UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2024

|

OR

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________________ to ____________________

|

OR

| ☐ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission file number: 001-40065

IM Cannabis Corp.

(Exact name of Registrant as specified in its charter)

British Columbia, Canada

(Jurisdiction of incorporation or organization)

3606 – 833 Seymour Street, Vancouver, British Columbia V6B 0G4

(Address of principal executive offices)

Oren Shuster, 972 544331111, oren@imcannabis.com

3606 – 833 Seymour Street, Vancouver, British Columbia V6B 0G4

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

|

Trading Symbol

|

|

Name of each exchange on which registered

|

|

Common Shares, no par value

|

|

IMCC

|

|

Nasdaq Capital Market

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: N/A

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 3,085,452 Common Shares

Indicate by check mark if the Company is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the Company is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the Company (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the Company has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Company was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the Company is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

|

Accelerated filer ☐

|

|

Non-accelerated filer ☒

|

|

Emerging growth company ☒

|

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the Company has used to prepare the financial statements included in this filing:

|

U.S. GAAP ☐

|

International Financial Reporting Standards as issued By the International Accounting Standards Board ☒

|

Other ☐

|

If “Other” has been checked in response to previous question, indicate by check mark which financial statement item the Company has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the Company is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

TABLE OF CONTENTS

|

|

5 |

|

|

7 |

|

|

12 |

|

|

|

12 |

|

|

|

12 |

|

|

|

12 |

|

A. |

Reserved. |

12 |

|

B. |

Capitalization and Indebtedness |

12 |

|

C. |

Reasons for the Offer and Use of Proceeds

|

13 |

|

D. |

Risk Factors |

13 |

|

|

|

41

|

|

A. |

History and Development of the Company

|

41

|

|

B. |

Business Overview |

47 |

|

C. |

Organizational Structure |

65 |

|

D. |

Property, Plants and Equipment |

65 |

|

|

|

66 |

|

|

|

66

|

|

A. |

Operating Results |

66

|

|

B. |

Liquidity and capital resources

|

66

|

|

C. |

Research and development, patents and

licenses, etc |

66 |

|

D. |

Trend Information |

67 |

|

E. |

Critical Accounting Estimates |

67 |

|

|

|

80

|

|

A. |

Directors and Senior Management |

80

|

|

B. |

Compensation |

83

|

|

C. |

Board Practices |

95

|

|

D. |

Employees |

102

|

|

E. |

Share Ownership |

103

|

|

F. |

Disclosure of a registrant’s action

to recover erroneously awarded compensation |

103

|

|

|

|

103

|

|

A. |

Major Shareholders |

103

|

|

B. |

Related Party Transactions |

105

|

|

C. |

Interests of Experts and Counsel

|

107

|

|

|

|

107

|

|

A. |

Consolidated Statements and Other Financial

Information |

107

|

|

B. |

Significant Changes |

113

|

|

|

|

114

|

|

A. |

Offer and Listing Details |

114

|

|

B. |

Plan of Distribution |

114

|

|

C. |

Markets |

114

|

|

D. |

Selling Shareholders |

114

|

|

E. |

Dilution |

114

|

|

F. |

Expenses of the Issue |

114

|

|

|

|

114

|

|

A. |

Share Capital |

114

|

|

B. |

Memorandum and Articles of Association

|

114

|

|

C. |

Material Contracts |

119

|

|

D. |

Exchange Controls |

119

|

|

E. |

Taxation |

120

|

|

F. |

Dividends and Paying Agents |

127

|

|

G. |

Statement by Experts |

127 |

|

H. |

Documents on Display |

127 |

|

I. |

Subsidiary Information |

128 |

|

J. |

Annual Report to Security Holders

|

128 |

|

|

|

128 |

|

|

|

128 |

|

|

|

128

|

|

|

|

128 |

|

|

|

129 |

|

A. |

Disclosure Controls and Procedures

|

129 |

|

B. |

Management’s Annual Report on Internal

Control Over Financial Reporting |

129 |

|

C. |

Attestation Report of Registered Public

Accounting Firm |

129 |

|

D. |

Changes in Internal Controls Over Financial

Reporting |

129 |

|

|

|

130 |

|

|

|

130 |

|

|

|

130 |

|

|

|

131 |

|

|

|

131 |

|

|

|

132 |

|

|

|

132 |

|

|

|

133 |

|

|

|

133 |

|

|

|

133 |

|

|

|

133 |

| |

Risk Management and Strategy |

133

|

| |

Governance |

134

|

|

|

|

135 |

|

|

|

135 |

|

|

|

136 |

INTRODUCTION

In this annual report on Form 20-F (this “Annual

Report”), “Company,” “IMC,”

“Group,” “we,” “us”

and “our” refer to IM Cannabis Corp., and its consolidated subsidiaries, and Focus

(as defined herein) an Israeli private company over which IMC Holdings (as defined herein) exercises “de facto” control under.

Information contained in this Annual Report is given as of December 31, 2024, the

fiscal year end of Company, unless otherwise specifically stated.

Market and industry data used throughout this Annual Report was obtained from various

publicly available sources. Although the Company believes that these independent sources are generally reliable, the accuracy and completeness

of such information are not guaranteed and have not been verified due to limits on the availability and reliability of raw data, the voluntary

nature of the data gathering process and the limitations and uncertainty inherent in any statistical survey of market size, conditions

and prospects.

Statements made in this Annual Report concerning the contents of any contract, agreement

or other document are summaries of such contracts, agreements or documents and are not complete descriptions of all of their terms. If

we file any of these documents as an exhibit to this Annual Report, you may read the document itself for a complete description of its

terms.

Unless otherwise indicated and except for per share data and the information contained under “Item

6B. Compensation”, all dollar figures in this Annual Report are expressed in thousands and

all references in this Annual Report to: (i) “dollars” or “CAD”

or “$” are to Canadian dollars; (ii) “USD”

or “US$” are to United States of America (“U.S.”

or “United States”) dollars; (iii) “NIS”

are to New Israeli Shekels; and (iv) “€” or to “Euros”

are to Euros. All intercompany balances and transactions were eliminated on consolidation. Common shares, stock options, units, prefunded

warrants, warrants, and prices, are not expressed in thousands.

On July 12, 2024, the Company consolidated all of its issued and outstanding Common Shares (as defined

herein) on a 6:1 basis (the “July 2024 Consolidation”). All references to Common Shares,

and securities issuable into Common Shares in this Annual Report, other than in documents dated prior to July 12, 2024, that are incorporated

by reference in this Annual Report, reflect post-July 2024 Consolidation amounts unless otherwise indicated or the context otherwise requires.

All documents dated prior to July 12, 2024, that are incorporated by reference in this Annual Report reflect pre-July 2024 Consolidation

amounts unless otherwise indicated or the context otherwise requires.

References herein to “Q1 2023”, “Q2 2023”, “Q2 2024”,

“Q3, 2024” and “Q4 2024” refers to the three months ended March 31, 2023, June 30, 2023, June 30, 2024, September

30, 2024, and December 31, 2024, respectively.

This Annual Report should be read in conjunction with the audited consolidated financial statements of

the Company and the notes thereto as at and for the years ended December 31, 2024, and 2023 (the “2024

Annual Financial Statements”) and the accompanying management’s discussion and analysis for the years ended December

31, 2024, and 2023 (the “2024 Annual MD&A”). The 2024 Annual Financial Statements

were prepared by management in accordance with the International Financial Reporting Standards (“IFRS”)

as issued by the International Accounting Standards Board. IFRS requires management to make certain judgments, estimates and assumptions

that affect the reported amount of assets and liabilities at the date of the 2024 Annual Financial Statements and the amount of revenue

and expenses incurred during the reporting period. The results of operations for the periods reflected herein are not necessarily indicative

of results that may be expected for future periods.

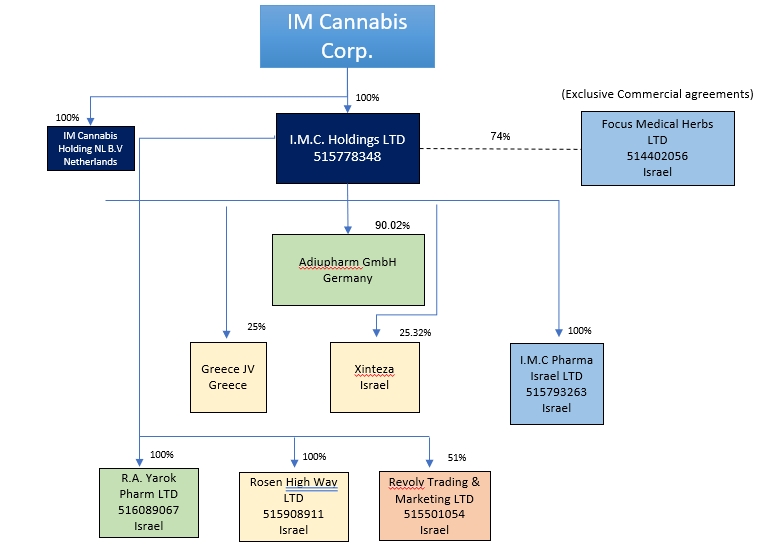

The 2024 Annual Financial Statements, includes the accounts of the Company, its consolidated

subsidiaries and Focus, which includes, among others, the following entities:

|

Legal

Entity |

Jurisdiction

|

Relationship

with the Company |

|

I.M.C.

Holdings Ltd. (“IMC Holdings”) |

Israel

|

Wholly-owned

subsidiary |

|

I.M.C.

Pharma Ltd. (“IMC Pharma”) |

Israel

|

Wholly-owned

subsidiary of IMC Holdings |

|

Focus

Medical Herbs Ltd.(1) (“Focus”)

|

Israel

|

Private

company over which IMC Holdings exercises “de facto control” under IFRS 10 |

|

R.A.

Yarok Pharm Ltd. (“Pharm Yarok”) |

Israel

|

Wholly-owned

subsidiary of IMC Holdings |

|

Rosen

High Way Ltd. (“Rosen High Way”) |

Israel

|

Wholly-owned

subsidiary of IMC Holdings |

Revoly Trading and Marketing Ltd. d/b/a Vironna Pharm (“Vironna”)

|

Israel

|

Subsidiary

of IMC Holdings |

|

Adjupharm GmbH (“Adjupharm”)

|

Germany |

Subsidiary of IMC

Holdings |

|

Xinteza API Ltd (“Xinteza”)

|

Israel |

Subsidiary of IMC

Holdings |

|

Shiran Societe Anonyme

(“Greece”) |

Greece |

Subsidiary of IMC

Holdings |

|

IM Cannabis Holding

NL B.V Netherlands (“IMC Holdings NL”) |

Netherlands |

Wholly-owned subsidiary

of IMC Holdings |

Oranim Plus Pharm Ltd. (“Oranim Plus”) 2)

|

Israel

|

Former

subsidiary of IMC Holdings |

|

Trichome Financial

Corp. (3) |

Canada |

Former wholly-owned

subsidiary |

|

I.M.C

Farms Israel Ltd. (“IMC Farms”).

(4) |

Israel

|

Wholly-owned

subsidiary of IMC Holdings |

|

IMCC

Medical Herbs Ltd. (“IMCC Medical Herbs”)(5)

|

Israel

|

Wholly-owned

subsidiary of IMC Holdings |

|

High Way Shinua Ltd.

(“High Way Shinua”)(6)

|

Israel |

Subsidiary of IMC

Holdings |

|

(1) |

Effective February 26, 2024, IMC Holdings exercised its option to acquire a 74% ownership stake in Focus. |

|

(2) |

Effective April 16, 2024, IMC Holdings no longer holds shares in Oranim Plus. For more information, please see “Item

4B. History and Development of the Company Important Events in the Development of the Business in Fiscal 2024 to the date of this Annual

Report”. |

|

(3) |

Discontinued operations. Please see note 25 in the 2024 Annual Financial Statements |

|

(4) |

On January 8, 2025, the Israeli Companies Registrar approved the liquidation of IMC Farms, which will be

completed within 100 days from the date of approval. |

|

(5) |

On January 13, 2025, the Israeli Companies Registrar approved the liquidation status of IMCC Medical Herbs,

stating that the liquidation will be completed within 100 days from the date of approval. |

|

(6) |

On December 14, 2023, Israeli Companies Registrar approved the liquidation status of High Way Shinua, which

liquidation was completed on March 23, 2024. |

Please see Exhibit 8.1 for a complete list of the Company’s subsidiaries.

In this Annual Report, unless otherwise indicated, all references to: (i) “Company

Subsidiaries” are to the Israeli Subsidiaries and Adjupharm, (ii) “Israeli Operations”

are to IMC Holdings and the Israeli Subsidiaries as defined below (iii) “Trichome”

are to Trichome Financial Corp. and its subsidiaries. As of the date of this Annual Report “Israeli

Subsidiaries” means IMC Holdings, IMC Pharma, Focus, Pharm Yarok, Rosen High Way, Vironna, Xinteza and Focus.

CAUTIONARY

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report, including any documents incorporated by reference herein, contains

“forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws

(collectively referred to herein as “forward-looking statements”). All statements other

than statements of fact may be deemed to be forward-looking statements, including statements with regard to expected financial performance,

strategy and business conditions. The words “believe”, “plan”, “intend”, “estimate”, “expect”,

“anticipate”, “continue”, or “potential”, and similar expressions, as well as future or conditional

verbs such as “will”, “should”, “would”, and “could” often identify forward-looking statements.

These statements reflect management’s current beliefs with respect to future events and are based on information currently available

to management as of the date of this Annual Report, or a document incorporated by reference therein, including reasonable assumptions,

estimates, internal and external analysis and opinions of management considering its experience, perception of trends, current conditions

and expected developments as well as other factors that management believes to be relevant as at the date such statements are made.

Without limitation, this Annual Report contains forward-looking statements pertaining

to:

|

• |

the Company’s business objectives and milestones and the anticipated timing of execution; |

|

• |

the performance of the Company’s business, strategies and operations; |

|

• |

the Company’s intentions to expand the business, operations and potential activities of the Company; |

|

• |

the Company’s plans to expand its sales channels, distribution, delivery and storage capacity, and reach to medical cannabis

patients; |

|

• |

the competitive conditions of the cannabis industry and the growth of medical or adult-use recreational cannabis markets in the jurisdictions

in which the Company operates; |

|

• |

the competitive conditions of the industry, including the Company’s ability to maintain or grow its market share and maintain

its competitive advantages; |

|

• |

statements relating to the Company’s commitment to responsible growth and compliance with the strictest regulatory environments;

|

|

• |

the Company’s focus on providing premium cannabis products to medical patients in the jurisdictions in which the Company conducts

business and any other jurisdiction in which the Company may conduct business in the future; |

|

• |

the Company’s plans to amplify its commercial and brand power to become a global high-quality cannabis player; |

|

• |

the Company’s primary goal of sustainably increasing revenue in its core markets; |

|

• |

the demand and momentum in the Company’s Israeli and Germany operations; |

|

• |

how the Company intends to position its brands; |

|

• |

the efficiencies and synergies of the Company as a global organization with domestic expertise in Israel and Germany; |

|

• |

expectations that providing high-quality, reliable supply to the Company’s customers and patients will lead to recurring sales;

|

|

• |

expectations related to the Company’s introduction of new Stock Keeping Units (“SKUs”);

|

|

• |

anticipated cost savings from the reorganization of the Company and the completion thereof upon the timelines disclosed herein;

|

|

• |

geographic diversification and brand recognition and the growth of the Company’s brands in the jurisdictions that the Company

operates in or may expand to; |

|

• |

expectations related to the Company’s ability to address the ongoing needs and preferences of medical cannabis patients;

|

|

• |

the Company’s retail presence, distribution capabilities and data-driven insights; |

|

• |

the future impact of the Regulations Amendment (as defined herein) regarding the transition reform from licenses to prescriptions

for medical treatment of cannabis; |

|

• |

the Company’s continued partnerships with third party suppliers and partners and the benefits thereof; |

|

• |

the Company’s ability to achieve profitability in 2025; |

|

• |

the number of patients in Israel licensed by the Israeli Ministry of Health (“MOH”)

to consume medical cannabis; |

|

• |

expectations relating to the number of patients paying out-of-pocket for medical cannabis products in Germany; |

|

• |

the anticipated decriminalization or legalization of adult-use recreational cannabis in Israel and Germany; |

|

• |

expectations related to the demand and the ability of the Company to source premium and ultra-premium cannabis products exclusively

and competition in this product segment; |

|

• |

the anticipated impact of inflation and liquidity on the Company’s performance; |

|

• |

expectations with respect to the Company’s operating budget and the assumptions related thereto; |

|

• |

expectations relating to the Company as a going concern and its ability to conduct business under the ordinary course of operations;

|

|

• |

expectations related to the collection of the payment awarded in Test Kits Appeal, and the potential outcome of the Test Kits Appeal

(as defined herein); |

|

• |

the continued listing of the common shares in the capital of the Company (“Common Shares”)

on the Nasdaq Stock Market (“Nasdaq”) and Canadian Securities Exchange (“CSE”);

|

|

• |

cannabis licensing in the jurisdictions in which the Company operates; |

|

• |

the renewal and/or extension of the Company’s licenses; |

|

• |

the Company’s anticipated operating cash requirements and future financing needs; |

|

• |

the Company’s expectations regarding its revenue, expenses, profit margins and operations; |

|

• |

the expected increase in revenue and margins in its Israeli medical cannabis market activities arising from its acquisitions;

|

|

• |

future opportunities for the Company in Israel, particularly in the retail and distribution segments of the cannabis market;

|

|

• |

future expansion and growth opportunities for the Company in Germany and Europe and the timing of such; and |

|

• |

contractual obligations and commitments. |

With respect to the forward looking-statements contained in this Annual Report, the

Company has made assumptions regarding, among other things:

|

• |

the Company has the ability to achieve its business objectives and milestones under the stated timelines; |

|

• |

the Company will succeed in carrying out its business, strategies and operations; |

|

• |

the Company will realize upon its intentions to expand the business, operations and potential activities of the Company; |

|

• |

the Company will expand its sales channels, distribution, delivery and storage capacity, and reach to medical cannabis patients;

|

|

• |

the competitive conditions of the cannabis industry and the growth of medical or adult-use recreational cannabis in the jurisdictions

in which the Company operates; |

|

• |

the competitive conditions of the industry will be favorable to the Company, and the Company has the ability to maintain or grow

its market share and maintain its competitive advantages; |

|

• |

the Company will commit to responsible growth and compliance with the strictest regulatory environments; |

|

• |

the Company will remain focused on providing premium cannabis products to medical patients in the jurisdictions in which the Company

conducts business and any other jurisdiction in which the Company may conduct business in the future; |

|

• |

the Company has the ability to amplify its commercial and brand power to become a global high-quality cannabis player; |

|

• |

the Company will maintain its primary goal of sustainably increasing revenue in its core markets; |

|

• |

the demand and momentum in the Company’s Israeli and Germany operations will be favorable to the Company; |

|

• |

the Company will carry out its plans to position its brands as stated; |

|

• |

the Company has the ability to realize upon the stated efficiencies and synergies the Company as a global organization with domestic

expertise in Israel and Germany; |

|

• |

providing a high-quality, reliable supply to the Company’s customers and patients will lead to recurring sales; |

|

• |

the Company will introduce new SKUs; |

|

• |

the Company will realize the anticipated cost savings from the reorganization; |

|

• |

the Company has the ability to achieve geographic diversification and brand recognition and the growth of the Company’s brands

in the jurisdictions that the Company operates in or may expand to; |

|

• |

the Company’s has the ability to address the ongoing needs and preferences of medical cannabis patients; |

|

• |

the Company has the ability to realize upon its retail presence, distribution capabilities and data-driven insights; |

|

• |

the future impact of the Regulations Amendment will be favorable to the Company; |

|

• |

the Company will maintain its partnerships with third parties, suppliers and partners; |

|

• |

the Company has the ability to achieve profitability in 2025; |

|

• |

the accuracy of number of patients in Israel licensed by the MOH to consume medical cannabis; |

|

• |

the accuracy of the number of patients paying out-of-pocket medical cannabis products in Germany; |

|

• |

the anticipated decriminalization or legalization of adult-use recreational cannabis in Israel and Germany will occur; |

|

• |

the Company has the ability to source premium and ultra-premium cannabis products exclusively and competition in this product segment;

|

|

• |

the anticipated impact of inflation and liquidity on the Company’s performance will be as forecasted; |

|

• |

the accuracy with respect to the Company’s operating budget and the assumptions related thereto; |

|

• |

the Company will remain as going concern; |

|

• |

a favorable outcome with respect to the collection of the awards in successful judgements, and the success of other ongoing claims

the Company is involved in; |

|

• |

the Company’s Common Shares will remain listed on the Nasdaq and CSE; |

|

• |

the Company’s ability to maintain cannabis licensing in the jurisdictions in which the Company operates; |

|

• |

the Company has the ability to obtain the renewal and/or extension of the Company’s licenses; |

|

• |

the Company has the ability to meet operating cash requirements and future financing needs; |

|

• |

the Company will meet or surpass its expectations regarding its revenue, expenses, profit margins and operations; |

|

• |

the Company will have the ability to collect the payment awarded in Test Kits Appeal; |

|

• |

the Company will increase its revenue and margins in its Israeli medical cannabis market activities arising from its acquisitions;

|

|

• |

the Company has the ability to capitalize on future opportunities for the Company in Israel, particularly in the retail and distribution

segments of the cannabis market; |

|

• |

the Company will carry out its future expansion and growth opportunities for the Company in Germany and Europe and the timing of

such; and |

|

• |

the Company will fulfill its contractual obligations and commitments. |

Readers are cautioned that the above lists of forward-looking statements and assumptions

are not exhaustive. Since forward-looking statements address future events and conditions, by their very nature they involve inherent

risks and uncertainties. Actual results may differ materially from those currently anticipated or implied by such forward-looking statements

due to a number of factors and risks. These include:

|

• |

the Company’s inability to achieve its business objectives and milestones under the stated timelines; |

|

• |

the Company inability to carry out its business, strategies and operations; |

|

• |

the Company’s inability to realize upon its intentions to expand the business, operations and potential activities of the Company;

|

|

• |

the Company will not expand its sales channels, distribution, delivery and storage capacity, and reach to medical cannabis patients;

|

|

• |

the competitive conditions of the cannabis industry and the growth of medical or adult-use recreational cannabis markets will be

unfavorable to the Company in the jurisdictions in which the Company operates; |

|

• |

the competitive conditions of the industry will be unfavorable to the Company, and the Company’s inability to maintain or grow

its market share and maintain its competitive advantages; |

|

• |

the Company will not commit to responsible growth and compliance with the strictest regulatory environments; |

|

• |

the Company’s inability to remain focused on providing premium cannabis products to medical patients in the jurisdictions in

which the Company conducts business and any other jurisdiction in which the Company may conduct business in the future; |

|

• |

the Company inability to amplify its commercial and brand power to become a global high-quality cannabis player; |

|

• |

the Company will not maintain its primary goal of sustainably increasing revenue in its core markets; |

|

• |

the demand and momentum in the Company’s Israeli and Germany operations will be unfavorable to the Company; |

|

• |

the Company will not carry out its plans to position its brands as stated; |

|

• |

the Company’s inability to realize upon the stated efficiencies and synergies of the Company as a global organization with

domestic expertise in Israel and Germany; |

|

• |

providing a high-quality, reliable supply to the Company’s customers and patients will not lead to recurring sales; |

|

• |

the Company will not introduce new SKUs; |

|

• |

the Company’s inability to realize upon the anticipated cost savings from the reorganization; |

|

• |

the Company’s inability to achieve geographic diversification and brand recognition and the growth of the Company’s brands

in the jurisdictions that the Company operates in or may expand to; |

|

• |

the Company’s inability to address the ongoing needs and preferences of medical cannabis patients; |

|

• |

the Company’s inability to realize upon its retail presence, distribution capabilities and data-driven insights; |

|

• |

the future impact of the Regulations Amendment will be unfavorable to the Company; |

|

• |

the Company will not maintain its partnerships with third party suppliers and partners; |

|

• |

the Company’s inability to achieve profitability in 2025; |

|

• |

the inaccuracy of number of patients in Israel licensed by the MOH to consume medical cannabis; |

|

• |

the inaccuracy of the number of patients paying out-of-pocket for medical cannabis products in Germany; |

|

• |

the anticipated decriminalization or legalization of adult-use recreational cannabis in Israel and Germany will not occur;

|

|

• |

the Company’s ability to source premium and ultra-premium cannabis products exclusively and competition in this product segment;

|

|

• |

the anticipated impact of inflation and liquidity on the Company’s performance will not be as forecasted; |

|

• |

the inaccuracy with respect to the Company’s operating budget and the assumptions related thereto; |

|

• |

the Company will not remain as going concern; |

|

• |

an unfavorable outcome of legal proceedings the Company is involved in; |

|

• |

an unfavorable outcome with respect to the collection of the award pursuant to the Test Kits Appeal and the Company being unsuccessful

in other ongoing claims the Company is involved in; |

|

• |

the Company’s Common Shares will not remain listed on the Nasdaq and CSE; |

|

• |

the Company’s inability to maintain cannabis licensing in the jurisdictions in which the Company operates; |

|

• |

the Company’s inability to obtain the renewal and/or extension of the Company’s licenses; |

|

• |

the Company’s inability to meet operating cash requirements and future financing needs; |

|

• |

the Company will not meet or surpass its expectations regarding its revenue, expenses, profit margins and operations; |

|

• |

the Company will not increase its revenue and margins in its Israeli medical cannabis market activities arising from its acquisitions;

|

|

• |

the Company’s ability to capitalize on future opportunities for the Company in Israel, particularly in the retail and distribution

segments of the cannabis market; |

|

• |

the Company will not carry out its future expansion and growth opportunities for the Company in Germany and Europe and the timing

of such; and |

|

• |

the Company will not fulfill its contractual obligations and commitments. |

The foregoing list of risk factors is not exhaustive. Additional

information on these and other factors that could affect the business, operations or financial results of the Company are detailed under

the heading “Risk Factors” in this Annual Report. Unless otherwise indicated, forward-looking statements in this Annual Report

describe our expectations as of the date of this Annual Report. The Company and management caution readers not to place undue reliance

on any forward-looking statements, which speak only as of the date made. Although the Company believes that the expectations reflected

in the forward-looking statements are reasonable, it can give no assurance that such expectations will prove to have been correct. The

Company and management assume no obligation to update or revise them to reflect new events or circumstances except as required by applicable

securities laws.

Additional information about the assumptions, risks and uncertainties of the Company’s

business and material factors or assumptions on which information contained in forward-looking statements is based is provided in the

Company’s disclosure materials, including in the Annual MD&A under “Legal and Regulatory

– Risk Factors”, available on the Company’s profile on SEDAR+ at www.sedarplus.ca

and on EDGAR at www.sec.gov/edgar

.

CAUTIONARY

NOTE REGARDING FUTURE ORIENTED FINANCIAL INFORMATION

This Annual Report may contain future oriented financial information (“FOFI”)

within the meaning of Canadian securities legislation and analogous U.S. securities laws, about prospective results of operations, financial

position or cash flows, based on assumptions about future economic conditions and courses of action, which FOFI is not presented in the

format of a historical balance sheet, income statement or cash flow statement. The FOFI has been prepared by management to provide an

outlook of the Company’s activities and results and has been prepared based on a number of assumptions including the assumptions

discussed under the heading above entitled “Cautionary Note Regarding Forward-Looking Statements”

and assumptions with respect to the costs and expenditures to be incurred by the Company, capital expenditures and operating costs, taxation

rates for the Company and general and administrative expenses. Management does not have, or may not have had at the relevant date, firm

commitments for all of the costs, expenditures, prices or other financial assumptions which may have been used to prepare the FOFI or

assurance that such operating results will be achieved and, accordingly, the complete financial effects of all of those costs, expenditures,

prices and operating results are not, or may not have been at the relevant date of the FOFI, objectively determinable.

Importantly, the FOFI contained in this Annual Report are, or may be, based upon certain

additional assumptions that management believes to be reasonable based on the information currently available to management, including,

but not limited to, assumptions about: (i) the future pricing for the Company’s products, (ii) the future market demand and trends

within the jurisdictions in which the Company may from time to time conduct the Company’s business, (iii) the Company’s ongoing

inventory levels, and operating cost estimates, and (iv) the Company’s financial results for 2025. The FOFI or financial outlook

contained in this Annual Report do not purport to present the Company’s financial condition in accordance with IFRS as issued by

the International Accounting Standards Board, and there can be no assurance that the assumptions made in preparing the FOFI will prove

accurate. The actual results of operations of the Company and the resulting financial results will likely vary from the amounts set forth

in the analysis presented in any such document, and such variation may be material (including due to the occurrence of unforeseen events

occurring subsequent to the preparation of the FOFI). The Company and management believe that the FOFI has been prepared on a reasonable

basis, reflecting management’s best estimates and judgments as at the applicable date. However, because this information is highly

subjective and subject to numerous risks including the risks discussed under the heading above entitled “Cautionary

Note Regarding Forward-Looking Statements” and under the heading “Risk Factors”

in the Company’s public disclosures, FOFI or financial outlook within this Annual Report should not be relied on as necessarily

indicative of future results.

Readers are cautioned not to place undue reliance on the FOFI, or financial outlook

contained in this Annual Report. Except as required by Canadian securities laws and analogous U.S. securities laws, the Company does not

intend, and does not assume any obligation, to update such FOFI.

PART I

ITEM 1. IDENTITY

OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER

STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY

INFORMATION

A. Reserved.

B. Capitalization

and Indebtedness

Not applicable.

C. Reasons

for the Offer and Use of Proceeds

Not applicable.

D. Risk

Factors

The Company’s operations and financial performance are subject to the normal

risks of its industry and are subject to various factors which are beyond the control of the Company. Certain of these risk factors are

described below. The risks described below are not the only ones facing the Company. Additional risks not currently known to the Company,

or that it currently considers immaterial, may also adversely impact the Company’s business, operations, financial results or prospects,

should any such other events occur.

Risks Relating to Our Business

There are certain risks associated with owning securities of the Company that holders

should carefully consider. The risks and uncertainties below are not the only risks and uncertainties facing the Company. Additional risks

and uncertainties not presently known to the Company or that the Company currently considers immaterial may also impair the business,

operations and future prospects of the Company, cause the price of its securities to decline and cause future results to differ materially

from those described herein. If any of the following risks actually occur, the business of the Company may be harmed, and its financial

condition and results of operations may suffer significantly. In that event, the trading price of the Company’s securities could

decline, and holders may lose all or part of their investment.

The cannabis-related business and activities of the Group are heavily regulated in

all jurisdictions where it carries on business. The Group’s operations are subject to various laws, regulations and guidelines by

governmental authorities, particularly the MOH, and the Federal Opium Agency of Germany’s Federal Institute for Drugs and Medical

Devices in Germany (“BfArM”), relating to the grow, propagate, manufacture, marketing,

management, transportation, storage, distribution, sale, pricing and disposal of dried and fresh cannabis, cannabis plants and seeds,

edible cannabis, cannabis extracts, clones and plants and cannabis extracts. The Group’s operations are also subject to laws and

regulations relating to health and safety, insurance coverage, the conduct of operations and the protection of the environment.

The

Company consolidates certain financial results under IFRS 10 and any failure to maintain common control could result in a material adverse

effect on the business, results of operations and financial condition of the Company

The Company complies with IFRS 10, which applies a single consolidation model using

a definition of “control” that requires an investor (as defined in IFRS 10) to consolidate an investee (as defined in IFRS

10) where: (i) the investor has power over the investee; (ii) the investor has exposure or rights to variable returns from involvement

with the investee; and (iii) the investor can use its power over the investee to affect the amount of the investor’s returns.

The Company analyzed the terms of the contractual agreements with Focus in accordance

with IFRS 10 to conclude whether it should continue to consolidate the accounts of Focus in its financial statements.

Under IFRS 10, consolidation occurs when an investor can exercise control over an

investee. Control is achieved through voting rights or other evidence of power. Where there are no direct holdings, under IFRS 10, an

investor (as defined in IFRS 10) should consider other evidence of power and ability to unilaterally direct an investee’s (as defined

in IFRS 10) relevant activities. In view of the contractual agreements and the guidance in IFRS 10, notwithstanding that the Company has

no direct or indirect ownership of Focus, it has sufficient rights to unilaterally direct the relevant activities (a concept known as

“de facto control”), mainly due to the following:

| 1) |

the Company receiving economic benefits from Focus (and the terms of the Commercial Agreements (as defined herein) cannot be changed

without the approval of the Company); |

| 2) |

the Company having the option to purchase the divested 74% interest in Focus held by Oren Shuster, the Chief Executive Officer, director

and a promoter of the Company, and Rafael Gabay, a former consultant director, a former consultant and a promoter of the Company;

|

| 3) |

Messrs. Shuster and Gabay each being a director of Focus (while Mr. Shuster concurrently being a director, officer and substantial

shareholder of the Company and Mr. Gabay concurrently being a substantial shareholder of the Company); and |

| 4) |

the Company providing management and support activities to Focus through the Services Agreement (as defined herein). |

Accordingly, under IFRS 10, the Company has “de facto control” over Focus,

and therefore consolidates the financial results of Focus in the Company’s financial statements.

Any failure of the Company or Messrs. Oren Shuster and Rafael Gabay to maintain “de

facto control” over Focus as defined under IFRS 10 could alter the Company’s consolidation model, potentially resulting in

a material adverse effect on the business, results of operations and financial condition of the Company.

For the period ended December 31, 2024, the Company analyzed the terms of the definitive

agreements with each of its Consolidated Entities (as defined within IFRS 10) in accordance with accounting criteria IFRS 10. Viewed as

effectively exercising control over their Consolidated Entities, the Company consolidate the financial results of the Consolidated Entities

as of the date of signing each such definitive agreement.

The

regulatory authorities in Israel may determine that the Company is in contravention of Israeli cannabis regulations

There is a risk that regulatory authorities in Israel may determine that the Company

is in contravention of Israeli cannabis regulations. Namely, prior approval of the Israeli Medical Cannabis Agency (“IMCA”)

is required for any shareholder owning 5% or more of an Israeli company licensed to engage in cannabis-related activities. Any contravention

of Israeli cannabis regulations could jeopardize the good standing of the Company’s licenses. Such a determination may adversely

affect the Company’s ability to conduct sales and marketing activities and could have a material adverse effect on the Company’s

business, operating results or financial condition.

The

Company is subject to governmental regulations in the markets in which it operates and any delays in obtaining, or failure to obtain regulatory

approvals could significantly delay the development of markets and products and could have a material adverse effect on the business,

results of operations, financial condition and prospects of the Company

Israel – MOH Regulation

Laws and regulations, applied generally, grant government agencies and self-regulatory

bodies broad administrative discretion over the activities of the Israeli Subsidiaries and Focus, which can include the power to limit

or restrict business activities, the import and export of cannabis products and the imposition of additional quality criteria and disclosure

requirements on the products and services provided by Israeli Subsidiaries and Focus. Achievement of the Israeli Subsidiaries and

Focus business objectives are contingent, in part, upon compliance with regulatory requirements enacted by these governmental authorities

and obtaining all regulatory approvals, where necessary, for the production and sale of its products.

The Company cannot predict the time required for the Israeli Subsidiaries or Focus

to secure all appropriate regulatory approvals for the products and activity, or the extent of testing and documentation that may be required

by governmental authorities. Any delays in obtaining, or failure to obtain regulatory approvals would significantly delay the development

of markets and products and could have a material adverse effect on the business, results of operations, financial condition and prospects

of the Company.

Failure to comply with the laws and regulations applicable to its operations may lead

to possible sanctions including the revocation or imposition of additional conditions on licenses to operate the Israeli Subsidiaries and/or

the Focus business, the suspension or expulsion from a particular market or jurisdiction or

of its key personnel, and the imposition of fines and censures. To the extent that there are changes to the existing laws and regulations

or the enactment of future laws and regulations that affect the sale or offering of the Israeli Subsidiaries and/or Focus

products or services in any way, this could have a material adverse effect on the business, results of operations, financial condition

and prospects of the Company.

Germany – BfArM Regulation

On March 10, 2017, the German federal government enacted bill Bundestag- Drucksache

18/8965 – Law amending narcotics and other regulations that amended existing narcotics legislation to recognize cannabis as a form

of medicine and allow for the importation and domestic cultivation of medical cannabis products. Under the subsequent updated legislation,

cannabis was listed in Annex 3 to the Federal Narcotics Act (“BtMG”) as a “marketable

narcotic suitable for prescription” until the Medical Cannabis Act (MedCanG) came into force on 1 April 2024. Since then, medical

cannabis has no longer been subject to the BtMG but to the MedCanG. With regard to medical cannabis, the cultivation, production, distribution,

exportation, transit and importation are currently legal in Germany, subject to regulations and licensing requirements. At the same time

as the MedCanG, the Consumer Cannabis Act (KCanG) also came into force on 1 April 2024. Operations involving adult-use recreational cannabis

products became legal under certain conditions defined in the KCanG. Until the KCanG came into force, legalization in Germany applied

only to cannabis for medicinal purposes under state control in accordance with the Narcotic Convention. This development has its origins

in the fact that the still incumbent German government (Elections were held at the end of February 2025, coalition negotiations are currently

being considered, a new government will probably be formed during April 2025. It remains to be seen whether a new coalition government

will bring about changes with regard to medical cannabis and/or cannabis for consumption.) has declared in the coalition agreement at

the end of 2021 its intention to open up the German market also in the adult-use recreational market. In October 2022, a key points paper1

on the controlled supply of cannabis to adults for consumption purposes, although a restructuring of the existing regulatory framework

on cannabis in general was also discussed, published by the cabinet, which was submitted to the European Union Commission for a preliminary

legal examination. In this respect, the Federal Government issued a declaration of interpretation with regard to existing international

agreements governing the adult-use recreational cannabis usage and submitted a draft law to the European Union Commission within the framework

of a notification. After a long political debate, the German Bundestag approved the federal government's draft law "on the controlled

use of cannabis" (BT Drs. 20/87042, BT Drs. 20/87633,

BT-Drs. 20/104264) on Friday, 23 February 2024. The draft

law (BT Drs. 20/8704) then came into force on 1 April 2024. An adjustment has already been made by Article 1 of the Act of 20 June 2024

(BGBl. 2024 I No. 207)5. Some components of the KCanG,

which deal with so-called consumer cannabis, came into force on 1 July 2024 (such as the possibility to apply for a permission to grow

by and distribute recreational cannabis to members of a cultivation association. The entry into force of the law also had direct consequences

for medical cannabis, which is the subject matter of Art. 2 (Medical Cannabis Act - MedCanG) and 3 (BtMG) of the law. Since the KCanG

and MedCanG came into force, cannabis is no longer a narcotic by definition and is therefore no longer subject to the BtMG. The definition

in Annex 3 of the BtMG was be replaced by that in Section 2 MedCanG: "Cannabis for medical purposes: plants, flowers and other parts of

plants belonging to the genus Cannabis that are grown for medical purposes under state control in accordance with Articles 23 and 28(1)

of the Single Convention on Narcotic Drugs of 1961 of 30 March 1961 (Federal Law Gazette 1973 II p. 1354), as well as delta-9-tetrahydrocannabinol

including dronabinol and preparations of all the aforementioned substances". However, the narcotics regulations were replaced by comparable

regulations and authorisations. The Federal Institute for Drugs and Medical Devices (BfArM) remains responsible for the latter as a higher

federal authority. From a regulatory perspective, medical cannabis remains a medicinal product or an active pharmaceutical ingredient,

meaning that the requirements under medicinal product law will remain in place. As a result, the marketing of irradiated products continues

to require a marketing authorisation in accordance with the Ordinance on Medicinal Products Treated with Radioactive or Ionising Radiation

(AMRadV). Only the narcotics licence pursuant to Section 3 BtMG is replaced by a new licence pursuant to the Medical Cannabis Act (MedCanG)

(see Section 1), which, however, largely corresponds to the previous provisions of the BtMG regarding the application process and general

regulations. However, there are the following differences that are new since the entry into force: Medical cannabis no longer has to be

stored and transported like a narcotic. The corresponding safety precautions no longer apply, meaning that compliance with the provisions

of pharmaceutical law is sufficient. The so-called semi-annual reports are replaced by annual reports. The requirements for the person

responsible for medical cannabis are slightly reduced compared to those for narcotics. A prescription of medical cannabis is possible

without the need to use the form for prescription for narcotics. A normal prescription is sufficient.

1 https://www.bundesgesundheitsministerium.de/fileadmin/Dateien/3_Downloads/Gesetze_und_Verordnungen/GuV/C/Kabinettvorlage_Eckpunktepapier_Abgabe_Cannabis.pdf

(in German language).

2 https://dserver.bundestag.de/btd/20/087/2008704.pdf

(in German language).

3 https://dserver.bundestag.de/btd/20/087/2008763.pdf

(in German language).

4 https://dserver.bundestag.de/btd/20/104/2010426.pdf

(in German language).

5 https://www.recht.bund.de/bgbl/1/2024/207/VO.html.

Medical cannabis in Germany must comply with the corresponding monographs of the German

and European pharmacopoeia. Currently, there are still (non-harmonised) national pharmacopoeial monographs for cannabis flowers (e.g.

in the German Pharmacopoeia (Deutsches Arzneibuch (DAB)) and cannabis extracts (DAB) in the EU. The Committee on Herbal Medicinal Products

(HMPC) as the European Medicines Agency’s (EMA) committee responsible for compiling and assessing scientific data on herbal substances,

preparations and combinations, announced that in view of uniform EU quality requirements (including with respect to import and export

of cannabis), further European Pharmacopoeia (Ph. Eur.) Cannabis monographs are in preparation.

The European Pharmacopoeia (Ph. Eur.) Suppl. 11.5 is published and contains the new

Ph. Eur. Monograph on cannabis flowers and the new Ph. Eur. Monograph on Cannabidiol (CBD). With the entry into force of Suppl. 11.5 of

the national edition of the European Pharmacopoeia (Ph. Eur.) on April 1, 2025, the monograph 'Cannabis flowers / Cannabis flos [3028]'

contained therein will be legally binding from this date. The previous monograph 'Cannabis flowers' of the German Pharmacopoeia is scheduled

for deletion from the next edition (DAB 2025). The DAB 2025 is expected to come into force on July 01, 2025. The new monograph on cannabis

flowers includes Starting materials for the production of extracts, medicinal products that can be prescribed as such (herbal medicinal

products) that are taken by patients by inhalation or oral administration. There are not entirely irrelevant changes compared to the German

monograph.

All BtMG permit applications had to specify the strains and estimated quantities of

medical cannabis involved and any subsequent changes had to be reported to the Federal Opium Agency of Germany, whereby varieties and

quantities no longer appear on the permit, even if these are to be specified in the application. The same applies regarding Sections 7,

8 MedCanG in relation to the authorisation to trade in medical cannabis, although it is now apparent that no expected annual quantities

are to be specified. However, it can be assumed that the BfArM nevertheless enquire about these due to the (albeit somewhat reduced compared

to the BtMG) reporting obligations in Sections 16 and 17 MedCanG and the Foreign Narcotics Trade Regulation, which remains applicable

(see Section 14 MedCanG).

CBD is neither a real subject to the KCanG nor to the MedCanG. Only in Section 1 No.

3 KCanG is there a definition, in Section 1 No. 8 b) KCanG the exemption of CBD from the term cannabis and in Section 2 para. 2 No. 1

KCanG the exemption from the prohibition of extraction of the cannabis plant, which permits the extraction of CBD, even if it does not

contain any further regulations on CBD in isolation. With regard to synthetic CBD, a different set of regulations is important: the handling

of cannabimimetics/synthetic cannabinoids is prohibited in accordance with Section 2 of the Annex in conjunction with Section 3 of the

New Psychoactive Substances Act (NpSG). Product-specific regulations relating to CBD can be found in other regulations. Thus, Annex 1

of the Ordinance on the Prescription of Medicinal Products stipulates that CBD is in principle subject to prescription but does not specify

a minimum quantity or a specific dosage form. If we look at the food sector, a distinction is made between products that naturally contain

CBD and those that consist of or contain extracted CBD; the European Commission considers the latter to be novel foods under Regulation

(EU) 2015/2283, which require authorisation before being placed on the market. Although applications for such authorisation have been

submitted, the European Commission believes that they contain at least insufficient data on safety in food use, meaning that none of the

applications can currently lead to authorisation. Against this background, various products containing CBD can be found on the German

market. There are currently various court decisions that problematise CBD in foods (especially food supplements) and in cosmetics (especially

mouth oil). On the one hand, CBD is regarded as a potential active pharmaceutical ingredient (API) to be used in medicinal products or

as a novel food subject to authorisation and therefore unsuitable for a safe use in a foodstuff, and on the other hand as unsuitable for

cosmetic use in the mouth, as CBD would ultimately be consumed in this case (like a foodstuff and therefore to be regarded as foodstuff).

CBD is therefore sometimes declared as a flavoring in foods, as flavorings are excluded from the scope of the Novel Food Regulation. Nevertheless,

there are already decisions that exclude suitability as a flavoring in individual cases.

Cultivation in Germany

and Distribution of Medical Cannabis Cultivated in Germany

The Past:

The Federal Opium Agency of Germany’s Federal Institute for Drugs and Medical

Devices (“BfArM”) formed a cannabis division (the “Cannabis Agency”) to

oversee cultivation, harvesting, processing, quality control, storage, packaging and distribution to wholesalers, pharmacists and manufacturers.

The Cannabis Agency also regulated pricing of German-produced medical cannabis products and served as an intermediary of medical cannabis

product sales between manufacturers, wholesalers and pharmacies on a non-profit basis so far. In late 2018, the Cannabis Agency issued

a call for tenders to award licenses for local medical cannabis cultivation and distribution of German-cultivated medical cannabis products

(the “German Local Tender”). The Cannabis Agency served as an intermediary in the supply chain between such cultivation and

distribution. In April 2019, three licenses for local cultivation were granted. In consequence three companies in Germany received the

permission to cultivate on behalf of the Cannabis Agency of the BfArM.

Current Situation:

Since the entry into force of the MedCanG, the granting of licences for domestic cultivation

is no longer subject to tendering but governed by §§ 4 et seq. MedCanG. The previously time-consuming tendering and awarding

of contracts for the domestic cultivation of cannabis for medical purposes by the Cannabis Agency and the subsequent purchase and distribution

of the domestic harvest yields by the Cannabis Agency from the economic operators determined during the tendering procedure are no longer

necessary. Ultimately, only the corresponding licences in accordance with the MedCanG and - from implementation of manufacturing steps

relevant under pharmaceutical law - the AMG are required in compliance with the respective conditions and the associated regulations.

Import volumes and procedures

regarding Medical Cannabis

The past and present regime permits the importation of cannabis plants and plant parts

for medicinal purposes under state control subject to the requirements under the Narcotic Convention, according to which, Germany must

estimate the expected demand of medical cannabis products for medical and research purposes for the following year and report such estimates

to the International Narcotics Control Board.

As a prerequisite to obtaining a German import license, the supplier must grow and

harvest in compliance with EU-GACP-Guidelines and manufacture in compliance with EU-GMP-Guidelines and certifications, or alternatively,

it is a pure EU-GACP product, and the EU-GMP manufacturing steps then take place in Germany. With regard to imports from third countries

and the associated testing and assessment of EU GMP compliance, the relevant pharmaceutical regulations are in force, which also provide

for on-site inspections by the EU authorities, provided that no MRA or similar is in force for the specific product type. All medical

cannabis products imported to Germany must derive from plant material cultivated in a country whose regulations comply with Art. 23 and

38 of the Narcotic Single Convention and must comply with the relevant and applicable monographs described in the German and European

pharmacopeias.

Dispensing Exclusively

via Pharmacies

Medical cannabis products imported pursuant to an import license under the MedCanG

and AMG permits are sold exclusively to pharmacies for final dispensing to patients on a prescription basis as ‘magistral preparations’,

a term used in Europe to refer to medical products prepared in a pharmacy in accordance with a medical prescription for an individual

patient. Magistral preparations require certain manufacturing steps in the pharmacy. Such manufacturing steps of the pharmacist typically

include the testing and dosing of pre-packaged cannabis inflorescences (typically referred to as “flos”), medical cannabis

products for oral administration (dronabinol), medical cannabis products for inhalation upon evaporation, and medical cannabis-infused

teas. In addition to magistral preparations, medical cannabis products are also marketable as pre-packaged, licensed drugs (e.g. Sativex®).

The

Company’ ability to produce, store, import, distribute and sell cannabis and derivative products in Israel and Germany is dependent

on licensing and any failure to maintain the respective licenses would have a material adverse impact on the business, financial condition

and operating results of the Company

Israel – Reliance on the Israeli Licenses

The Company’s ability to produce, store, import, distribute and sell cannabis

in Israel is dependent on the Israeli Subsidiaries and Focus maintaining the Israeli Licenses with the IMCA. Failure to comply with the

requirements or any failure to maintain the Israeli Licenses would have a material adverse impact on the business, financial condition

and operating results of the Company. There can be no guarantees that the IMCA will extend or renew any of Israeli Licenses as necessary

or, if it extended or renewed, that any of the Israeli Licenses will be extended or renewed on the same or similar terms. Should the IMCA not

extend or renew any of Israeli Licenses or should it renew any of the Israeli Licenses on different terms, the business, financial condition

and results of the operations of the Company would be materially adversely affected.

Germany – Reliance on the Adjupharm Licenses

The Company’s ability to produce and distribute cannabis through Adjupharm’s

certification as an EU-GMP and EU-GDP producer and distributor in Germany with wholesale, narcotics handling, manufacturing, procurement,

storage and distribution authority is granted by German regulatory authorities. Failure to comply with the requirements of the BfArM issued

licenses or any failure to maintain their respective licenses would have a material adverse impact on the business, financial condition

and operating results of the Company.

The

Company relies on licensed facilities in Israel and Germany to conduct its operations and any adverse changes or developments affecting

such facilities could have a material adverse effect on the Company’s business, financial condition, results of operations and prospects

Israel – Reliance on the Company’s Facilities

The Israeli Facilities

The Israeli Licenses are specific to each respective facility holding such license

and therefore both the license and the facility must remain in good standing for each of the Company’s pharmacies (Virona and R.A

Pharm Yarok, together the “Israeli Pharmacies”) to be able to conduct the Israeli cannabis

activities authorized thereunder (the facilities of the Israeli Pharmacies together” “Israeli

Facilities”). Adverse changes or developments affecting the Israeli Facilities, including but not limited to the failure

to maintain all requisite regulatory and ancillary permits and licenses, the failure to comply with state or municipal regulations, or

a breach of security, could have a material adverse effect on the Company’s business, financial condition, results of operations

and prospects.

Any breach of any lease agreement relevant to the operations of the Israeli Facilities

or any failure to renew such lease agreements, on materially similar or more favorable terms, may also have a material adverse effect

on the Company’s business, financial condition, results of operations and prospects.

Germany – Reliance on the German Logistics Center

The Company’s EU-GMP logistics centre in Germany (the “German Logistics

Center”) allows Adjupharm to manage all aspects of its supply chain including the production, the repackaging and distribution

of bulk medical cannabis. Any breach of regulatory requirements, including any failure to comply with recommendations or requirements

arising from inspections by government regulators, could also have an impact on Adjupharm’s ability to maintain the licenses and/or

keep the German Logistics Center in good standing, and to continue operating it under the licenses, could have a material adverse effect

on the Company’s business, financial condition, results of operations and prospects.

In

Germany and in Israel, the Company relies on various supply and distribution agreements with third-parties, such as cannabis cultivators,

packaging suppliers, service providers and distribution partners. The loss of such suppliers and/or service providers and/or distributors

and/or their timely service would have a material adverse effect on the Company’s business and operational results

Israel – Supply, Manufacture and Distribution Agreements

The Israeli Subsidiaries rely on and are substantially dependent on various supply

agreements with third-party cannabis cultivators in Israel and Canada, imported cannabis products, manufacture and packaging agreements

and distribution agreements to fulfill the supply requirements of its distribution and sales agreements with pharmacies in the Israeli

medical cannabis market. The Israeli Subsidiaries acquire cannabis from third parties in amounts sufficient to operate its business. However,

there can be no assurance that there will continue to be a supply of cannabis available for the Company to purchase to operate or expand.

Additionally, the price of cannabis and other inputs may rise which would increase the cost of goods. If any suppliers fail to supply

any contracted materials to the Israeli Subsidiaries, the Israeli Subsidiaries may fail to meet purchase commitments from their distribution

partners. If the Company were unable to acquire the cannabis or other inputs required to operate or expand or to do so on favorable terms

or fail to maintain the manufacture agreements with IMC-GMP manufacture companies, it could have a material adverse impact on the Company’s

business, financial condition and results of operations. If any of the Company’s suppliers fails to provide inputs meeting the Company’s

quality standards, it may need to source cannabis or other inputs from other suppliers, which may result in additional costs and delay

in the delivery of its products and services to distributors, pharmacies and patients. There is no assurance that suppliers will be able

to supply and deliver the required materials to the Company in a timely manner or that the materials they supply to the Company will not

be defective or substandard. Any delay in the delivery of materials, or any defect in the materials, supplied to the Company may materially

and adversely affect or delay its production schedule and affect its product quality. Consequently, the Company relies on the suppliers

of such supply agreements to provide necessary cannabis products to the Israeli Subsidiaries. If the Company cannot secure cannabis of

similar quality and at reasonable prices from alternative suppliers in a timely manner, or at all, the Israeli Subsidiaries may

not be able to deliver its products to distributors, pharmacies or patients on time with the required quality. The various suppliers and

distributors may elect, at any time, to breach or otherwise cease to participate in supply, service or distribution agreements, or other

relationships, upon which the Company’s operations rely. Loss of its suppliers, service providers or distributors or their timely

service would have a material adverse effect on the Company’s business and operational results.

Germany – Reliance on Supply and Distribution Agreements

in Germany

Adjupharm relies on its sales and distribution agreements to supply IMC-branded products

to distribution partners in Germany, which are then distributed to German pharmacies for sales to medical cannabis patients and on direct

sales by Adjupharm of IMC-branded products to German pharmacies.

Adjupharm relies on supply agreements with cannabis cultivators and producers to meet

the demands of their respective sales agreements with distribution partners and pharmacies. Consequently, the Company relies on the suppliers

of such supply agreements to provide necessary cannabis products to Adjupharm. If any suppliers fail to supply any contracted materials

to Adjupharm, Adjupharm may fail to meet purchase commitments from their distribution partners and this could result a material adverse

effect on the Company’s business, financial and operational results.

There

can be no assurances that income tax laws or the interpretation thereof in any of the jurisdictions in which the Company operates will

not be changed or interpreted or administered in a manner which adversely affects the Company and its shareholders

The Company is subject to the provisions of the ITA12 and to review by CRA13. The

Company files its annual tax compliance based on its interpretation of the Income Tax Act (the

“ITA”) and Canada Revenue Agency’s (the “CRA”)

guidance. There is no certainty that the returns and tax position of the Company will be accepted by CRA as filed. Any difference between

the Company’s tax filings and CRA’s final assessment could impact the Company’s results and financial position.

There can be no assurance that income tax laws or the interpretation thereof in any

of the jurisdictions in which the Company operates will not be changed or interpreted or administered in a manner which adversely affects

the Company and its shareholders. In addition, there is no assurance that CRA will agree with the manner in which the Company calculates

taxes payable or that any of the other tax agencies will not change their administrative practices to the detriment of the Company or

its shareholders.

If

operational cash flows continue to be negative, the Company may be required to fund future operations with alternative financing options

such as offerings of shares

During the year ended December 31, 2024, the Company had negative cash flows from

operating activities. There is no assurance that the Company will generate positive cash flows from its future operating activities. If

operational cash flows continue to be negative, the Company may be required to fund future operations with alternative financing options

such as offerings of shares.

The

Company may not be able to secure the funds necessary to implement its strategies, which could cause significant delays in carrying out

business objectives or result in a material adverse effect on the Company’s business, financial condition, operational results and

prospects

There is no assurance that the Company will be able to secure the funds necessary

to implement its strategies. Additional debt incurred by the Company from engagements such as major acquisitions may cause the Company’s

debt level to increase and result in difficulties in completing or negotiating future debt financings. Any triggering of credit defaults

or failure to raise capital by the Company may cause significant delays in carrying out business objectives or result in a material adverse

effect on the Company’s business, financial condition, operational results and prospects.

Increased

competition could materially and adversely affect the business, financial condition and results of operations of the Group

There is potential that the Group will face intense competition from other companies

or groups of companies, some of which can be expected to have more financial resources, industry, manufacturing and marketing experience

than the Group. Because of the early stage of the industry in which the Group operates, as well as evolving legislation and governmental

initiatives in several jurisdictions, the Group expects to face additional competition from new entrants in the jurisdictions in which

it currently operates or is contemplating operations. If the number of users of medical cannabis products in Israel and Europe increases,