UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

--12-31

FORM 20-F

| ☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2024

OR

| ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number 001-31236

TSAKOS ENERGY NAVIGATION LIMITED

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

Bermuda

(Jurisdiction of incorporation or organization)

367 Syngrou Avenue

175 64 P. Faliro

Athens, Greece

011-30210-9407710

(Address of principal executive offices)

Paul Durham

367 Syngrou Avenue

175 64 P. Faliro

Athens, Greece

Telephone: 011-30210-9407710

E-mail: ten@tenn.gr

Facsimile: 011-30210-9407716

(Name, Address, Telephone Number, E-mail and Facsimile Number of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

| Common Shares, par value $5.00 per share |

TEN |

NYSE |

Series E Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Shares, par

value $1.00 per share |

TEN.PRE |

NYSE |

Series F Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Shares, par

value $1.00 per share |

TEN.PRF |

NYSE |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

As of December 31, 2024, there were 30,127,603 of the registrant’s Common Shares, 4,745,947 Series E Preferred Shares and 6,747,147 Series F Preferred Shares outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated Filer ☒ Non-accelerated filer ☐ Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report Yes ☒ ☐ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b) ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ |

International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

TABLE OF CONTENTS

FORWARD-LOOKING INFORMATION

All statements in this Annual Report on Form 20-F that are not statements of historical fact are “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995. The disclosure and analysis set forth in this Annual Report on Form 20-F includes assumptions, expectations, projections, intentions and beliefs about future events in a number of places, particularly in relation to our operations, cash flows, financial position, plans, strategies, business prospects, changes and trends in our business and the markets in which we operate. These statements are intended as forward-looking statements. In some cases, predictive, future-tense or forward-looking words such as “believe,” “intend,” “anticipate,” “estimate,” “project,” “forecast,” “plan,” “potential,” “may,” “should” and “expect” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements.

Forward-looking statements include, but are not limited to, such matters as:

| |

• |

future operating or financial results and future revenues and expenses; |

| |

• |

future, pending or recent business and vessel acquisitions, business strategy, areas of possible expansion and expected capital spending and our ability to fund such expenditures; |

| |

• |

operating expenses including the availability of key employees, crew, length and number of off-hire days, dry-docking requirements and fuel and insurance costs; |

| |

• |

general market conditions and shipping industry trends, including charter rates, vessel values and factors affecting supply and demand of crude oil, petroleum products and LNG, including the impact of the conflict in Ukraine and related sanctions and the impact of tariffs imposed by the U.S. and other countries; |

| |

• |

our financial condition and liquidity, including our ability to make required payments under our credit facilities, comply with our loan covenants and obtain additional financing in the future to fund capital expenditures, acquisitions and other corporate activities, as well as higher inflation and increasing interest rate levels; |

| |

• |

the overall health and condition of the U.S. and global financial markets, including the value of the U.S. dollar relative to other currencies; |

| |

• |

the carrying value of our vessels and the potential for any asset impairments; |

| |

• |

our expectations about the time that it may take to construct and deliver new vessels or the useful lives of our vessels; |

| |

• |

our continued ability to enter into period time charters with our customers and secure profitable employment for our vessels in the spot market; |

| |

• |

the ability and willingness of our counterparties, including our charterers and shipyards, to honor their contractual obligations; |

| |

• |

our expectations relating to dividend payments and ability to make such payments; |

| |

• |

our ability to leverage to our advantage the relationships and reputation of Tsakos Shipping & Trading S.A. within the shipping industry; |

| |

• |

our anticipated general and administrative expenses; |

| |

• |

environmental and regulatory conditions, including changes in laws and regulations or actions taken by regulatory authorities; |

| |

• |

risks inherent in vessel operation, including terrorism, piracy and discharge of pollutants; |

| |

• |

potential liability from future litigation; |

| |

• |

global and regional political conditions; |

| |

• |

tanker, product carrier and LNG carrier supply and demand; and |

| |

• |

other factors discussed in the “Risk Factors” described in Item 3 of this Annual Report on Form 20-F. |

We caution that the forward-looking statements included in this Annual Report on Form 20-F represent our estimates and assumptions only as of the date of this Annual Report on Form 20-F and are not intended to give any assurance as to future results. These forward-looking statements are not statements of historical fact and represent only our management’s belief as of the date hereof, and involve risks and uncertainties that could cause actual results to differ materially and inversely from expectations expressed in or indicated by the forward-looking statements. Assumptions, expectations, projections, intentions and beliefs about future events may, and often do, vary from actual results and these differences can be material. There are a variety of factors, many of which are beyond our control, which affect our operations, performance, business strategy and results and could cause actual reported results and performance to differ materially from the performance and expectations expressed in these forward-looking statements. These factors include, but are not limited to, supply and demand for crude oil carriers, product tankers and LNG carriers, charter rates and vessel values, supply and demand for crude oil and petroleum products and liquefied natural gas, accidents, collisions and spills, environmental and other government regulation, the availability of debt financing, fluctuation of currency exchange and interest rates and the other risks and uncertainties that are outlined in this Annual Report on Form 20-F. As a result, the forward-looking events discussed in this Annual Report on Form 20-F might not occur and our actual results may differ materially from those anticipated in the forward-looking statements. Accordingly, you should not unduly rely on any forward-looking statements.

We undertake no obligation to update or revise any forward-looking statements contained in this Annual Report on Form 20-F, whether as a result of new information, future events, a change in our views or expectations or otherwise. New factors emerge from time to time, and it is not possible for us to predict all these factors. Further, we cannot assess the impact of each such factor on our business or the extent to which any factor, or combination of factors, may cause actual results to be materially different from those contained in any forward-looking statement.

PART I

Tsakos Energy Navigation Limited is a Bermuda company that is referred to in this Annual Report on Form 20-F, together with its subsidiaries, as “Tsakos Energy Navigation,” “the Company,” “we,” “us,” or “our.” This report should be read in conjunction with our consolidated financial statements and the accompanying notes thereto, which are included in Item 18 to this report.

Item 1. Identity of Directors, Senior Management and Advisers

Not Applicable.

Item 2. Offer Statistics and Expected Timetable

Not Applicable.

Item 3. Key Information

Capitalization

The following table sets forth our (i) cash and cash equivalents, (ii) restricted cash and (iii) consolidated capitalization as of December 31, 2024. This table should be read in conjunction with our consolidated financial statements and the notes thereto, and “Item 5. Operating and Financial Review and Prospects,” included elsewhere in this Annual Report.

| In thousands of U.S. Dollars |

|

As of December 31, 2024 |

| Cash |

|

|

| Cash and cash equivalents |

$ |

343,373 |

| Restricted cash |

|

4,939 |

| |

|

|

| Total cash |

|

348,312 |

| |

|

|

| Capitalization |

|

|

| Debt: |

|

|

| Long-term secured debt obligations and other financial liabilities (including current portion) 1 |

$ |

1,747,094 |

| |

|

|

| Stockholders’ equity: |

|

|

| Preferred shares, $1.00 par value; 25,000,000 shares authorized, 4,745,947 Series E Preferred Shares and 6,747,147 Series F Preferred Shares issued and outstanding |

|

11,493 |

| Common shares, $5.00 par value; 60,000,000 shares authorized; 30,805,776 shares issued, and 30,127,603 shares outstanding |

|

151,541 |

| Additional paid-in capital |

|

919,718 |

| Cost of treasury stock |

|

(6,791) |

| Accumulated other comprehensive loss |

|

(904) |

| Retained earnings |

|

652,651 |

| Non-controlling interest |

|

39,489 |

| |

|

|

| Total stockholders’ equity |

|

1,767,197 |

| |

|

|

| Total capitalization |

$ |

3,514,291 |

| 1 Obligations under operating leases are not included. |

|

|

Reasons for the Offer and Use of Proceeds

Not Applicable.

Risk Factors

Summary of Risk Factors

An investment in our common shares or preferred shares is subject to a number of risks, including risks related to our industry, business and corporate structure. The following summarizes some, but not all, of these risks. Please carefully consider all of the information discussed in “Item 3. Key Information— Risk Factors” in this annual report for a more thorough description of these and other risks.

Risks Related To Our Industry

| |

• |

The tanker industry is cyclical, resulting in charter rates that can be volatile. Poor charter markets for crude oil and product tankers may adversely affect our future revenues and earnings. |

| |

• |

Disruptions in global economic conditions, including as a result of the conflicts in Ukraine and the Middle East, as well as protectionist trade measures, including the tariffs recently imposed by the U.S. and retaliatory tariffs from other countries, and other governmental action, including related to tariffs imposed by the United States, could have a material adverse impact on our results of operations, financial condition, cash flows and share price. |

| |

• |

The tanker industry is highly dependent upon the crude oil and petroleum products industries, with the level of availability and demand for oil and petroleum products impacting demand for tankers and, in turn, charter rates. |

| |

• |

An increase in the supply of vessels could cause charter rates to decline, adversely affecting our results. |

| |

• |

We face substantial competition for charters, including from state and independent oil companies. |

| |

• |

We operate internationally, and terrorist attacks, international hostilities, economic sanctions and economic conditions could adversely affect our business. |

| |

• |

Failure to comply with the U.S. Foreign Corrupt Practices Act and other anti-bribery legislation could result in fines, criminal penalties, contract terminations and adversely affect our business. |

| |

• |

We are subject to regulation and liability under environmental, health and safety laws that could require significant expenditures, including with respect to climate change and greenhouse gas emissions, and customers and investors’ concerns related thereto. |

| |

• |

Increasing scrutiny and changing expectations from investors, lenders and other market participants with respect to ESG policies may impose additional costs on us or expose us to additional risks. |

Risks Related To Our Business

| |

• |

A decline in the future value of our vessels could affect our ability to comply with various covenants in our credit facilities, which are secured by mortgages on our subsidiaries’ vessels. |

| |

• |

Charters at attractive rates may not be available when our current time charters expire. |

| |

• |

We are dependent on the ability and willingness of our charterers to honor their commitments to us for substantially all our revenues. |

| |

• |

Contracts for newbuilding vessels present certain economic and other risks. |

| |

• |

Credit conditions internationally might impact our ability to raise debt financing. |

| |

• |

The future performance of our subsidiaries’ LNG carriers depends on continued growth in LNG production and demand for LNG and LNG shipping, which could be significantly affected by volatile natural gas prices and demand for natural gas, and the supply of LNG carriers. |

| |

• |

Our growth in shuttle tankers depends partly on continued growth in demand for offshore oil transportation, processing and storage services. |

| |

• |

Fuel prices may adversely affect our profits. |

| |

• |

The shipping industry has inherent operational risks that may not be adequately covered by our insurance. |

| |

• |

Failure to protect our information systems against security breaches could adversely affect our business and financial results. Additionally, if these systems fail or become unavailable for any significant period, our business could be harmed. |

| |

• |

Our degree of leverage and certain restrictions in our financing agreements impose constraints on us. |

| |

• |

We are exposed to volatility in SOFR and selectively enter into derivative contracts, which can result in higher than market interest rates and charges against our income. |

| |

• |

Inflation could adversely affect our business and financial results by increasing the costs of operating our business |

| |

• |

Because some of our subsidiaries’ vessels’ expenses are incurred in foreign currencies, we are exposed to exchange rate risks |

| |

• |

The Tsakos Holdings Foundation and the Tsakos family, who own a significant percentage of our common shares, can exert considerable influence over us, which may limit your ability to influence our actions. |

Risks Related to Our Management Arrangements

| |

• |

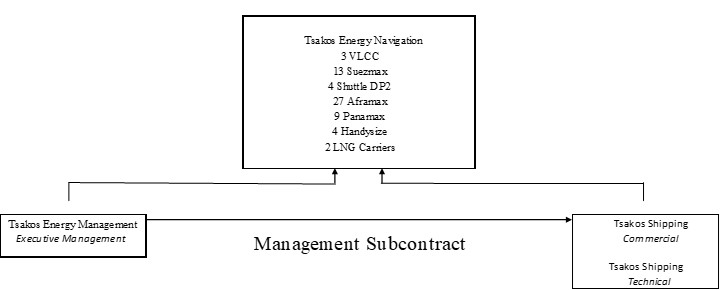

We depend on Tsakos Energy Management and Tsakos Shipping to manage our business, as we do not have the employee infrastructure to manage our operations and have no physical assets. |

| |

• |

Tsakos Shipping could experience conflicts of interests in performing obligations owed to us and the operators of other tankers, including tankers that clients of Tsakos Shipping have acquired. |

| |

• |

Our chief executive officer has affiliations with Tsakos Energy Management and Tsakos Shipping, which could create conflicts of interest. |

Risks Related To Our Common and Preferred Shares

| |

• |

Future sales of our shares in the public market could cause the market price of our shares to decline. |

| |

• |

We may not be able to pay cash dividends on our common shares or preferred shares as intended if market conditions change. |

| |

• |

Our preferred shares represent perpetual equity interests and holders have no right to receive any greater payment than the liquidation preference regardless of the circumstances. |

| |

• |

Holders of our preferred shares have extremely limited voting rights. |

| |

• |

Market interest rates may adversely affect the value of our Series E Preferred Shares and Series F Preferred Shares. |

| |

• |

Provisions in our Bylaws and our management agreement with Tsakos Energy Management would make it difficult for a third-party to acquire us, even if such a transaction is beneficial to our shareholders. |

| |

• |

Because we are a Bermuda company you may not have the same rights as a shareholder in a U.S. corporation. |

| |

• |

As “foreign private issuer” under NYSE rules we are entitled to exemption from certain NYSE corporate governance standards, and you may not have the same protections afforded to shareholders of companies that are subject to all of the NYSE corporate governance requirements. |

Tax Risks

| |

• |

If we became subject to tax in jurisdictions in which we operate, our financial results would be adversely affected. |

| |

• |

If we were treated as a passive foreign investment company, a U.S. investor in our shares would be subject to disadvantageous rules under U.S. tax laws. |

Risks Related To Our Industry

The tanker industry is cyclical, resulting in charter rates that can be volatile. Poor charter markets for crude oil and product tankers may adversely affect our future revenues and earnings.

The tanker industry is historically cyclical, resulting in volatility in charter rates, and, in turn, our revenue and earnings. The typical cycle is partially the result of fluctuations in the number of tankers available in the market, which determines the overall supply of tankers competing for charters. The number of tankers in the market changes as a result of new deliveries to the market, offset by vessels demolished or converted due to technical obsolescence, as well as changes in the number of vessels occupied on long-distance travel or delayed by geopolitical events. The cycle is also impacted by demand for charter hires resulting from material changes in the supply of and demand for oil due primarily to fluctuations in the price of oil and to geopolitical factors. As of April 4, 2025, half of the vessels owned by our subsidiary companies were employed under charters based upon prevailing market rates (including time charters with a profit share component), and the remaining vessels were employed on time charters which, if not extended, are scheduled to expire on various dates between April 2025 and April 2038, including twenty-one which are scheduled to expire within 2025.

After declining significantly from 2016 through most of 2018, adversely affecting our revenues, profitability and cash flows, tanker charter rates improved significantly in the latter part of 2019 and stayed strong through the first half of 2020 due mainly to a strong demand for floating oil storage brought about by low oil prices. However, stagnant demand for oil induced by the COVID-19 pandemic and the release of inventory from storage caused a dramatic fall in tanker rates in the second half of 2020 which continued through 2021 and through the first half of 2022, before increasing significantly since such time through the date of this Annual Report. The current crisis in Ukraine that started during the first quarter of 2022, has created a global redrawing of trade routes leading to an increase in the length of oil tanker voyages and sanctions have resulted in elimination of some vessels that are engaged in sanctioned activity from the available fleet. While the conflict in Ukraine is disrupting energy production and trade patterns and its impact on energy prices and tanker charter rates, which initially have increased, is uncertain. The factors influencing the supply of and demand for tanker shipping capacity are outside of our control, and we may not be able to correctly assess the nature, timing and degree of changes in industry conditions. The effective supply of tankers has been impacted in recent years by the impact of sanctions and trade pattern disruptions, including vessels currently continuing to reroute away from the Red Sea, Gulf of Aden and Suez Canal due to Houthi attacks on ships. These factors resulted in fleet inefficiencies and support for tanker charter rates, which may not continue.

If rates in the charter market were to decline and remain at low levels for any significant period in 2024, it will have an adverse effect on our revenues, profitability and cash flows. Declines in prevailing charter rates also affect the value of our vessels, which are correlated to the trends of charter rates, and could affect our ability to comply with our loan covenants.

Disruptions in global economic conditions, including due to the conflict in Ukraine and the Middle East, and protectionist trade measures such as tariffs and other governmental action in the United States and in other parts of the world could have a material adverse impact on our results of operations, financial condition, cash flows and share price.

Global economic conditions impact worldwide demand for energy and commodities and, thus, tanker shipping. The current macroeconomic environment is characterized by significant inflation, causing the U.S. Federal Reserve and other central banks to increase interest rates, which may raise the cost of capital, increase operating costs and reduce economic growth, disrupting global trade and shipping. Political events such as the continued and escalating global trade war between the U.S. and China, expansion of U.S. tariffs and trade protectionism policies to other countries, including Canada, Mexico and the E.U., and other policies that the new U.S. administration has stated, such as demands related to the operation of the Panama Canal, as well as ongoing conflicts throughout the world, such as those in Ukraine and in the Middle East, including Houthi attacks on ships in the Red Sea and the Gulf of Aden, may disrupt global supply chains and negatively impact globalization and global economic growth. Weakened global economic conditions could disrupt financial markets, and may lead to weaker energy demand in the European Union, the United States and other parts of the world which could have a material adverse effect on our business.

Beginning in February of 2022, President Biden and several European leaders announced various economic sanctions against Russia in connection with the aforementioned conflicts in the Ukraine region and continue to remain in effect, which may adversely impact our business. Our business could also be adversely impacted by trade tariffs, trade embargoes or other economic sanctions that limit trading activities by the United States or other countries against countries in the Middle East, Asia or elsewhere as a result of terrorist attacks, hostilities or diplomatic or political pressures. On March 8, 2022, President Biden issued an executive order, which still remains in effect, prohibiting the import of certain Russian energy products into the United States, including crude oil, petroleum, petroleum fuels, oils, liquefied natural gas and coal. Additionally, the executive order prohibits any investments in the Russian energy sector by US persons, among other restrictions both to common and preferred shareholders.

In addition, the exit of the UK from the European Union and the possible need of realignment of trading patterns as a consequence, as well as continued turmoil and hostilities in Ukraine and the Middle East or potential hostilities elsewhere in the world and additional public health emergencies or natural disasters, could contribute to volatility in the global financial markets. These circumstances, along with the re-pricing of credit risk and the reduced participation of certain financial institutions from financing of the shipping industry, will likely continue to affect the availability, cost and terms of vessel financing. If financing is not available to us when it is needed, or is available only on unfavorable terms, our business may be adversely affected, with corresponding effects on our profitability, cash flows and ability to pay dividends.

Our operations expose us to the risk that increased trade protectionism from the United States, China or other nations adversely affect world oil and petroleum markets and in turn the demand for energy shipping. Restrictions on imports, including in the form of tariffs, could have a major impact on global trade and demand for shipping. Tensions over trade and other matters remain high between the U.S. and China. In recent years, the United States instituted large tariffs on a wide variety of goods, including from China, which led to retaliatory tariffs from leaders of other countries including China, and the new U.S. administration, led by President Trump, has announced the intention to use tariffs extensively as a policy tool. The United States has recently imposed blanket 10% tariffs on virtually all imports to the U.S. and significantly higher tariffs applicable to imports from many countries, including tariffs aggregating 145% on imports from China, which have resulted in other countries imposing additional tariffs on imports from the U.S., including additional tariffs of 125% on imports from the U.S., announced by China, and is likely to continue to result in more retaliatory tariffs. On April 9, 2025, the U.S. announced a temporary pause on its tariffs applicable to many countries, while increasing the tariffs applicable to imports from China. The new U.S. administration has threatened to continue to broadly impose tariffs, which could lead to corresponding punitive actions by the countries with which the U.S. trades. The U.S. has also recently threatened to increase port fees for Chinese-built or owned ships, including for a vessel operator whose fleet includes one or more Chinese-built vessels or that has newbuilding orders at a Chinese shipyard. The proposal of the U.S. trade representative (USTR), if adopted as proposed, would require Chinese shipping companies to pay up to $1 million per port call and those operating Chinese-built vessels to be charged up to $1.5 million per U.S. port call, depending on the percentage of vessels in their fleet built at Chinese shipyards or newbuilding orders with Chinese shipyards. It is unknown whether and to what extent these new port fees on Chinese shipping companies and vessels will be adopted, or the effect that they would have on us or our industry generally. These policy pronouncements have created significant uncertainty about the future relationship between the United States and China, Canada, Mexico, the E.U. and other exporting countries, including with respect to trade policies, treaties, government regulations and tariffs, and has led to concerns regarding the potential for an extended trade war. Protectionist developments, or the perception they may occur, may have a material adverse effect on global economic conditions, and may significantly reduce global trade and, in particular, trade between the United States and other countries, including China, which could adversely and materially affect our business, results of operations, and financial condition.

The tanker industry is highly dependent upon the crude oil and petroleum products industries, with the level of availability and demand for oil and petroleum products impacting demand for tankers and, in turn, charter rates.

The employment of our subsidiaries’ vessels is driven by the availability of and demand for crude oil and petroleum products, the availability of modern tanker capacity and the scrapping, conversion, or loss of older vessels. Historically, the world oil and petroleum markets have been volatile and cyclical because of the many conditions and events that affect the supply, price, production and transport of oil, including:

| |

• |

increases and decreases in the demand and price for crude oil and petroleum products; |

| |

• |

availability of crude oil and petroleum products; |

| |

• |

demand for crude oil and petroleum product substitutes, such as natural gas, coal, hydroelectric power and other alternate sources of energy that may, among other things, be affected by environmental regulation; |

| |

• |

actions taken by OPEC and major oil producers and refiners; |

| |

• |

political turmoil in or around oil producing nations; |

| |

• |

global and regional political and economic conditions; |

| |

• |

developments in international trade; |

| |

• |

international trade sanctions; |

| |

• |

changes in seaborne and other transportation patterns. |

Despite turbulence in the world economy at times in recent years, worldwide demand for oil and oil products has continued to rise; however, the COVID-19 pandemic caused demand for oil and oil products to stagnate for an extended period of time. In the event that an economic slowdown results in a persistent stagnation or decline in demand and the long-term trend falters, the production of and demand for crude oil and petroleum products will encounter pressure which could lead to a decrease in shipments of these products and consequently this would have an adverse impact on the employment of our vessels and the charter rates that they command, as was case from the second half of 2020 until the second quarter of 2022. Also, if oil prices decline to uneconomic levels for producers, whether as a result of global economic weakness resulting from the escalating trade wars resulting from U.S. tariff announcements or otherwise, it may lead to declining output. As a result of any reduction in demand or output, the charter rates that we earn from our vessels employed on charters related to market rates may decline, and possibly remain at low levels for a prolonged period, as was the case for most periods during the preceding ten years.

Our operating results are subject to seasonal fluctuations.

The tankers owned by our subsidiary companies operate in markets that have historically exhibited seasonal variations in tanker demand, which may result in variability in our results of operations on a quarter-by-quarter basis. Tanker markets are typically stronger in the winter months due to increased oil consumption in the northern hemisphere, but weaker in the summer months as a result of lower oil consumption in the northern hemisphere and refinery maintenance. As a result, revenues generated by the tankers in our fleet have historically been weaker during the fiscal quarters ended June 30 and September 30. However, there may be periods in the northern hemisphere when the expected seasonal strength does not materialize to the extent required to support sustainable profitable rates due to tanker overcapacity.

An increase in the global supply of vessels, or specifically in a particular category of vessel, without an increase in demand for such vessels could cause global charter rates to decline, or rates for a particular category of vessel to decline, which could have a material adverse effect on our revenues and profitability.

Historically, the marine transportation industry has been cyclical. The profitability and asset values of companies in the industry have fluctuated based on certain factors, including changes in the supply and demand of vessels. The supply of vessels generally increases with deliveries of newly constructed vessels and decreases with the scrapping or conversion of older vessels and/or the removal of vessels from the competitive fleet either for storage purposes or for utilization in offshore projects. The newbuilding order book equaled approximately 14% of the existing world tanker fleet at the beginning of March 2025, by number of vessels, with a significant amount of these newbuilding vessels scheduled to be delivered in 2026. No assurance can be given that the order book will not increase further in proportion to the existing fleet. If vessel supply increases, and demand does not match that increase, the charter rates for our vessels could decline significantly. In addition, any decline of trade on specific long-haul trade routes will effectively increase available capacity with a detrimental impact on rates. A decline in charter rates could have a material adverse effect on our revenues and profitability.

The global tanker industry is highly competitive.

We operate our fleet in a highly competitive market. Our competitors include owners of VLCC, suezmax, aframax, dual-fuel LNG powered aframax, panamax and handysize tankers, as well as owners in the DP2 shuttle tanker and LNG markets, which are other independent tanker companies, as well as state and independent oil companies, some of which have greater financial strength and capital resources than we do. Competition in the tanker industry is intense and depends on price, location, size, age, condition, installation of required or technically up to date equipment and the acceptability of the available tankers and their operators to potential charterers.

Acts of piracy on ocean-going vessels could adversely affect our business.

Despite a decline in the frequency of pirate attacks on seagoing vessels in the western part of the Indian Ocean, such attacks remain prevalent off the west coast of Africa and between Malaysia and Indonesia. In addition, more recently, there has been an apparent attempted hijack of a tanker by stowaways off the UK coast, requiring military intervention by British special forces. If piracy attacks or vessel hijacks result in regions in which our vessels are deployed being characterized by insurers as “war risk” zones, as the Gulf of Aden has been, or Joint War Committee (JWC) “war and strikes” listed areas, premiums payable for such insurance coverage could increase significantly and such insurance coverage may be more difficult to obtain. Crew costs, including those due to employing onboard security guards, could increase in such circumstances. In addition, while we believe the charterer remains liable for charter payments when a vessel is seized by pirates, the charterer may dispute this and withhold charter hire until the vessel is released. A charterer may also claim that a vessel seized by pirates was not “on-hire” for a certain number of days and it is therefore entitled to cancel the charter party, a claim that we would dispute. We may not be adequately insured to cover losses from these incidents, which could have a material adverse effect on us. In addition, hijacking as a result of an act of piracy against our vessels, or an increase in cost, or unavailability of insurance for our vessels, could have a material adverse impact on our business, financial condition, results of operations and cash flows.

Terrorist attacks, international hostilities, economic and trade sanctions, including those related to the conflict in Ukraine, can affect the tanker industry, which could adversely affect our business.

Major oil and gas producing countries in the Middle East have become involved militarily in conflicts in Iraq, Syria, Azerbaijan and Yemen. Armed conflicts with insurgents and others continue, as well, in Chad and Libya, and political unrest and instability have adversely affected the infrastructure and economic stability of Venezuela, each of which is a major oil exporting country. In addition, tension and instability in the Persian Gulf and Red Sea, a vital passageway for international oil shipment, may adversely affect the future export of oil around the region.

Any such hostility or instability could seriously disrupt the production of oil or LNG and endanger their export by vessel or pipeline, which could put our vessels at serious risk and impact our operations and our revenues, expenses, profitability and cash flows in varying ways that we cannot now project with any certainty.

Furthermore, Russia’s invasion of Ukraine, and sanctions subsequently announced by the United States, the EU and several European and other nations against Russia and any further sanctions, including any sanctions or restrictions affecting companies with Russian connections or the Russian energy sector and harmed by any retaliatory measures by Russia or other countries in response, may also adversely impact our business given Russia’s role as a major global exporter of crude oil.

Since 2023 and into early 2025 Houthi rebels based in Yemen have been targeting vessels with drone attacks whilst transiting the Red Sea. Many shipowners and charterers have diverted vessels to avoid the area, despite a strong Naval presence in the area. Whilst the stated aim of the Houthi rebels has been to target vessels trading to or from Israel or with links to the US or UK, other non-related vessels have been attacked and our policy has therefore been to avoid transits of the Red Sea.

The increasing number of terrorist attacks throughout the world, longer-lasting wars, international incidents or international hostilities, such as in the Ukraine, Afghanistan, Iraq, Syria, Libya, Yemen and the Korean peninsula, could damage the world economy and adversely affect the availability of and demand for crude oil and petroleum products and negatively affect our investment and our customers’ investment decisions over an extended period of time. In addition, sanctions against oil exporting countries such as Iran, Sudan, Syria, Russia and Venezuela may also impact the availability of crude oil which would increase the availability of tankers, thereby negatively impacting charter rates. We conduct our vessel operations internationally and despite undertaking various security measures, our vessels may become subject to terrorist acts and other acts of hostility like piracy, either at port or at sea. Such actions could adversely impact our overall business, financial condition and results of operations. In addition, terrorist acts and regional hostilities around the world in recent years have led to increases in our insurance premium rates and the implementation of special “war risk” premiums for certain trading routes, although our charter party agreements generally provide that additional war risks insurance costs are for charterers’ account.

The conflict in Ukraine could disrupt our operations and negatively impact charter rates and costs.

The conflict in Ukraine, and the economic sanctions imposed by the EU, U.S. and other countries in response to Russian action, is disrupting energy production and trade patterns, including shipping in the Black Sea and elsewhere, and its impact on energy prices and tanker rates, which initially have increased, is uncertain. Some of these sanctions and executive orders target the Russian oil sector, including a prohibition on the import of oil from Russia to the United States or the United Kingdom, and the European Union's ban on Russian crude oil and petroleum products which took effect in December 2022 and February 2023, respectively, as well as a price cap on Russian oil of $60 per barrel. Prior to the war, Russia exported approximately 5.5 mbpd of seaborne crude oil and refined petroleum products to the EU, USA, South Korea and Japan. After February 2023, Russia is exporting less than 0.4 mbpd to these countries. The price of crude oil (Brent) initially traded above $100 per barrel as a result of the war and escalating tensions in the region and fears of potential shortages in the supply of Russian crude oil but has since come down and is now trading above $60 per barrel. Russian crude oil is restricted for export, due to the extension of economic sanctions, and has also been impacted by boycotts and general sentiment, which could result in a reduction in the supply of crude oil and refined petroleum products cargoes available for transportation and, while initially tanker rates have increased, this could negatively impact tanker charter rates over the longer term. In addition, higher oil prices could reduce demand for oil and refined petroleum products, including in the event of any slowdown in the global economy due such high oil prices or the impact of economic sanctions or geopolitical tensions and uncertainty, and in turn reduce demand for tankers and tanker charter rates. The conflict may also impact various costs of operating our business, such as bunker expenses, for which we are responsible when our vessels operate in the spot market, which have increased with higher oil prices, war risk insurance premiums and crewing services, as Russia and the Ukraine are significant sources of crews, which may be disrupted or more expensive.

In addition, our vessels carry lawful cargoes originating in Russia, in compliance with existing sanctions, oil majors and other charterers may elect not to charter our vessels simply for doing business with companies that do lawful business in Russia. In addition, it may not be possible for us to obtain war risk insurance for any vessel loading Russian origin cargoes, in which case our vessels would not be allowed to call Russian ports and thereby impacting the vessels’ future trading pattern and earnings.

The situation in Ukraine, and the global response, continues to evolve and its impact on energy supply and demand, energy prices and tanker operations and charter rates remains subject to considerable uncertainty, which could adversely impact our business, results of operations and financial condition.

Our charterers may direct one of our vessels to call on ports located in countries that are subject to restrictions imposed by the U.S. government, the UN or the EU, which could negatively affect the trading price of our shares.

On charterers’ instructions, our subsidiaries’ vessels may be requested to call on ports located in countries subject to sanctions and embargoes imposed by the U.S. government, the UN or the EU and countries identified by the U.S. government, the UN or the EU as state sponsors of terrorism. The U.S., UN- and EU- sanctions and embargo laws and regulations vary in their application, as they do not all apply to the same covered persons or proscribe the same activities, and such sanctions and embargo laws and regulations may be amended or strengthened over time.

The U.S. also maintains embargoes on Cuba, North Korea and Syria, and certain regions of Ukraine. Beginning in February 2022, the United States, the European Union and numerous other nations have also been imposing substantial additional sanctions on Russia regarding its invasion of Ukraine.

We can anticipate that some of our charterers may request our vessels to call on ports located in these countries. Although we believe that we are in compliance with all applicable sanctions and embargo laws and regulations, and intend to maintain such compliance, there can be no assurance that we will be in compliance in the future, particularly as the scope of certain laws may be unclear and may be subject to changing interpretations. Such sanctions and embargo laws and regulations may be amended or expanded over time as is the case with the war in Ukraine. Any such violation could result in fines or other penalties and could result in some investors deciding, or being required, to divest their interest, or not to invest, in us. Additionally, some investors may decide to divest their interest, or not to invest, in us simply because we do business with companies that do lawful business in sanctioned countries. Moreover, our charterers may violate applicable sanctions and embargo laws and regulations because of actions that do not involve us or our vessels, and those violations could in turn negatively affect our reputation. Current or future counterparties of ours may be or become affiliated with persons or entities that are now or may in the future be the subject of sanctions imposed by the U.S. Government, the European Union, and/or other international bodies. If we determine that such sanctions or embargoes require us to terminate existing or future contracts to which we, or our subsidiaries are a party or if we are found to be in violation of such applicable sanctions or embargoes, we could face monetary fines, we may suffer reputational harm and our results of operations may be adversely affected. Investor perception of the value of our shares may also be adversely affected by the consequences of war, the effects of terrorism, civil unrest and governmental actions in these and surrounding countries.

Failure to comply with the U.S. Foreign Corrupt Practices Act and other anti-bribery legislation in other jurisdictions could result in fines, criminal penalties, contract terminations and an adverse effect on our business.

The vessels of our subsidiaries load and discharge cargoes in several countries throughout the world. In addition, we deal with many charterers and shipbrokers that are based in various countries. Certain of the countries in which these charterers and brokers operate may, in the past, have had a reputation for corruption. Brazilian authorities have charged certain shipbrokers with various offenses in connection with charters entered into between a major state oil entity and various international shipowners. We are subject to the risk that the alleged actions taken by these brokers are determined to constitute a violation of anti-corruption laws applicable to the Company, including the U.S. Foreign Corrupt Practices Act of 1977 (the “FCPA”). In 2020, in parallel with U.S. Department of Justice and U.S. Securities and Exchange Commission investigations regarding whether the circumstances surrounding these charters, including the actions taken by these shipbrokers, constituted non-compliance with provisions of the FCPA applicable to the Company, we began investigating these matters. We are always committed to doing business in accordance with anti-corruption laws and cooperated with these agencies. In June 2024, the SEC informed the Company that it had terminated its investigation of the Company.

Any violation of the FCPA or other anti-bribery legislation in other jurisdictions could result in substantial fines, sanctions, civil and/or criminal penalties, or curtailment of operations in certain jurisdictions, and might adversely affect our business, results of operations or financial condition. In addition, actual or alleged violations could damage our reputation and ability to do business. Furthermore, detecting, investigating, and resolving actual or alleged violations is expensive and can consume significant time and attention of our senior management.

Efforts to take advantage of opportunities in pursuit of our growth strategy may result in financial or commercial difficulties.

A key strategy of management is to continue to renew and grow the fleet by pursuing the acquisition of additional vessels or fleets or companies that are complementary to our existing operations. If we seek to expand through acquisitions, we face numerous challenges, including:

| |

• |

difficulties in raising the required capital; |

| |

• |

depletion of existing cash resources more quickly than anticipated; |

| |

• |

assumption of potentially unknown material liabilities or contingent liabilities of acquired companies; and |

| |

• |

competition from other potential acquirers, some of which have greater financial resources. |

We cannot assure you that we will successfully integrate the operations, personnel, services or vessels that we might acquire in the future, and our failure to do so could adversely affect our profitability.

Increasing scrutiny and changing expectations from investors, lenders and other market participants with respect to ESG policies may impose additional costs on us or expose us to additional risks.

Companies across all industries, including the shipping industry, are facing increased scrutiny relating to their ESG policies. Investor advocacy groups, certain institutional investors, investment funds, lenders and other market participants are increasingly focused on ESG practices and in recent years have placed increasing importance on the implications and social cost of their investments. The increased focus and activism related to ESG and similar matters may hinder access to capital, as investors and lenders may decide to reallocate capital or to not commit capital as a result of their assessment of a company’s ESG practices. Companies which do not adapt to or comply with investor, lender or other industry shareholder expectations and standards, which are evolving, or which are perceived to have not responded appropriately to the growing concern for ESG issues, regardless of whether there is a legal requirement to do so, may suffer from reputational damage and the business, financial condition, and/or the stock price of such a company could be materially and adversely affected. As a result, we may be required to implement more stringent ESG procedures or standards so that we continue to have access to capital and our existing and future investors and lenders remain invested in us and make further investments in us.

Specifically, we may face increasing pressures from investors, lenders and other market participants, who are increasingly focused on climate change, to prioritize sustainable energy practices, reduce our carbon footprint and promote sustainability. Additionally, certain investors and lenders may exclude tanker shipping companies, such as us, from their investing portfolios altogether due to environmental, social and governance factors. If we are faced with limitations in the debt and/or equity markets as a result of these concerns, or if we are unable to access alternative means of financing on acceptable terms, or at all, we may be unable to access funds to implement our business strategy or service our indebtedness, which could have a material adverse effect on our financial condition and results of operations.

We are subject to regulation and liability under environmental, health and safety laws that could require significant expenditures and affect our cash flows and net income.

Our business and the operation of our subsidiaries’ vessels are subject to extensive international, national, and local environmental and health and safety laws and regulations in the jurisdictions in which our vessels operate, as well as in the country or countries of their registration. In addition, major oil companies chartering our vessels impose, from time to time, their own environmental and health and safety requirements.

To comply with these requirements and regulations, such as the MARPOL Annex VI sulfur emission requirements instituting a global 0.5% sulfur cap on marine fuels from January 1, 2020 ,the IMO ballast water management (“BWM”) convention, which requires vessels to install ballast water treatment systems (“BWTS”) with a ship specific timeframe latest by September 8, 2024 and the latest MARPOL Annex VI amendments that introduced the technical and operational measures of the Energy Efficiency Existing Shipping Index (“EEXI”) and the Carbon Intensity Indicator (“CII”) to reduce carbon emissions produced by vessels, we may be required to incur additional costs to meet new maintenance and inspection requirements, develop contingency plans for potential mitigation measures, and obtain insurance coverage. Vessels that continually receive subpar CII ratings will be required to submit corrective action plans to ensure compliance.

In addition, as of January 1, 2024, the European Union expanded the existing EU Emissions Trading System (“EU ETS”) to include carbon dioxide (“CO2”) emissions from vessels of 5,000 gross tonnage and above. Shipping companies which perform voyages to/from/within the EU and EEA (Iceland, Liechtenstein and Norway) will need to acquire and surrender EU allowances (“EUAs”) through their Union Registry account by September of the following year to cover their annual emissions. One EUA is equivalent to one tonne of CO2 emission. The EU ETS covers 50% of emissions from voyages starting or ending outside of the EU and 100% of emissions from voyages that occur between two EU ports and when ships are within EU ports. The surrendering of allowances by shipping companies will be gradually increased with respect to verified emissions reported for the years 2024 and 2025. This means, in 2025, shipping companies will be liable to surrender allowances for 40% of verified emissions reported in 2024. In 2026, this increases to 70% of verified emissions reported in 2025. As of 2027 and each year thereafter, shipping companies will have to surrender allowances reflecting 100% of their verified emissions.

These and future environmental regulations, which may become stricter, may limit our ability to do business, increase our operating costs and/or force the early retirement of our vessels, all of which could have a material adverse effect on our financial condition and results of operations. Environmental laws and regulations are often revised, and we cannot predict the ultimate cost of complying with them, or the impact they may have on the resale prices or useful lives of our vessels. We believe that regulation of the shipping industry will continue to become more stringent and compliance with such new regulations will be more expensive for us and our competitors.

International, national and local laws imposing liability for oil spills and carbon emissions are also becoming increasingly stringent. Some impose joint, several, and in some cases, unlimited liability on owners, operators and charterers for oil spills regardless of fault. We could be held liable as an owner, operator or charterer under these laws. In addition, under certain circumstances, we could also be held accountable under these laws for the acts or omissions of Tsakos Shipping & Trading S.A. (“Tsakos Shipping”), Tsakos Energy Management Limited (“Tsakos Energy Management”) or other companies that provide technical and commercial management services for our subsidiaries’ vessels and us, or others in the management or operation of our subsidiaries’ vessels. Although we currently maintain, and plan to continue to maintain, for each of our subsidiaries’ vessels’ pollution liability coverage in the amount of $1 billion per incident (the maximum amount available), liability for a catastrophic spill could exceed the insurance coverage we have available and result in our having to liquidate assets to pay claims. In addition, we may be required to contribute to funds established by regulatory authorities for the compensation of oil pollution damage or provide financial assurances for oil spill liability to regulatory authorities.

Adverse effects upon the oil and gas industry relating to climate change, including growing public concern about the environmental impact of climate change, may also have an effect on demand for our services. For example, increased regulation of greenhouse gases or other concerns relating to climate change may reduce the demand for oil and natural gas in the future or create greater incentives for use of alternative energy sources. Any long-term material adverse effect on the oil and gas industry could have significant financial and operational adverse impacts on our business that we cannot predict with certainty at this time.

Maritime disasters and other operational risks may adversely impact our reputation, financial condition, and results of operations.

The operation of ocean-going vessels has an inherent risk of maritime disaster and/or accident, environmental mishaps, cargo and property losses or damage and business interruptions caused by, among others:

| |

• |

adverse weather conditions; |

| |

• |

vessel off hire periods; |

| |

• |

political action, civil conflicts, terrorism and piracy in countries where vessel operations are conducted, vessels are registered or from which spare parts and provisions are sourced and purchased. |

Any of these circumstances could adversely affect our operations, result in loss of revenues or increased costs and adversely affect our profitability and our ability to perform our charters.

Our subsidiaries’ vessels could be arrested at the request of third-parties.

Under general maritime law in many jurisdictions, crew members, tort claimants, vessel mortgagees, suppliers of goods and services and other claimants may lien a vessel for unsatisfied debts, claims or damages. In many jurisdictions a maritime lien holder may enforce its lien by arresting a vessel through court process. In some jurisdictions, under the extended sister ship theory of liability, a claimant may arrest not only the vessel with respect to which the claimant’s maritime lien has arisen, but also any associated vessel under common ownership or control. While in some jurisdictions which have adopted this doctrine, liability for damages is limited in scope and would only extend to a company and its ship-owning subsidiaries, we cannot assure you that liability for damages caused by some other vessel determined to be under common ownership or control with our subsidiaries’ vessels would not be asserted against us.

Risks Related To Our Business

A decline in the future value of our vessels could affect our ability to comply with various covenants in our credit facilities unless waived or modified by our lenders.

Our credit facilities, which are secured by mortgages on our subsidiaries’ vessels, require us to maintain specified collateral coverage ratios and satisfy financial covenants, including requirements based on the market value of our vessels, such as maximum corporate leverage levels and loan-to-asset collateral coverage requirements. The appraised value of a vessel fluctuates depending on a variety of factors including the age of the vessel, its hull configuration, prevailing charter market conditions, supply and demand balance for vessels and new and pending legislation. If these values again decline, it may result in an inability to comply with the financial covenants under our credit facilities which relate to our consolidated leverage and loan-to-asset value collateral requirements. If we were unable to obtain waivers in the case of non-compliance with consolidated leverage or other financial covenants or post additional collateral or prepay principal in the case of loan-to-asset value requirements, our lenders could accelerate our indebtedness.

Charters at attractive rates may not be available when our current time charters expire.

During 2024, we derived approximately 73% of our revenues from time charters, as compared to 61% in 2023. Although tanker charter rates are currently at relatively high levels, as our current period charters on twenty-one of the vessels owned by our subsidiary companies expire in the remainder of 2025 and for additional vessels in future years, considering the volatile nature of the tanker market, it may not be possible to re-charter these vessels on a period basis at attractive rates. If attractive period charter opportunities are not available, we may seek to charter the vessels owned by our subsidiary companies on the spot market, which is subject to significant fluctuations. In the event a vessel owned by one of our subsidiary companies may not find employment at economically viable rates, management may opt to lay up the vessel until such time that rates become attractive again (an action which our subsidiary companies have never undertaken). During the period of any layup, the vessel would continue to incur expenditures such as debt service, insurance, reduced crew wages and maintenance costs.

We are dependent on the ability and willingness of our charterers to honor their commitments to us for substantially all our revenues and the failure of our counterparties to meet their obligations under our charter agreements could cause us to suffer losses or otherwise adversely affect our business.

We derive substantially all our revenues from the payment of charter hire by our charterers. As of April 4, 2025, 51 of our 61 subsidiaries’ vessels were employed under time charters including time charters with profit sharing provisions above specified minimum rate levels. We could lose a charterer or the benefits of a time charter if:

| |

• |

the charterer fails to make charter payments to us because of its financial inability, liquidation, disagreements with us, defaults on a payment or otherwise; |

| |

• |

the charterer exercises certain specific limited rights to terminate the charter; |

| |

• |

we do not take delivery of a newbuilding vessel we may contract for at the agreed time; or |

| |

• |

the charterer terminates the charter because the vessel fails to meet certain guaranteed speed and fuel consumption requirements and we are unable to rectify the situation or otherwise reach a mutually acceptable settlement; or. |

| |

• |

a serious accident or explosion occurs at a client refinery. |

If we lose a time charter, we may be unable to re-deploy the related vessel on terms as favorable to us or at all. We would not receive any revenues from such a vessel while it remained unchartered, but we may be required to pay expenses necessary to maintain the vessel in proper operating condition, insure it and service any indebtedness secured by such vessel.

The ability and willingness of each of the counterparties to perform their obligations under their charters will depend on a number of factors that are beyond our control and may include, among other things, general economic conditions, the condition of the oil and energy industries and of the oil and oil products shipping industry as well as the overall financial condition of the counterparties and prevailing charter rates. There can be no assurance that some of our subsidiaries’ customers would not fail to pay charter hire or attempt to renegotiate charter rates and, if the charterers fail to meet their obligations or attempt to renegotiate charter agreements, we could sustain significant losses which could have a material adverse effect on our business, financial condition, results of operations and cash flows, as well as our ability to pay dividends in the future.

If our charterers fail to meet their obligations to us or attempt to renegotiate our charter agreements, as part of a court-led restructuring or otherwise, we could sustain significant reductions in revenue and earnings which could have a material adverse effect on our business, financial condition, results of operations and cash flows, as well as our ability to pay dividends, if any, in the future, and comply with the covenants in our credit facilities.

If our exposure to the spot market increases, our revenues could suffer and our expenses could increase.

The spot market for crude oil and petroleum product tankers is highly competitive. As of April 4, 2025, ten of the vessels owned by our subsidiary companies were employed under spot charters, as we have decided to maintain a considerable number of vessels in the spot market to take advantage of current high spot rates. Due to increased participation in the spot market, we may experience a lower overall utilization of our fleet through waiting time or ballast voyages, which could lead to a decline in operating revenue in rate environments where spot rates earned do not offset such lower utilization. Moreover, to the extent our vessels are employed in the spot market, both our revenue from vessels and our operating costs, specifically our voyage expenses, will be significantly impacted by adverse movements in the cost of bunkers (fuel), including the price of low sulfur fuel certain of our vessels have been required to use since the beginning of 2020. See “—Fuel prices may adversely affect our profits.” Unlike time charters in which the charterer bears all the bunker costs, in spot market voyages we bear the bunker charges as part of our voyage costs. As a result, while historical movements in bunker prices are factored into the prospective freight rates for spot market voyages periodically announced by World Scale Association (London) Limited and similar organizations, increases in bunker prices in any given period could have a material adverse effect on our cash flow and results of operations for the period in which the increase occurs. In addition, to the extent we employ our vessels pursuant to contracts of affreightment, the rates that we earn from the charterers under those contracts may be subject to reduction based on market conditions, which could lead to a decline in our operating revenue.

Because the market value of our vessels may fluctuate significantly, we may incur impairment charges or losses when we sell vessels which may adversely affect our earnings.

The fair market value of tankers may increase or decrease depending on any of the following:

| |

• |

general economic and market conditions affecting the tanker industry; |

| |

• |

supply and demand balance for ships within the tanker industry; |

| |

• |

competition from other shipping companies; |

| |

• |

types and sizes of vessels; |

| |

• |

other modes of transportation; |

| |

• |

governmental or other regulations; |

| |

• |

prevailing level of charter rates; and |

| |

• |

technological advances. |

Currently tanker market values are at relatively high levels, but until the second half of 2022 were at relatively low levels for most of the period since the financial crisis in 2008, falling whenever there was excess fleet capacity and declining freight rates. Although our subsidiaries currently own a relatively modern fleet, with an average age of 10.4 years as of April 4, 2025, as vessels grow older, they generally decline in value.

We have a policy of considering the disposal of tankers periodically. If our subsidiaries’ tankers are sold at a time when tanker prices have fallen, the sale may be at less than the vessel’s carrying value on our financial statements, with the result that we will incur a loss.

In addition, accounting standards require that we periodically review long-lived assets and certain identifiable intangibles for impairment whenever events or changes in circumstances indicate that the carrying amount of the assets may not be recoverable. An impairment charge for an asset held for use should be recognized when the estimate of undiscounted cash flows, excluding interest charges, expected to be generated by the use of the asset is less than it’s carrying amount. Measurement of the impairment charge is based on the fair value of the asset as provided by third-parties. In cases where sale and purchase activity in the market does not exist or is limited, the Company uses future discounted net operating cash flows or a combination of future discounted net operating cash flows and third-party valuations to estimate the fair value of an impaired vessel, respectively. Such reviews may from time-to-time result in asset write-downs, which could adversely affect our results of operations, such as we did in 2023, with respect one of our subsidiaries’ LNG carriers.

If Tsakos Shipping and Trading S.A. (“Tsakos Shipping” or “TST”) is unable to attract and retain skilled crew members, our reputation and ability to operate safely and efficiently may be harmed.

Our continued success depends in significant part on the continued services of the officers and seamen whom TST provides to crew the vessels owned by our subsidiary companies. The market for qualified, experienced officers and seamen is extremely competitive and has grown more so in recent periods due to the growth in world economies and other employment opportunities. Although TST has manning management arrangements with a number of accredited manning agencies in Philippines, Ukraine, Romania, Georgia, Latvia, Brazil, Greece and Uruguay and sponsors various academies in the relevant regions, we cannot assure you that TST will be successful in its efforts to recruit and retain properly skilled personnel at commercially reasonable salaries. Any failure to do so could adversely affect our ability to operate cost-effectively and our ability to increase the size of the fleet.

Labor interruptions could disrupt our operations.

Substantially all of the seafarers and land-based employees of TST are covered by industry-wide collective bargaining agreements that set basic standards. We cannot assure you that these agreements will prevent labor interruptions. In addition, like many other vessels internationally, some of our subsidiaries’ vessels operate under so-called “flags of convenience” and may be vulnerable to unionization efforts by the International Transport Federation and other similar seafarer organizations which could be disruptive to our operations. Any labor interruption or unionization effort which is disruptive to our operations could harm our financial performance.

Contracts for new building vessels present certain economic and other risks.

As of April 4, 2025, our subsidiaries have contracts for the construction of twelve DP2 suezmax shuttle tankers for delivery in 2025, 2026, 2027 and 2028, two suezmax tankers for delivery in 2025, two MR tankers for delivery in 2026 and five LR1 tankers for delivery in 2027 and 2028. Our subsidiaries may also order additional new building vessels. During the construction of a vessel, we are required to make progress payments and need to finance the purchase price upon delivery of the vessel, with remaining purchase price obligations for new buildings of $2.0 billion, as of April 4, 2025, funding which will require us to obtain substantial additional secured debt and/or other financing. We have arranged senior secured debt financing for the remaining installment payments for the three DP2 suezmax shuttle tankers of these new buildings and we are in the process of seeking to arrange debt financing for the remaining eighteen new buildings. Management is in discussion with various high-end charterers to employ the two MR tankers and the five LR1 tankers on long-term contracts upon delivery, for which charters have not yet been arranged. While we typically have refund guarantees from banks to cover defaults by shipyards and our construction contracts would be saleable in the event of our payment default, we can still incur economic losses if we or the shipyards are unable to fulfil our respective obligations. Shipyards may periodically experience financial difficulties.

Delays in the delivery of these vessels, or any new building our subsidiaries may agree to acquire, could delay our receipt of revenues generated by these vessels and, to the extent we have arranged charter employment for these vessels, could possibly result in the cancellation of those charters, and therefore adversely affect our anticipated results of operations. The delivery of new building vessels could be delayed because of, among other things: work stoppages or other labor disturbances; bankruptcy or other financial crisis of the shipyard building the vessel; hostilities or political or economic disturbances in the countries where the vessels are being built; weather interference or catastrophic events, such as a major earthquake, tsunami or fire; our requests for changes to the original vessel specifications; requests from our customers, with whom our commercial managers arrange charters for such vessels, to delay construction and delivery of such vessels due to weak economic conditions and shipping demand or a dispute with the shipyard building the vessel.

Credit conditions internationally might impact our ability to raise debt financing.

Global financial markets and economic conditions have been disrupted and volatile for periods in recent years. At times, the credit markets as well as the debt and equity capital markets were distressed, and it was difficult for many shipping companies to obtain adequate financing. The cost of available financing also increased significantly, but for leading shipping companies has since declined. The global financial markets and economic conditions could again experience volatility and disruption in the future.

We have traditionally financed our vessel acquisitions or constructions with our own cash (equity), including from share issuances, and bank debt from various reputable national and international commercial banks. In relation to new building contracts, the equity portion usually covers part of the pre-delivery obligations while the debt portion covers the outstanding amount due to the shipyard on delivery. However, we may arrange pre-delivery bank financing to cover much of the installments due before delivery, and, therefore, we would be required to provide the remainder of our equity investment at delivery. In addition, several of our existing loans will mature over the next few years, including five in 2025. If the related vessels are not sold, or we do not wish to use existing cash for paying the final balloon payments, then re-financing of the loans for an extended period beyond the maturity date will be necessary. Current and future terms and conditions of available debt financing, especially for older vessels without time charter could be different from terms obtained in the past and could result in a higher cost of capital, if available at all. Any adverse development in the credit markets could materially alter our current and future financial and corporate planning and growth and have a negative impact on our balance sheet.

The future performance of our subsidiaries’ LNG carriers depends on continued growth in LNG production and demand for LNG and LNG shipping.