 31, 2024

|

|

|

5,373,063

|

|

|

$

|

6.08

|

|

|

|

7.11

|

|

|

$

|

50,439

|

|

|

Granted

|

|

|

–

|

|

|

|

–

|

|

|

|

– |

|

|

|

– |

|

|

Exercised

|

|

|

–

|

|

|

|

–

|

|

|

|

– |

|

|

|

– |

|

|

Forfeited and expired

|

|

|

(25,159

|

)

|

|

|

7.65

|

|

|

|

– |

|

|

|

– |

|

|

Options outstanding at March 31, 2025

|

|

|

5,347,904

|

|

|

$

|

6.07

|

|

|

|

6.90

|

|

|

$

|

2,115

|

|

|

Vested and expected to vest at March 31, 2025

|

|

|

5,347,904

|

|

|

$

|

6.07

|

|

|

|

6.90

|

|

|

$

|

2,115

|

|

|

Exercisable at March 31, 2025

|

|

|

3,656,731

|

|

|

$

|

5.91

|

|

|

|

6.20

|

|

|

$

|

2,115

|

|

As of March 31, 2025, the Company had approximately $9,379,169 of unamortized stock-based compensation expense, which is expected to be recognized over a remaining average vesting period of 2.36 years.

Note 8 – Income Taxes

The Company records a valuation allowance against its deferred tax

assets to reduce the net carrying value to an amount that it believes is more likely than not to be realized. In assessing the realizability of the net deferred tax assets, the Company considers all relevant positive and

negative evidence to determine whether it is more likely than not that some portion or all of the deferred tax assets will not be realized. The realization of the gross deferred tax assets is dependent on several factors, including the

generation of sufficient taxable income prior to the expiration of the net operating loss carryforwards. The Company expects to have a loss for 2025 and therefore there will be no current income tax expense. The Company recorded a full valuation allowance against the net deferred tax assets as of March 31, 2025

and December 31, 2024. Consequently, the Company recorded no income tax benefit due to realization uncertainties.

The Company is subject to a U.S. federal statutory income tax rate of 21%. The primary factor impacting the effective tax rate for the three months ended March 31, 2025 is the anticipated full year operating loss

which will require a full valuation allowance against any associated net deferred tax assets.

Entities are required to evaluate, measure, recognize and disclose any uncertain income tax positions taken on their

income tax returns. The Company has analyzed its tax positions and has concluded that as of March 31, 2025, there were no uncertain positions. The Company’s U.S. federal and state net operating losses have occurred since its inception and as such, tax years subject to potential tax examination could

apply from that date because the utilization of net operating losses from prior years opens the relevant year to audit by the IRS and/or state taxing authorities. The Company did not have any unrecognized tax benefits and has not accrued any

interest or penalties for the three months ended March 31, 2025 or for the year ended December 31, 2024.

In accordance with the State of

New Jersey’s Technology Business Tax Certificate Program, which allows certain high technology and biotechnology companies to sell unused NOL carryforwards to other New Jersey-based corporate taxpayers, the Company sold New Jersey NOL

carryforwards, resulting in the recognition of $1.2 million and $0.9 million of income tax benefit, net of transaction costs in the three months ended March 31, 2025 and in April 2024, respectively.

Note 9 – Commitments and Contingencies

Rent

For month-to-month arrangements not impacted by the adoption of ASC 842, rent for the three months ended March 31, 2025 and 2024 was $65,700 and $66,000, respectively.

Exclusive License Agreement

In December 2022, the Company entered into an exclusive global license agreement with Merck KGaA, Darmstadt, Germany for the tumor targeting IL 12 fused antibody drug conjugate, M9241 (the “Merck KGaA License Agreement”).

Pursuant to the Merck KGaA License Agreement, the Company agreed to make (i) development and first commercial sales milestone payments totaling up to $11

million upon the achievement of certain milestones, including the dosing of the fifth patient in a Phase 3 trial of the clinical candidate and first commercial sale of the product for a first and second indication in a major market, and (ii) up

to $105 million upon achieving certain aggregate sales levels of the product.

The Company also agreed to pay Merck KGaA, Darmstadt, Germany a royalty of 10% on aggregate net sales of product as specified in the Merck KGaA License Agreement on a product-by-product and country-by-country basis until the later of: (i) ten years after the first commercial sale of a product in a given country; and (ii) the expiration or invalidation of the licensed patents covering

the compound or product in such country. The royalty rate is subject to reduction in the event that a product is not covered by a valid patent claim, a biosimilar to the compound or the product comes on the market in a particular country, or if

the Company obtains a license to any intellectual property owned or controlled by a third-party which, but for such license would be infringed by making, using or selling the compound.

Legal Proceedings

The Company is currently not a party to, and the Company’s property is not currently the subject of, any material pending legal proceedings. The Company may be involved, from time to time, in legal proceedings and claims arising in the ordinary

course of business. Such matters are subject to many uncertainties and outcomes that may not be predictable with assurance.

Note 10 – Venture Loan and Security Agreement

In August 2022, the Company entered into a Venture Loan and Security Agreement (the “Loan and Security Agreement”) with

Horizon Technology Finance Corporation, as a lender and collateral agent for itself and the other Lenders (in such capacity, the “Collateral Agent”), and the other persons party thereto from time to time as lenders (“Lenders”). The

Company’s indebtedness under the Loan and Security Agreement was retired and satisfied in full with a portion of the proceeds received from the Securities Purchase Agreement, as discussed above.

For the three

months ended March 31, 2025 and 2024, the Company recognized interest expense of $928,177 and $1,170,758, respectively, in connection with the Loan and Security Agreement of which $272,578 and $270,236, respectively, was related to the amortization of the

debt discount.

Note 11 – Retirement Plan

The

Company has a 401(k) defined contribution plan for the benefit of all employees and permits voluntary contributions by employees, subject to IRS-imposed limitations. The 401(k) employer contributions were $65,540 and $66,488 for the three

months ended March 31, 2025 and 2024, respectively.

Note 12 – Segment Reporting

In accordance with FASB ASC Topic 280, Segment Reporting, the Company has determined that

it operates as a single reportable segment, developing a growing pipeline of targeted immunotherapies

designed to overcome the limitations of current immunotherapy. The financial results of the Company’s operations are managed and reported to the Chief Executive Officer who is considered the Company’s chief operating decision maker

(CODM), on a consolidated basis.

The CODM assesses performance and allocates resources based on the Company’s consolidated statements of operations and key components and processes of the Company’s

operations are managed centrally. Segment asset information is not used by the CODM to allocate resources.

As a single reportable segment

entity, the Company’s segment performance measure is net income / (loss) attributable to shareholders. Significant segment expenses, as provided to the CODM, are presented below:

| |

|

Quarter Ended March 31,

|

|

| |

|

2025

|

|

|

2024

|

|

|

Segment expenses

|

|

|

|

|

|

|

|

Salaries and Benefits

|

|

$

|

3,829,221

|

|

|

$

|

4,183,270

|

|

|

Professional fees

|

|

|

1,127,046

|

|

|

|

1,077,266

|

|

|

General administrative expenses

|

|

|

344,354

|

|

|

|

364,662

|

|

|

Clinical development expenses

|

|

|

2,432,198

|

|

|

|

3,113,509

|

|

|

Other development expenses

|

|

|

1,372,939

|

|

|

|

1,358,921

|

|

|

Total operating and segment expenses

|

|

$

|

9,105,758

|

|

|

$

|

10,097,627

|

|

| |

|

|

|

|

|

|

|

|

|

Interest income

|

|

|

377,849

|

|

|

|

668,895

|

|

|

Interest expense

|

|

|

(930,878

|

)

|

|

|

(1,174,745

|

)

|

|

Benefit from income taxes

|

|

|

1,169,820

|

|

|

|

–

|

|

|

Segment and consolidated net loss

|

|

$

|

(8,488,967

|

)

|

|

$

|

(10,603,477

|

)

|

Note 13 – Subsequent Events

On April 30, 2025, the Company entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with certain third

party lenders and JGB Collateral LLC, as collateral agent. Pursuant to the Securities Purchase Agreement, the Company agreed to sell (i) senior secured convertible debentures in an aggregate principal amount of $22,222,222 and (ii) warrants to purchase up to 1,000,000

shares of common stock, for an exercise price of $2.52 per share, subject to adjustments as set forth in the warrants, for a total

purchase price of $20,000,000.

Approximately $19 million

of the proceeds from the transactions contemplated by the Securities Purchase Agreement were used to satisfy in full and retire the Company’s indebtedness under the Loan and Security Agreement.

| ITEM 2. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

The following discussion and analysis of

our financial condition and results of operations should be read in conjunction with our unaudited interim condensed consolidated financial

statements and related notes thereto appearing elsewhere in this Quarterly Report on Form 10-Q (this “Quarterly Report”) and with the audited financial statements and notes thereto of the Company as of and for the year ended December 31, 2024 on Form

10-K, filed with the Securities and Exchange Commission, or SEC, on March 27, 2025.

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report contains forward-looking statements (including within the meaning of Section 21E of the United States Securities

Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning the Company and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events,

results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include

statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,”

“forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual

results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation:

|

● |

the Company’s ability to protect its intellectual property rights;

|

|

● |

the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future

equity financings;

|

|

● |

the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its clinical and product candidates, and the

risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or clinical and product candidates;

|

|

● |

the Company’s limited operating history in the current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the

likelihood of the Company’s successful implementation of such business plan;

|

|

● |

the timing for the Company or its partners to initiate the planned clinical trials for

its Versamune® products, including Versamune® HPV (formerly PDS0101), Versamune®

MUC1 (formerly PDS0103), and others, alone or in combination with PDS01ADC, as well as Infectimune® based clinical candidates and the future success of such trials;

|

|

● |

the successful implementation of the Company’s research and development programs and collaborations, including any collaboration trials concerning the Company’s

Versamune®, PDS01ADC and Infectimune® based clinical and product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success

of the Company’s clinical and product candidates;

|

|

● |

the success, timing and cost of the Company’s ongoing clinical trials and anticipated

clinical trials for the Company’s current clinical candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including our ability to fully fund our disclosed clinical trials, which

assumes no material changes to our currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim results (including, without limitation, any preclinical results or

data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials;

|

|

● |

expectations for the clinical and preclinical development, manufacturing, regulatory approval, and commercialization of the Company’s clinical and product candidates;

|

|

● |