UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________

FORM

_____________________

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of Earliest Event Reported):

_____________________

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification No.) |

|

|

||

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Coeptis Therapeutics Holdings, Inc.

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) |

Name of each exchange on which registered | ||

|

|

|

|

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

On April 24, 2026, CP Merger Sub, Inc., a Wyoming corporation (“Merger Sub”) and wholly owned direct subsidiary of Coeptis Therapeutics Holdings, Inc., a Delaware corporation (“Coeptis”), merged with and into Z Squared Inc., a Wyoming corporation (“Z Squared”), with Z Squared surviving as a wholly owned subsidiary of Coeptis (the “Merger”). The Merger was completed on April 24, 2026 (the “Closing Date”). In connection with the Merger, pursuant to the Articles of Merger, the surviving corporation changed its name to Z Squared OpCo Inc. (“OpCo”). Coeptis is the parent holding company of OpCo and, following the Merger, on April 27, 2026, pursuant to an amendment to Coeptis’ certificate of incorporation, Coeptis changed its name to Z Squared Inc., a Delaware corporation, and is referred to herein as “Pubco”. References to “we,” “us,” “our,” and “the company” refer to Pubco unless the context otherwise requires.

These forward-looking statements are only predictions, are uncertain and involve substantial known and unknown risks, uncertainties and other factors which may cause our (or our industry’s) actual results, levels of activity or performance to be materially different from any future results, levels of activity or performance expressed or implied by these forward-looking statements. The “Risk Factors” section of this current report sets forth detailed risks, uncertainties and cautionary statements regarding our business and these forward-looking statements.

We cannot guarantee future results, levels of activity or performance. You should not place undue reliance on these forward-looking statements, which speak only as of the date that they were made. These cautionary statements should be considered with any written or oral forward-looking statements that we may issue in the future. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to reflect actual results, later events or circumstances or to reflect the occurrence of unanticipated events.

| i |

EXPLANATORY NOTE

On April 24, 2026, CP Merger Sub, Inc., a Wyoming corporation (“Merger Sub”) and wholly owned direct subsidiary of Coeptis Therapeutics Holdings, Inc., a Delaware corporation (“Coeptis”), merged with and into Z Squared Inc., a Wyoming corporation (“Z Squared”), with Z Squared surviving as a wholly owned subsidiary of Coeptis (the “Merger”). The Merger was completed on April 24, 2026 (the “Closing Date”). In connection with the Merger, pursuant to the Articles of Merger, the surviving corporation changed its name to Z Squared Opco Inc. (“OpCo”). Coeptis is the parent holding company of OpCo and, following the Merger, on April 27, 2026, pursuant to an amendment to Coeptis’ certificate of incorporation, Coeptis changed its name to Z Squared Inc., a Delaware corporation, and is referred to herein as “Pubco”. References to “we,” “us,” “our,” and “the company” refer to Pubco unless the context otherwise requires.

This Current Report contains summaries of the material terms of various agreements executed in connection with the transactions described herein. The summaries of these agreements are subject to, and are qualified in their entirety by, reference to these agreements, all of which are incorporated herein by reference.

This Current Report is being filed in connection with a series of transactions consummated by the company and certain related events and actions taken by the company.

This current report responds to the following items on Form 8-K:

| Item 2.01 | Completion of Acquisition or Disposition of Assets |

| Item 5.01 | Changes in Control of the Registrant |

| Item 5.02 | Departure of Directors or Principal Officers; Election of Directors; Appointment of Principal Officers; Compensatory Arrangements of Certain Officers |

| Item 5.03 | Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year |

| Item 9.01 | Financial Statements and Exhibits |

| ii |

TABLE OF CONTENTS

| iii |

| Item 2.01. | Completion of Acquisition or Disposition of Assets |

THE MERGER AND RELATED TRANSACTIONS

The Merger

On April 25, 2025, Coeptis Therapeutics Holdings, Inc., a Delaware corporation (“Coeptis”), CP Merger Sub, Inc., a Wyoming corporation and wholly owned direct subsidiary of Coeptis (“Merger Sub”), and Z Squared Inc., a Wyoming corporation (“Z Squared”), entered into an Agreement and Plan of Merger, as may be amended from time to time (the “Merger Agreement”), pursuant to which, subject to the satisfaction or waiver of the conditions set forth in the Merger Agreement, Merger Sub merged with and into Z Squared, with Z Squared surviving as a wholly owned subsidiary of Coeptis (the “Merger”). The Merger was completed on April 24, 2026 (the “Closing Date”). In connection with the Merger, pursuant to the Articles of Merger, the surviving corporation changed its name to Z Squared OpCo Inc. (“OpCo”). Coeptis is the parent holding company of OpCo and, following the Merger, on April 27, 2026, pursuant to an amendment to Coeptis’ certificate of incorporation, Coeptis changed its name to Z Squared Inc., a Delaware corporation, and is referred to herein as “Pubco”. References to “we,” “us,” “our,” and “the company” refer to Pubco unless the context otherwise requires.

At the effective time of the Merger (the “Effective Time”), each share of Z Squared’s common stock, par value $0.001 (the “Z Squared Common Stock”) outstanding immediately prior to the Effective Time was converted into the right to receive one share of Coeptis’ common stock, par value $0.0001 per share (the “Coeptis Common Stock”), which shares of Coeptis Common Stock were issued at the Effective Time as consideration for the Merger, as calculated pursuant to the terms set forth in the Merger Agreement.

As consideration for the Merger, upon the consummation of the Merger (the “Closing”), the Z Squared stockholders collectively received from Coeptis, in the aggregate, 43,877,497 shares of Coeptis Common Stock, representing the Applicable Percentage (as defined in the Merger Agreement) of Coeptis’ issued and outstanding shares of Coeptis Common Stock as calculated on a fully-diluted basis, as provided in the Merger Agreement (the “Merger Consideration”).

The rights attendant to the Coeptis Common Stock are set forth in the Pubco’s Certificate of Incorporation, as amended to date, a copy of which is attached hereto as Exhibits 3.1 and 3.2.

On April 27, 2026, concurrent with the Merger, we amended our certificate of incorporation to change the name of the company from Coeptis Therapeutics Holdings, Inc. to “Z Squared Inc.” The Certificate of Incorporation, as amended, is included as Exhibits 3.1 and 3.2 hereto.

Commencing on April 27, 2026, the trading symbol for the Pubco Common Stock, which is currently listed on the Nasdaq Global Market, changed from “COEP” to “ZSQR.”

The Merger will be treated as a reverse merger of Coeptis for financial accounting purposes. The historical financial statements of Coeptis before the Merger will be replaced with the historical financial statements of OpCo before the Merger in all future filings with the Securities and Exchange Commission (the “SEC”).

Following the Closing Date, our board of directors consists of five members. On the Closing Date, pursuant to the Merger Agreement, all of the then-serving directors and executive officers of Coeptis resigned at or prior to the Effective Time. Prior to the Effective Time but to be effective immediately following the closing of the Merger and ratification by the new Pubco Board, the Coeptis Board elected five designees selected by Z Squared to serve as members of the board of directors of Pubco effective upon consummation of the Merger. The composition of the board of directors of Pubco following the Effective Time in the aggregate satisfies the requisite independence requirements, as well as the sophistication and independence requirements for the required committees, pursuant to Nasdaq listing requirements. As of the Effective Time, the board of directors of Pubco is as follows:

| David Halabu | Chief Executive Officer, President and Director | |

| Adam Sohn | Director | |

| Bryan Fuerst | Director | |

| Kenneth Cooper | Director | |

| Michelle Burke | Director and Chief Operating Officer |

| 1 |

The executive officers of Pubco following the consummation of the Merger are: David Halabu (Chief Executive Officer); Michelle Burke (Chief Operating Officer); and Brian Cogley (Chief Financial Officer).

The parties have taken all actions necessary to ensure that the Merger is treated as a tax-free exchange under Section 368(a) of the Internal Revenue Code of 1986, as amended.

On April 15, 2026, Coeptis undertook a reorganization of its assets related to its biopharmaceutical operations (other than its assets with respect to GEAR Therapeutics, Inc.) to reorganize such assets to be held directly or indirectly by a new subsidiary Coeptis Holdings, Inc (“CHI”). Specifically, and in connection therewith, Coeptis entered into two assignment and assumption agreements and a contribution agreement pursuant to which substantially all of such assets and liabilities were assigned/contributed to CHI, in exchange for the issuance to Coeptis of a 100% ownership interest in CHI. Further, as of immediately prior to the consummation of the Merger, Coeptis declared a one-for-one pro rata dividend of its ownership interest in CHI to the stockholders of Coeptis existing as of January 2, 2026 (the record date for Coeptis’ most recent shareholder meeting), which pro rata distribution was effected prior to the closing of the Merger.

In addition, in exchange for Coeptis keeping in its organization on a post-Merger basis its subsidiary GEAR Therapeutics, Inc, Coeptis issued to CHI 1,000,000 shares of Coeptis’ common stock and executed and delivered to CHI an option agreement that grants CHI a limited time option exercisable in its discretion to acquire GEAR Therapeutics, Inc. for the fair market value of GEAR Therapeutics, Inc. at the time of exercise. The option becomes exercisable on October 24, 2026, is exercisable for a period of twenty-four (24) months from the date on which such option becomes exercisable, and contemplates that the exercise price for the option may be paid at the option of CHI in cash, by return of shares of Coeptis common stock based on the value of the Coeptis common stock at the time of exercise of the option, or a combination thereof.

Current Ownership

Immediately after giving effect to the Merger, our issued and outstanding securities as of the Closing Date of the Merger are 51,431, 493 shares of Pubco Common Stock .

Accounting Treatment; Change of Control

The Merger is being accounted for as a “reverse merger,” and OpCo is deemed to be the acquirer in the reverse merger. Consequently, the assets and liabilities and the historical operations that will be reflected in the financial statements prior to the Merger will be those of OpCo, and the consolidated financial statements after completion of the Merger will include the assets and liabilities of OpCo, historical operations of OpCo and operations of OpCo from the Closing Date of the Merger. Except as described in the previous paragraphs, no arrangements or understandings exist among present or former controlling stockholders with respect to the election of members of our board of directors and, to our knowledge, no other arrangements exist that might result in a change of control of Pubco. Further, as a result of the issuance of the shares of Coeptis Common Stock pursuant to the Merger, a change in control of the Pubco occurred as of the date of consummation of the Merger.

| 2 |

DESCRIPTION OF BUSINESS

Immediately following the Merger, the business of OpCo became the business of Pubco. Because the Merger is being accounted for as a “reverse merger,” and OpCo is deemed to be the acquirer in the reverse merger, the business description below is a description of Pubco’s business based on OpCo’s operations.

Corporate Information

Pubco is a public corporation, and its securities are traded on the Nasdaq Global Market under the ticker (ZSQR). The principal executive offices of Pubco are located at 550 South Andrews Ave. Ste. #700, Fort Lauderdale, FL 33301, which we lease, and its telephone number is (954) 400-9994.

Company History

General. Coeptis was originally incorporated in the British Virgin Islands on November 27, 2018, under the name Bull Horn Holdings Corp. On October 27, 2022, Bull Horn Holdings Corp. domesticated from the British Virgin Islands to the State of Delaware. On October 28, 2022, in connection with the closing of the merger, Coeptis changed its corporate name from Bull Horn Holdings Corp. to “Coeptis Therapeutics Holdings, Inc.”

The 2021 Recapitalization Transaction

Coeptis Pharmaceuticals, LLC was formed on July 12, 2017 as a Pennsylvania multi-member limited liability company. On December 1, 2018, the members of LLC contributed their interest to a newly formed corporation, Coeptis Pharmaceuticals, Inc. As of December 1, 2018, the LLC became a disregarded single-member limited liability company which is wholly owned by the newly formed corporation. On February 12, 2021, Vinings Holdings, Inc., a Delaware corporation (“Vinings”), merged with and into Coeptis Pharmaceuticals, Inc. On July 12, 2021, Vinings legally changed its name from Vinings Holdings, Inc. to Coeptis Therapeutics, Inc. Coeptis was the surviving corporation of that merger. As a result of the merger, Vinings acquired the business of Coeptis and continued the existing business operations of Coeptis as a wholly owned subsidiary. The merger was treated as a recapitalization of the company for financial accounting purposes. The historical financial statements of Vinings before the merger were replaced with the historical financial statements of Coeptis before the Merger in all future filings with the SEC.

The 2022 Merger Transaction. On October 28, 2022, a wholly owned subsidiary of Bull Horn Holdings Corp., merged with and into Coeptis Therapeutics, Inc., with Coeptis Therapeutics, Inc. as the surviving corporation of the 2022 merger. As a result of the 2022 merger, Coeptis acquired the business of Coeptis Therapeutics, Inc., which Coeptis operated as a wholly owned subsidiary.

The 2026 Merger Transaction. As described in more detail above, on April 24, 2026, Merger Sub merged with and into Z Squared, with Z Squared surviving as a wholly owned subsidiary of Coeptis. On April 27, 2026, Coeptis Therapeutics Holdings, Inc. changed its name to “Z Squared Inc.”

DESCRIPTION OF THE BUSINESS CONDUCTED BY OPCO

Overview

OpCo is a development-stage, vertically integrated cryptocurrency mining firm focused on optimized, multi-asset digital mining. OpCo will operate advanced mining facilities strategically distributed across North America (specifically North Carolina, South Carolina, and Iowa).

Following the acquisition of mining assets from BSG Series CM, LLC, as described under “Material Agreements” herein, OpCo will mine major cryptocurrency assets Dogecoin (DOGE) and Litecoin (LTC). OpCo’s mining operations are expected to span six locations across South Carolina, Iowa, and North Carolina, with 9,800 machines to be deployed, including 8,228 L7s, 849 L9s, and 723 DG1+ units and precise strategies tailored for each asset and mining algorithm (e.g., SHA-256, Scrypt, kHeavyHash).

| 3 |

Key elements of OpCo’s operations will include:

| · | Fleet Optimization: Continuous monitoring and rotation of miners based on performance, age, and market conditions. | |

| · | Repair & Spare Parts Program: In-house process for tracking, repairing, and recycling units, maximizing hardware lifecycle and reducing capital waste. | |

| · | Power Strategy: Dynamic response to curtailment and seasonal electricity rates, optimizing cost per kilowatt-hour and maintaining uptime. Energy costs are expected to be uniform at $0.088 per kWh, as set forth in the master Services Agreement with Minting Dome, and no material cost differences are anticipated at this stage. | |

| · | Performance Reporting: Custom-built dashboards for real-time visibility into Hash Rate, unit status, revenue per machine, and operational health. |

Mining Overview

OpCo will mine major cryptocurrency assets Dogecoin (DOGE) and Litecoin (LTC). It manages a substantial fleet of specialized ASIC miners—including Antminer models (L7, L9, and DG1+)—with precise strategies tailored for each asset and mining algorithm (e.g., SHA-256, Scrypt, kHeavyHash).

Mined crypto assets will be promptly converted to fiat or stablecoins rather than held for extended periods, aligning with a risk-averse strategy to mitigate price volatility. This conversion-focused approach supports compliance with accounting standards under ASC 350-60, where crypto assets are measured at fair value, and helps avoid classification issues under securities regulations. The typical holding period for mined assets is expected to be brief, not exceeding a period of up to two weeks from the receipt of mined crypto assets. This short duration minimizes exposure to market fluctuations and facilitates rapid liquidity. USD proceeds from converting mined digital assets typically vary from the spot value at receipt due to market movement and execution effects. Based on current experience, this variance is typically under approximately 3.0%, but may be higher or lower and is not a fee, cap or guarantee. OpCo may use automated conversion protocols to minimize exposure to short-term price swings. While OpCo aims to mitigate volatility, there may still be short-term fluctuations between mining and conversion that could affect net proceeds.

In connection with the Merger, a nationally recognized valuation firm performed a valuation analysis on behalf of Coeptis to estimate the fair market value of OpCo’s mining operations as of January 31, 2025. On April 22, 2025, the firm completed its valuation analysis wherein it ascribed a value of approximately $660,300,000 for OpCo’s mining machine assets. The valuation was based on the assumption that all of the company’s machines are L9 application-specific integrated circuit (ASIC) miners dedicated to mining Dogecoin (DOGE). However, it should be noted that the machines are in fact L7 ASIC miners, which are utilized to mine a broader range of digital assets, including Dogecoin (DOGE) and Litecoin (LTC). Notwithstanding this clarification, no material update to the valuation report is required. Each machine is routinely optimized on-site to reach L9-equivalent performance levels through methods such as overclocking and firmware updates.

Current Market Conditions

As of April 27, 2026, DOGE and LTC were priced at $0.098985 and $55.52, respectively. OpCo expects to operate with an average energy cost of $0.088/kWh. Mining economics were analyzed using three ASIC models, with Bitmain’s L9 demonstrating the highest efficiency (0.21 J/MH) and positive profit margins under current conditions. DOGE contributes approximately 85–90% of daily mining revenue, with LTC as a secondary component. Break-even DOGE prices range from $0.086 to $0.149, depending on miner type. Sensitivity analysis shows that a 20% increase in energy prices or 10% drop in crypto prices would compress margins but leave operations with thinner-margin units like the L7 most affected.

| 4 |

Hash Rate

Hash Rate is the total computational power a miner contributes to a network. Generally speaking, higher hash rate increases the probability of successfully mining a block and receiving the associated block reward + transaction fees. Hash rate is directly correlated to revenue, only to the extent that it proportionally outpaces the network difficulty and competitors' aggregate hash rate. With respect to energy consumption, mining hardware converts electricity into hashing power. Energy usage is a function of the efficiency of the hardware (e.g., J/TH), the hash rate being maintained, and uptime (ideally 100%). Mining Costs are primarily driven by electricity costs, cooling and infrastructure, depreciation of hardware, and hosting/lease agreements. With higher hash rate, more blocks mined would be expected (assuming network difficulty remains fixed), but if network difficulty rises, the same hash rate would generate lower rewards. Similarly, if market prices for DOGE or LTC decrease, revenue in fiat terms declines despite static performance.

Energy costs are also a critical metric. Less efficient miners can become unprofitable during price compression or halving events. Margins can also be affected due to price volatility or difficulty spikes.

Dogecoin (DOGE)

Dogecoin is a decentralized, peer-to-peer cryptocurrency that was initially introduced in 2013 as a light-hearted alternative to Bitcoin. Based on the Scrypt algorithm and derived from the Litecoin codebase, Dogecoin offers relatively fast transaction times and low fees. Despite its origins as a meme-inspired digital asset, Dogecoin has gained significant popularity and adoption, driven in part by its active online community and high-profile endorsements. Dogecoin is primarily used for tipping, microtransactions, and charitable donations, though it has increasingly been integrated into select payment systems.

Litecoin (LTC)

Litecoin is a decentralized, open-source cryptocurrency launched in 2011 as one of the earliest alternatives to Bitcoin. The Litecoin network utilizes the Scrypt proof-of-work algorithm and is designed to provide faster transaction confirmation times and a different hashing algorithm than Bitcoin. Litecoin’s maximum supply is capped at 84 million coins, and it has been widely adopted for peer-to-peer transactions and as a testbed for innovations later implemented in other cryptocurrencies, such as Segregated Witness (SegWit) and the Lightning Network. Litecoin is often referred to as the “silver to Bitcoin’s gold.”

OpCo will distinguish itself within the cryptocurrency mining industry through its specialized altcoin-centric mining strategy, bolstered by extensive and proven operational experience.

Unlike most major cryptocurrency mining firms focused solely on bitcoin, OpCo will strategically mine altcoins, Dogecoin (DOGE) and Litecoin (LTC). This portfolio enables OpCo to:

| · | Maximize profitability by rapidly reallocating hash power to coins offering superior short- to medium-term ROI, especially during market fluctuations. |

| · | Reduce asset-specific risk, ensuring more balanced, stable revenue streams even during downturns or volatile market conditions. |

| · | Optimize hardware investment by deploying specialized, highly-efficient ASIC miners uniquely tailored for specific altcoin algorithms, enhancing mining profitability compared to competitors using generalized equipment. |

The Dogecoin and Litecoin networks are decentralized and do not require governmental authorities or financial institution intermediaries to create, transmit or determine the value of Dogecoin or Litecoin. Rather, Dogecoin and Litecoin are created by the Dogecoin and Litecoin network protocols through a process referred to as “mining” and the persons or machines that provide transaction verification services to the Dogecoin and Litecoin networks are rewarded with new Dogecoin and Litecoin. They are called “miners.”

| 5 |

The Dogecoin and Litecoin blockchains are a digital chain of blocks with each block containing information relating to a group of Dogecoin or Litecoin transactions. Miners validate Dogecoin and Litecoin transactions, securing the blocks and adding the blocks of transactions to the blockchain record by using computer processing power to solve complex mathematical problems. Solving the problems will result in the block being successfully added to the chain. This means that the Dogecoin or Litecoin transaction information in the block is verified and locked into the blockchain where it remains as a permanent record on the blockchain network. The record set maintained by the Dogecoin and Litecoin networks is publicly viewable and accessible to all. As an incentive to those who incur the computational cost of securing the Dogecoin and Litecoin networks by validating transactions, the miner who correctly solves the problem resulting in a block being added to the Dogecoin or Litecoin blockchain is rewarded with Dogecoin or Litecoin.

To begin Dogecoin or Litecoin mining, a user can download and run Dogecoin or Litecoin network mining software, which turns the user’s computer into a “node” on the Dogecoin or Litecoin network that validates blocks. Each block contains the details of some or all of the most recent transactions of Dogecoin and Litecoin submitted by users of the Dogecoin and Litecoin network that are not already included in prior blocks, and a transaction awarding an amount of Dogecoin and Litecoin to the miner who will add the new block. Each unique block can be solved and added to the blockchain by only one miner. Therefore, individual miners and mining pools (i.e., groups of miners acting together) on the Dogecoin and Litecoin networks are engaged in a competitive process of increasing their computing power to improve their likelihood of solving for new blocks and receiving Dogecoin or Litecoin rewards. As more miners join the Dogecoin and Litecoin networks and its collective processing power increases, the Dogecoin and Litecoin networks adjust the complexity of the block-solving equation to maintain a predetermined pace of adding a new block to the blockchain, which varies by blockchain. A miner’s proposed block is added to the blockchain once a majority of the nodes on the Dogecoin or Litecoin network confirms the miner’s work. Miners that are successful in adding a block to the blockchain are awarded Dogecoin or Litecoin for their effort and may also receive transaction fees paid by transferors whose transactions are recorded in the block. This reward system is the method by which new Dogecoin and Litecoin enter into circulation.

Performance Metrics - Network Hash Rate and Difficulty

In cryptocurrency mining, “Hash Rate” or “hashes per second” are the measuring units of the processing speed of a mining computer mining Dogecoin or Litecoin. “Hash Rate” is defined as the speed at which a computer can take any set of information and use an algorithm to reduce that information into a string of letters and numbers of a certain length, known as a “hash.” A “hash” is the computation run by mining hardware in support of the blockchain; therefore, a miner’s “Hash Rate” refers to the rate at which it is capable of solving such computations.

An individual miner has a Hash Rate measured as the total Hash Rate of all of the miners it deploys in its Dogecoin and Litecoin mining operations, and network-wide there is a total Hash Rate of all miners seeking to mine Dogecoin and Litecoin. The higher total Hash Rate of a specific miner, as a percentage of the network wide total Hash Rate, generally results over time in a corresponding higher success rate in Dogecoin and Litecoin rewards as compared to miners with lower Hash Rates. Today, network wide Hash Rates are measured in peta hashes per second, or one quadrillion (1,000,000,000,000,000) hashes per second, and exa hashes per second, or one quintillion (1,000,000,000,000,000,000) hashes per second.

“Difficulty” is a relative measure of how complex the process is made to successfully solve the algorithm and obtain a Dogecoin or Litecoin award. The difficulty is adjusted by the Dogecoin network mining software periodically generally as a function of how much hashing power is deployed by the network of miners and designed to maintain certain mining results so that, on average, one minute is required to produce a Dogecoin block. If the time to produce a block is generally exceeding the one minute expectation, which suggests that the target difficulty is set too high, the network reduces the degree of difficulty and vice versa, with this protocol called difficulty retargeting.

Mining Power Requirements

OpCo excels at leveraging dynamic power strategies, including curtailment programs and proactive adjustments based on real-time electricity pricing. This allows OpCo to operate at significantly lower and more predictable energy costs compared to competitors, creating a sustainable cost advantage.

| 6 |

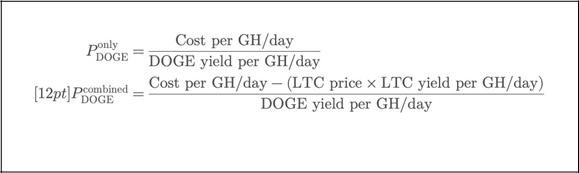

Breakeven Analysis

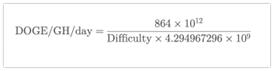

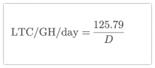

OpCo plans to operate a substantial fleet of specialized ASIC miners, including Bitmain Antminer L7, Bitmain Antminer L9, and ElphaPex DG1+ miners, all of which are specifically designed for mining Scrypt-based cryptocurrencies Dogecoin (DOGE) and Litecoin (LTC). The breakeven analysis of mining DOGE and LTC with this fleet is computed by setting the normalized power cost per (GH/s)-day, equal to merged-mining revenue per (GH/s)-day and solving for the DOGE price using contemporaneous DOGE and LTC coin yields per (GH/s)-day computed from network hashrate or difficulty.

The normalized power cost per (GH/s)-day (the “Fleet-Weighted Energy Cost”) represents the daily power cost per unit of hash rate normalized to 1 GH/s for one day, and is calculated by multiplying the total power (kW) of the fleet × 24 hours × the electricity hosting rate of $0.088/kWh, and dividing the product by the total hashrate (GH/s) of the fleet. Using this calculation and applying manufacturer-listed hashrate (GH/s) and power consumption (kW) data for the expected fleet of miners, OpCo estimates the Fleet-Weighted Energy Cost to be approximately $0.7451 per GH per day, which represents the cost of electricity required to operate 1 GH/s of hashrate for a full day.

Cost per unit of hash = (34,063 kW × 24h × 0.088 USD/kWh) / 96,555 GH/s

= $0.7451 per GH per day

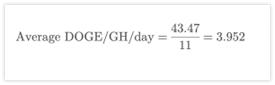

The expected merged-mining revenue (i.e. combined DOGE and Litecoin LTC coin yields per (GH/s)-day)) is computed from contemporaneous network statistics (block reward and block cadence) using network hashrate or, conversely, network difficulty. To mitigate day-to-day randomness in block discovery and to stabilize estimates for the breakeven analysis, the date range (April 18–27, 2026) is used by computing the expected coins on each day (using that day’s network hashrate or difficulty) and then averaging across the window to obtain period-average DOGE and LTC coin yields per (GH/s)-day.

DOGE has a fixed reward of 10,000 DOGE per block and targets ~1 minute per block, while LTC’s current reward is 6.25 LTC per block and targets ~2.5 minutes per block. For coins (DOGE or LTC), expected coins per (GH/s) per day are calculated by multiplying the blocks per day by the coins per block, and dividing by the network hashrate in GH/s using the network hashrate method:

Network hashrate method:

Network difficulty method:

| 7 |

| Network Hashrate Method | Network Difficulty Method |

|

5.0979 DOGE per (GH/s)-day |

5.0979 DOGE per (GH/s)-day |

|

0.001448 LTC/GH/day (average)

|

0.001448 LTC/GH/day (average) |

Independently, the difficulty method over the same window yields ≈ 5.0979 DOGE and ≈ 0.001448 LTC coins per (GH/s)-day.

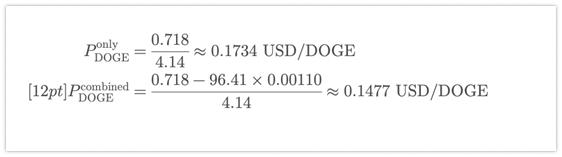

Using the April 18–27, 2026 window and LTC at $55.52, with a fleet-weighted energy cost of $0.7451 USD per (GH/s)-day, the DOGE breakeven prices are approximately 0.1462 USD/DOGE (DOGE-only) and 0.1304 USD/DOGE when crediting LTC at $55.52 per LTC.

| DOGE-only: |  |

| 8 |

DOGE with LTC credit at LTC $55.52 (April 27, 2026 close): |

|

The breakeven price of merged mining is influenced primarily by two factors: (i) the cost of electricity and (ii) the global hashrate of the Dogecoin/Litecoin networks. The breakeven analysis is an operational metric. and the estimated breakeven amounts assume that the electricity and hosting rate of $0.088/kWh under the Master Services Agreement with Minting Dome remains constant. While direct operational costs, such as electricity and hosting, are considered, the breakeven analysis also assumes continuous operation of the miners on a 24 hours/day, 7 days/week basis; and excludes pool fees and transaction fees, setup costs, maintenance, insurance, repairs, and other necessary costs and expenses of OpCo.

By equating the Fleet-Weighted Energy Cost to the expected merged-mining revenue (per unit of hash rate derived from contemporaneous network hashrates, block times, and block rewards), OpCo arrived at the breakeven point for the price per DOGE when considering Dogecoin yields alone, as well as the price per DOGE when including the offsetting value of Litecoin produced through merged mining. Therefore, if OpCo mines DOGE at the same price, it would achieve a breakeven.

| Inputs from April 18-27, 2026 | |

| LTC Price (as of April 27, 2026) | $55.52 |

| Total Power (kW) of miner fleet | 34,063 |

| Total Hashrate (GH/s) of miner fleet | 96,555 |

| DOGE Yield Average | 5.0979 DOGE coins per (GH/s)-day |

| LTC Yield Average | 0.001448 LTC coins per (GH/s)-day |

| Breakeven (DOGE only) | 0.1462 USD |

| Breakeven (DOGE with LTC) | 0.1304 USD |

Digital Asset Mix

Upon commencement of OpCo’s mining operations, DOGE will contribute 85-90% of daily mining revenue, and LTC will contribute the remaining, secondary component. Using the above closing prices for DOGE and LTC on April 27, 2026, DOGE daily issuance value of 1,440 blocks per day materially exceeds LTC’s at 576 blocks per day. When both DOGE and LTC are merged-mined on Scrypt hardware, DOGE’s larger reward value accounts for the principal driver of daily revenue based on the current prices and rewards.

DOGE’s outsized revenue contribution is due in part to current network conditions. A higher LTC price or, alternatively, a lower LTC network hashrate, would increase the LTC contribution in the DOGE breakeven formula and reduce the breakeven price, which in turn would increase margins.

| 9 |

Mining Pools

OpCo intends to register and operate its mining hardware within mining pools managed by third-party mining pool operators, each of whom ranks among the top five largest global mining pool operators for Dogecoin and Litecoin, such as EMCD, Antpool and ViaBTC. OpCo will contribute its hash rate to one or more global mining pools operated by the third-party mining pool operators, subject to their terms of service. In simple terms, the mining pool operator calculates and pays miners, such as OpCo, their share of the reward, which is a function of: (a) the miners’ actual hash rate contributed and (b) global network difficulty. The operator pays the miners (e.g. OpCo) in arrears for their mathematically calculated share of global block rewards (net of fees to the operator) plus our share of global transaction fees.

Each mining pool operator maintains different fee structures and reward methods for different coins, which are subject to change. The fee charged by each mining pool operator varies and is subject to change. OpCo expects fees to vary in an amount up to 4%.

Mining Pool Service Agreements

OpCo intends to “sign-up” with the mining pool operators on-line according to pre-arranged parameters, whereby OpCo’s hash rates are added to the pool in exchange for a ratable share of the pool’s Rewards based on the hash rate contributed by OpCo. The service agreements entered into with each mining pool operator are standard and typically commence as of the date of registration of a user account and continue for the lifetime of such account, under which the user undertakes to provide computing power in exchange for the cryptocurrencies mined, which are governed by and subject to the operator’s published online terms of use/service.

Mining Pool Verification of Rewards

In exchange for providing computing power, which represents OpCo’s performance obligation, OpCo would be entitled to non-cash consideration in the form of cryptocurrency, calculated under one of two payout methods, depending on the coin mined and the reward system used by the mining pool operator to distribute mining rewards. For example, the EMCD pool operates on the PPS+ and PPLNS models for Litecoin and Dogecoin, respectively. In the PPLNS (or Pay-Per-Last-N-Shares) reward distribution method, rewards depends on: (1) the mining pool’s luck in finding a block — the reward will only be paid if the pool finds blocks during a specific period (if the pool finds more blocks, the miners receive a higher reward); and (2) The number (N) of the last shares the miners’ equipment contributed to the pool — miners who worked longer during the period will receive higher rewards compared to those with short-term connections.

Rewards under PPS+ (or Pay Per Share Plus) reward method depend on the number of shares sent by the miners’ equipment (as in PPS) and the pool's luck in finding the block — in this case the miners get an additional reward if the pool finds a block (as in PPLNS). The higher the luck, the more blocks the pool will find, and the more additional rewards the miners get. OpCo will use dashboard metrics provided by the mining pool operator and blockchain explorers to calculate/verify its share of rewards received. Online agreements with each mining pool operator define payout terms, fees, and operational obligations, and are publicly available on each operator’s website.

Key Storage

Anchorage Digital employs a sophisticated Multi-Party Computation (MPC) with quorum requirements and multiple signors, as confirmed by OpCo's usage. This architecture provides the following security features:

Hardware Security Module (HSM) Integration

Anchorage Digital utilizes FIPS 140-2 certified hardware security modules that keep private key material completely offline within air-gapped hardware while enabling real-time transaction processing. The HSMs perform independent verification of transaction instructions and organizational policies before authorizing any asset movement.

| 10 |

Multi-Party Computation Framework:

The MPC system ensures that private keys never exist in complete form at any location or time. Key shares are distributed across multiple secure environments, with threshold signatures requiring a predetermined quorum for transaction authorization. This eliminates single points of failure inherent in traditional custody models.

Quorum-Based Authorization:

Anchorage Digital's policy engine validates that transactions meet organizational policies through cryptographic signatures from multiple hardware devices. The system requires biometric voice and video transaction approval from authorized users, with cryptographically signed instructions endorsing source, destination, currency, and amount.

Geographic and Access Controls:

Anchorage Digital maintains geographically distributed infrastructure with strict physical access controls meeting ISO 13491-2 and other security standards. The system provides proof of exclusive control and auditable records for compliance purposes.

Insurance

OpCo will maintain insurance with Anchorage Digital. The insurance policy covers digital assets throughout their life cycle, addressing gaps that typically exist in crypto custody insurance. Anchorage Digital maintains an aggregate $100 million commercial crime insurance policy that provides coverage for certain losses due to theft, robbery, burglary, as well as third-party computer and funds transfer fraud. This coverage applies to assets at all times when held at Anchorage Digital Bank, with no distinction between hot and cold storage, and provides comprehensive “end-to-end” insurance coverage not typically available at other custodians whose insurance coverage applies only to cold storage. As a federally chartered bank, Anchorage Digital’s insurance arrangements are subject to federal banking oversight, providing additional assurance of coverage adequacy and claims-paying ability. Digital assets held in custody by Anchorage Digital, however, are not guaranteed by Anchorage Digital and are not subject to the insurance protections of the Federal Deposit Insurance Corporation (FDIC).

Material Agreements

Master Services Agreement with Minting Dome

OpCo is party to a Master Services Agreement (“MSA”) with Minting Dome, a leading provider of digital asset infrastructure and tokenization services. Minting Dome provides technical and operational support for the issuance, management, and lifecycle services of digital assets and tokens related to OpCo’s blockchain initiatives, specifically, the optimized, multi-asset digital mining of Dogecoin and Litecoin. Pursuant to the MSA, Minting Dome hosts sites/locations whereby it provides electrical power at $0.088 per KWh, internet access, and connection equipment necessary for the operation of OpCo’s ASIC miners. Following the installation of OpCo’s ASIC miners, Minting Dome provides (i) management services, including remote monitoring to oversee the uptime of the ASIC miners and to facilitate repairs, (ii) on-site personnel to rack, set-up and de-rack the ASIC miners, and (iii) operation and maintenance of the ASIC miners in accordance with industry standards. The MSA provides that Minting Dome is the exclusive provider of these services to OpCo.

The agreement sets forth key terms including service level commitments, data security obligations, confidentiality and intellectual property rights. OpCo pays certain delivery and installation, logistics coordination, repair services, racking and de-racking, and hosting and management services fees.

The MSA became effective at the Effective Time and is structured with an initial term of three (3) years, with automatic renewal provisions unless terminated by either party in accordance with the agreement’s terms.

| 11 |

Master Services Agreement with Anchorage Digital

OpCo has also entered into a Master Custody Services Agreement (the “Custody Agreement”) with Anchorage Digital, a regulated digital asset custodian and infrastructure provider. Under the terms of the Custody Agreement, Anchorage Digital will act as custodian of OpCo’s digital assets deposited with Anchorage Digital. Anchorage Digital will provide services through its technology platform, which include: (i) the storage of OpCo’s digital assets, specifically, Dogecoin and Litecoin, (ii) handling and settlement of digital assets pursuant to OpCo’s authenticated instructions, and (iii) determining the eligibility of digital assets for continued storage. Anchorage Digital also provides support services, such as access to representatives for account management and, if needed, lock-up support services to restrict withdrawals and transfers from OpCo’s accounts with Anchorage Digital. Further, Anchorage Digital may, in its sole discretion, offer on-chain services to OpCo that include staking, voting, vesting, signaling, and other activities involving interaction with the blockchain underlying the Dogecoin and Litecoin digital assets. The Custody Agreement governs custody services only and does not provide for conversion services. Any conversion services, if utilized, would be provided under a separate arrangement with an Anchorage Digital affiliate or through third-party providers.

In consideration for Anchorage Digital providing the preceding services, OpCo will pay to Anchorage Digital fees depending on the Assets Under Custody (“AUC”) tier, ranging from 35 annual basis points (“Annual Basis Points”) for AUC under $10 million to 15 Annual Basis Points for AUC greater than $500 million. The Custody Agreement includes provisions related to security protocols, regulatory compliance, indemnification, and fees. Anchorage Digital does not have the authority to assign, hypothecate, pledge, encumber or otherwise dispose of OpCo’s digital assets. The Custody Agreement became effective on August 14, 2025 for an initial term of one year and will automatically renew for a renewal term of one year following the initial term unless terminated in accordance with its terms. While the Custody Agreement is currently effective, OpCo will begin using Anchorage Digital’s custodian services in full under the Custody Agreement following the Effective Date and concurrently with the commencement of OpCo’s business operations. Anchorage Digital’s services support OpCo’s commitment to operating in a secure and compliant digital asset environment.

Amended and Restated Asset-For-Share Exchange Agreement

Concurrently and in connection with the closing of the Merger Transaction, OpCo acquired operational mining computer assets comprised of 8,228 Bitmain Antminer L7 units, 849 Bitmain Antminer L9 units and 723 ElphaPex DG1+ units from BSG Series CM in exchange for 44,062,947 shares of OpCo Common Stock issued to BSG Series CM at a cost basis of $16.31 per share pursuant to an Asset-For-Share Exchange Agreement (as amended by the First Amendment to the Amended and Restated Asset-For-Share Exchange Agreement dated February 10, 2026, and the Second Amendment to the Amended and Restated Asset-For-Share Exchange Agreement dated April 23, 2026, the “Asset-For-Share Exchange Agreement”). The shares will be issued to BSG Series CM pursuant to an exemption from registration under the Securities Act. The Asset-For-Share Exchange Agreement was consummated concurrently with the Merger Transaction with the representations and warranties of OpCo and BSG Series CM surviving, along with the following share transfer restrictions.

Pursuant to the Asset-For-Share Exchange Agreement, BSG Series CM agreed to not sell, dispose of, or otherwise transfer the shares received from OpCo unless the volume-weighted average price of OpCo’s Common Stock over the ten (10) consecutive days immediately prior to the proposed sale date is greater than $16.31 per share. BSG Series CM further agreed that, commencing on the date on which OpCo’s Common Stock becomes publicly traded on a national securities exchange or recognized over-the-counter market, and continuing for a period of eighteen (18) months thereafter, BSG Series CM and each transferee of OpCo Common Stock transferred from BSG Series CM will not sell more than one-eighteenth of the total number of OpCo shares beneficially owned by it in any calendar month, not engage in any short selling, or sales that exceed five percent (5%) of the average daily trading volume of OpCo’s Common Stock over the ten (10) trading days immediately preceding such sale. Notwithstanding the lock-up and leak-out restrictions, BSG Series CM may sell OpCo Common Stock if the publicly quoted closing price exceeds $35.00 per share for any two (2) consecutive trading days. These restrictions also apply to any transferees of the shares held by BSG Series CM.

| 12 |

Competition

The digital asset mining industry is intensely competitive and rapidly evolving. We face competition from a range of companies that are well-capitalized, technologically advanced, and geographically diversified. These competitors include public and private entities that operate large-scale mining operations and infrastructure, many of which have significant access to renewable and low-cost energy sources.

Our competitors have invested heavily in purpose-built facilities, state-of-the-art mining hardware, and proprietary software to optimize operational efficiency. Several of these companies emphasize sustainability and environmental responsibility by sourcing energy from low-carbon or renewable sources, including hydroelectric, solar, wind, nuclear, and captured methane. Some are vertically integrated, managing everything from equipment procurement to facility operations, and are actively developing multi-gigawatt mining campuses powered by renewable energy.

Additionally, some competitors have global footprints, with operations spanning North America, the Middle East, Europe, and Asia. These companies benefit from economies of scale, strategic energy partnerships, and favorable regulatory environments in certain jurisdictions. Others support the decentralization of mining by providing institutional mining services, equipment financing, and large-scale mining pool operations.

The market also includes entities that have recently diversified into mining new proof-of-work digital assets beyond bitcoin, further increasing competition for infrastructure and capital. In this dynamic environment, we compete primarily on the basis of energy cost, access to capital, mining efficiency, facility uptime, regulatory compliance, and environmental stewardship.

While we believe our strategic positioning, technological capabilities, and commitment to sustainable practices offer significant competitive advantages, there is no assurance that we will be able to compete successfully against current or future industry participants.

Competitive Advantages

OpCo will distinguish itself in the cryptocurrency mining industry through a unique altcoin-focused strategy, deep operational expertise, and agile infrastructure management. Unlike many of its peers that concentrate exclusively on bitcoin mining, OpCo will strategically balance its operations with altcoins, Dogecoin (DOGE) and Litecoin (LTC). This altcoin-centric approach enables OpCo to dynamically reallocate hash power to assets offering superior short- to medium-term returns, particularly during periods of market volatility. The result is a more resilient and balanced revenue profile, mitigating asset-specific risk and maximizing capital efficiency. OpCo will also deploy specialized ASIC hardware tailored to the unique algorithms of these altcoins, allowing for greater mining efficiency than firms reliant on generalized mining equipment.

OpCo’s leadership team brings a track record of success in cryptocurrency mining, marked by sophisticated logistics, infrastructure optimization, and economic discipline. Michelle Burke, Chief Operating Officer of OpCo, is experienced in directing strategic vision, financial oversight and daily operations for a successful crypto mining operation from her roles as Chief Executive Officer of Minting Dome and Chief Operating Officer of Wattum Management. OpCo will excel in the full lifecycle management of its mining assets, supported by advanced repair systems, component reclamation processes, and techniques that extend hardware longevity. These practices minimize downtime, reduce capital expenditure, and lower environmental impact. OpCo’s real-time analytics infrastructure will enable precise, data-driven decision-making at both strategic and operational levels, ensuring sustained performance optimization across its fleet.

Operational agility is another key differentiator. OpCo will use Minting Dome’s hosting facility network to swiftly redeploy mining equipment across facilities to capitalize on favorable electricity rates, regulatory conditions, or other operational efficiencies. This flexibility allows OpCo to adapt more quickly than many of its competitors in an ever-evolving industry. Additionally, OpCo will leverage dynamic power management strategies, including curtailment programs and real-time electricity pricing models, to significantly reduce and stabilize energy costs - one of the most critical inputs in cryptocurrency mining.

Finally, OpCo’s distributed, facility-agnostic infrastructure reduces exposure to localized disruptions such as regulatory shifts or grid instability. This structure not only enhances operational resilience but also supports rapid scalability into new geographies and emerging technologies, providing OpCo with long-term strategic advantage.

| 13 |

Operational Strategy

OpCo employs a lean, data-driven, and asset-optimized operational strategy designed to maximize returns from digital assets, namely Dogecoin and Litecoin. Rather than focusing solely on scale, OpCo emphasizes operational flexibility, lifecycle efficiency, and precision execution to sustain competitive mining performance. Central to this approach is OpCo’s altcoin opportunism strategy, which will target assets such as Dogecoin and Litecoin-cryptocurrencies offering favorable short- to mid-term return potential. By deploying highly specialized ASIC miners tailored to these alternative algorithms, OpCo will be able to unlock greater efficiency and profit margins than firms focused exclusively on bitcoin.

OpCo’s hash power management will be continuously informed by real-time analysis of market trends, network difficulty, and token-specific profitability. This enables dynamic reallocation of mining resources to optimize returns as market conditions evolve. Operations are distributed across multiple third-party and partner-owned facilities in a facility-agnostic structure. This approach avoids over-reliance on any single hosting provider and supports agile relocation of equipment based on shifting power costs, infrastructure readiness, and uptime performance.

OpCo will implement comprehensive, end-to-end equipment lifecycle management to protect and extend the value of its mining assets. Each unit is tracked from deployment through repair and eventual retirement. A structured spare parts and reclamation system enables OpCo to extract usable components from decommissioned equipment, while in-house repair coordination reduces downtime and minimizes capital expenditure.

Operational decisions are grounded in real-time analytics integrated through centralized dashboards, aggregating data from mining pools, facility APIs, and internal sensors. This infrastructure will enable daily monitoring of unit-level Hash Rate, energy consumption, and profitability. The data is used to proactively detect underperformance, identify facility issues, and ensure energy efficiency across the fleet.

OpCo will also manage energy costs through a responsive curtailment strategy. It proactively adapts operations to curtailment schedules, seasonal rate fluctuations, and electricity market conditions-throttling or shifting activity to preserve profitability during high-cost periods. Facility-level downtime is analyzed and categorized to distinguish between voluntary curtailment, forced outages, and repair-related downtime.

A core component of OpCo’s future success will lie in its asset agility and logistical precision. Standard operating procedures govern the decommissioning, repair, and inventory management of hardware. On-the-ground personnel oversee installations, PDU swaps, and physical control of mining units. Every piece of equipment will be tracked via serial number and shipping records to maintain accountability and prevent loss during transfers or facility moves.

Rather than pursuing scale for its own sake, OpCo’s growth philosophy centers on sustainable efficiency. OpCo will avoid overleveraging and remain focused on optimizing hardware, adapting to network shifts, and positioning itself to capitalize on emerging asset classes. This operational discipline enables OpCo to scale effectively and profitably within an increasingly competitive mining ecosystem.

Intellectual Property

OpCo holds no patents, copyrights, trademarks, or licensing agreements.

| 14 |

Government Regulation

Government regulation of digital assets, including cryptocurrency, and blockchain technology is being actively considered by the United States federal government via a number of agencies and regulatory bodies, as well as similar entities in other countries. State government regulations also may apply to OpCo’s mining activities and other related activities in which OpCo participates or may participate in the future. Certain regulatory bodies have shown an interest in regulating or investigating companies engaged in the blockchain technology or business.

In addition, because transactions in cryptocurrency provide varying degrees of anonymity, they are susceptible to misuse for criminal activities, such as money laundering. This misuse, or the perception of such misuse (even if untrue), could lead to greater regulatory oversight of cryptocurrency platforms, and there is the possibility that law enforcement agencies could close cryptocurrency platforms or other crypto-related infrastructure with little or no notice and prevent users from accessing or retrieving cryptocurrency held via such platforms or infrastructure.

Multiple United States federal agencies and regulators have been active in rulemaking, issuing guidance and regulating various actors in the blockchain technology industry, including the CFTC, SEC, FINRA, OCC, CFPB, FinCEN, OFAC, IRS, FDIC, and Federal Reserve. In response to these events, the digital asset markets have experienced extreme price volatility. As the regulatory and legal environment evolves, OpCo may become subject to new laws, further regulation by the SEC, and other federal or state agencies, which may affect OpCo’s Dogecoin and Litecoin mining and other related activities. Certain state and local authorities have introduced and passed legislation that may affect OpCo’s business and the business of crypto mining.

For additional discussion regarding OpCo’s belief about the potential risks existing and future regulations pose to OpCo’s business, see “Risk Factors” herein.

Environmental Considerations

OpCo is aware that energy consumption is both a principal cost driver and a key environmental consideration within the cryptocurrency mining industry. As part of its commitment to sustainable operations, OpCo integrates energy efficiency and environmental responsibility into its facility selection, operational planning, and equipment lifecycle strategies.

Electricity represents the largest variable expense in OpCo’s future mining operations. OpCo will continuously monitor power pricing at each hosting facility, including $/kWh rates, time-of-use pricing structures, and peak-hour penalties. By leveraging real-time Hash Rate analytics, OpCo dynamically adjusts its mining loads to reduce operational intensity during periods of elevated energy costs or utility curtailment events, thereby optimizing profitability while minimizing environmental strain.

Facility selection is strategically driven by energy profile considerations. OpCo will partner exclusively with hosting providers that offer competitive long-term power agreements and infrastructure capable of efficiently supporting high-density ASIC hardware. This ensures not only cost-effective operations but also the use of stable, grid-compliant energy solutions with lower transmission losses.

As part of its sustainability initiative, OpCo will employ a comprehensive equipment lifecycle management strategy focused on waste minimization and resource efficiency. OpCo will actively reuse functional hardware components—such as hash boards, control boards, and cooling fans—and work with certified e-waste recyclers to responsibly dispose of non-repairable units. These practices reduce the volume of electronic waste and limit demand for new raw materials by extending the operational lifespan of mining equipment through repair and parts reclamation.

OpCo will also participate in structured energy curtailment programs offered by its hosting partners, such as Duke Energy’s PowerShare initiative in North Carolina. These programs typically involve 2–3 curtailment periods per year, most often during peak demand times such as extreme heat or cold. The maximum curtailment period is up to 8 hours per event, though the duration is typically 4–5 hours. During a curtailment event, the mining facility does not shut down operations entirely. Instead, demand load levels are reduced, allowing mining machines to temporarily idle (“sleep”) while cooling fans continue to run. This approach reduces stress on hardware and enables the facility to resume full operations quickly after the curtailment ends. Because there are 8,760 potential operating hours in a year, and curtailment is expected to total no more than approximately 24 hours annually, the impact represents roughly 0.3% of total operating time. As a result, curtailment is not expected to materially reduce OpCo’s overall mining capacity or hash power.

| 15 |

OpCo’s equipment procurement decisions will prioritize energy efficiency over raw Hash Rate. It favors next-generation miners with superior joules-per-terahash (J/TH) performance, including models such as the L9 for Scrypt-based assets with favorable energy profiles. Each hardware purchase is evaluated based on projected energy return on investment (EROI), ensuring that equipment decisions support both economic performance and environmental responsibility.

Through these integrated measures, OpCo seeks to maintain operational excellence while reducing its environmental impact and contributing to the long-term sustainability of the digital asset mining ecosystem.

Legal Proceedings

OpCo may become engaged, in litigation in the ordinary course of business. Subject to the inherent uncertainties of litigation and although no assurances are possible, we believe that there are no pending lawsuits or claims that, individually or in the aggregate, will have a material adverse effect on our business, financial condition or our results of operations.

OpCo is party to the Asset-For-Share Exchange Agreement with BSG Series CM, LLC (“BSG Series CM”), an entity currently named as a defendant in ongoing litigation initiated by the Securities and Exchange Commission involving allegations of misconduct related to certain investment activities. BSG Series CM is subject to regulatory monitoring and oversight pursuant to court orders issued in connection with this litigation. While OpCo is not a party to the litigation, it acknowledges that its contractual relationship with BSG Series CM may expose it to certain reputational and operational risks associated with the ongoing legal proceedings and monitoring.

Planned Business Operations Following the Merger Transaction

OpCo’s planned business operations over the next 12 months center on deploying and activating its fleet of approximately 9,800 ASIC miners across multiple hosting sites in the United States, while simultaneously laying the groundwork for infrastructure and product-oriented initiatives that support long-term scalability.

Q1 2026 Operational Plan:

Upon closing, OpCo expects to initiate the following critical operational steps:

| · | Execute hosting agreements and energize facilities in multiple states |

| · | Install approximately 9,000 ASIC units across hosting sites |

| · | Inventory and document all OpCo assets |

| · | Link all operational machines to the selected mining pool(s) |

| · | Establish daily miner health monitoring protocols and uptime reporting |

| · | Investigate a strategy for adding additional ASIC units to the fleet as sourcing opportunities arise |

| · | Finalize remote management processes for real-time visibility |

These deployments are expected to occur in a staged rollout, with full activation of the fleet targeted by the end of Q2 2026.

| 16 |

Q2 2026 Strategic Development Focus:

In parallel with core mining operations, OpCo has begun evaluating and planning for additional revenue-generating opportunities that align with its infrastructure, existing asset base, and market expertise. These early-stage initiatives are subject to feasibility review, partner discussions, and technical assessment before any capital-intensive implementation occurs. Planned areas of focus include potential retail-facing services, and risk mitigation strategies related to evolving consensus models within the Dogecoin ecosystem.

Funding Requirements and Implementation Plan:

OpCo intends to fund its near-term operations through a near term equity financing. The anticipated use of proceeds includes fleet activation, hosting contracts, infrastructure installation, system monitoring, and foundational support functions. The company believes the combined post-merger structure provides a strong platform for capital formation. There is no assurance, however, that the required funding will be provided through equity financing or another source. Any delay in funding or lack thereof will delay the implementation of our business strategy and may cause the company to consider strategic alternatives, including debt financing or reorganization of the company.

Spin-Out of Coeptis Legacy Assets

On April 15, 2026, Coeptis undertook a reorganization of its assets related to its biopharmaceutical operations (other than its assets with respect to GEAR Therapeutics, Inc.) to reorganize such assets to be held directly or indirectly by a new subsidiary Coeptis Holdings, Inc (“CHI”). Specifically, and in connection therewith, Coeptis entered into two assignment and assumption agreements and a contribution agreement pursuant to which substantially all of such assets and liabilities were assigned or contributed to CHI, in exchange for the issuance to Coeptis of a 100% ownership interest in CHI (the “Spin Out”). Further, as of immediately prior to the consummation of the Merger, Coeptis declared a one-for-one pro rata dividend of its ownership interest in CHI to the stockholders of Coeptis existing as of January 2, 2026 (the record date for Coeptis’ most recent shareholder meeting).

In connection with the Spin Out, Coeptis spun out its biopharmaceutical operations, other than those conducted through GEAR Therapeutics, Inc. In exchange for Coeptis keeping in its organization, on a post-Merger basis, its subsidiary GEAR Therapeutics, Inc, Coeptis issued to CHI 1,000,000 shares of Coeptis’ common stock and executed and delivered to CHI an option agreement that grants CHI a limited time option exercisable in its discretion to acquire GEAR Therapeutics, Inc. for the fair market value of GEAR Therapeutics, Inc. at the time of exercise. The option becomes exercisable on October 24, 2026, is exercisable for a period of twenty-four (24) months from the date on which such option becomes exercisable, and contemplates that the exercise price for the option may be paid at the option of CHI in cash, by return of shares of Coeptis common stock based on the value of the Coeptis common stock at the time of exercise of the option, or a combination thereof. The GEAR Therapeutics, Inc. retained operations are not material to OpCo’s continuing business strategy, and OpCo does not currently intend to make additional investments in or further pursue such legacy business line.

| 17 |

RISK FACTORS AND SPECIAL CONSIDERATIONS

You should carefully consider all the following risk factors, together with all of the other information in this Current Report, including the financial information. We operate in a highly competitive and highly regulated business environment. Our business can be expected to be affected by government regulation, economic, political and social conditions, business’ response to new and existing products and services, technological developments and the ability to obtain and maintain patent and/or other intellectual property protection. Our actual results could differ materially from management’s expectations because of changes both within and outside of our control. Due to such uncertainties and the risk factors set forth in this Current Report, prospective investors are cautioned not to place undue reliance upon such forward-looking statements.

Throughout this section, references to “we,” “us,” “our,” and “the company” refer to Pubco and its consolidated subsidiaries as the context so requires.

This Report contains forward-looking statements. Information provided in this Current Report may contain forward-looking statements which reflect management’s current view with respect to future events, the viability or efficacy of our products and our future performance. Such forward-looking statements may include projections with respect to market size and acceptance, revenues and earnings, marketing and strategies and business operations.

Risks Related to Our Business

General Risks

OpCo is an early-stage company and has a limited history of generating profits.

OpCo was formed out of a shell company formed in December 2022, and has a limited history upon which an evaluation of OpCo’s performance and future prospects can be made. OpCo anticipates mining operations to begin in Q2 2026, and had no previous existing operations. OpCo’s current and proposed operations are subject to all of the business risks associated with new enterprises. These include likely fluctuations in operating results as OpCo reacts to developments in its market, manages its growth and operations, and responds to the entry of competitors into the market. Further, there is no assurance that OpCo can successfully execute its business plan. OpCo has had limited revenues generated.

Pubco may be unable to access sufficient additional capital to fund its operations or for future strategic growth initiatives.

OpCo’s purchase of its fleet of Dogecoin and Litecoin miners was a capital intensive project, and OpCo anticipates that future strategic growth initiatives will likewise be capital-intensive. If Pubco raises capital through public or private equity offerings, the ownership interest of Pubco’s existing stockholders will be diluted, and the terms of these securities may include liquidation or other preferences that adversely affect Pubco’s stockholders’ rights. If Pubco raises capital through debt financing, Pubco may be subject to covenants limiting or restricting Pubco’s ability to take specific actions, such as incurring additional debt or liens, making capital expenditures or declaring dividends. Further, Pubco may be unable to raise capital in a timely manner, in sufficient quantities, or on terms acceptable to Pubco, if at all. If Pubco is unable to raise the capital needed to fund its operations or execute future strategic growth initiatives, Pubco may be less competitive in its industry and its results of operations and financial condition may suffer. The value of its securities may also be materially and adversely affected.

Pubco’s loss of any of its management or advisory team, its inability to execute an effective succession plan, or its inability to attract and retain qualified personnel, could adversely affect Pubco’s business.

Pubco’s success and future growth will depend to a significant degree on the skills and services of its management and advisors, including David Halabu, Pubco’s Chief Executive Officer and President. Pubco will need to continue to grow its management in order to alleviate pressure on its existing team and in order to continue to develop its business. If Pubco’s management, including any new hires that Pubco may make, fail to work together effectively and to execute Pubco’s plans and strategies on a timely basis, Pubco’s business could be harmed. Furthermore, if Pubco fails to execute an effective contingency or succession plan with the loss of any member of management, the loss of such management personnel may significantly disrupt its business.

| 18 |

The loss of key members of management or advisory team could inhibit Pubco’s growth prospects. Pubco’s future success also depends in large part on its ability to attract, retain and motivate key management and operating personnel. As Pubco continues to develop and expand its operations, it may require personnel with different skills and experiences, and who have sound understandings of OpCo’s business and the Dogecoin and Litecoin network industry. The market for highly qualified personnel in this industry is very competitive, and Pubco may be unable to attract such personnel. If Pubco is unable to attract such personnel, its business could be harmed.

There is a substantial doubt about our ability to continue as a going concern.

The report of our independent registered public accounting firm that accompanies our consolidated financial statements includes an explanatory paragraph indicating there is a substantial doubt about our ability to continue as a going concern, citing our need for additional capital for the future planned expansion of our activities and to service our ordinary course activities (which may include servicing of indebtedness). The inclusion of a going concern explanatory paragraph in the report of our independent registered public accounting firm will make it more difficult for us to secure additional financing or enter into strategic relationships on terms acceptable to us, if at all, and likely will materially and adversely affect the terms of any financing that we might obtain. Our consolidated financial statements do not include any adjustments that may result from the outcome of this uncertainty.

We have incurred significant losses in prior periods, and losses in the future could cause the quoted price of our Common Stock to decline or have a material adverse effect on our financial condition, our ability to pay its debts as they become due, and on its cash flows.

For the year ended December 31, 2025, we incurred a net loss of $12,277,192 and, as of that date, we had an accumulated deficit of $109,953,728. For the year ended December 31, 2024, we incurred a net loss of $10,877,412 and, as of that date, had an accumulated deficit of $98,233,673. Any losses in the future could cause the quoted price of our Common Stock to decline or have a material adverse effect on our financial condition, its ability to pay its debts as they become due, and on its cash flows.

To date, we have generated only minimal revenue. We expect that our planned product development and strategic expansion pursuits will increase losses significantly over the next five years. In order to achieve profitability, we will be required to generate significant revenue. We cannot be certain that we will generate sufficient revenue to achieve profitability. We anticipate that we will continue to generate operating losses and experience negative cash flow from operations at least through the first quarter of 2026 or longer. We cannot be certain that we will ever achieve profitability or that, if profitability is achieved, that is will be maintained. If our revenue grows at a slower rate than we anticipate or if our product development, marketing and operating expenses exceed our expectations or cannot be adjusted accordingly, our business, results of operation and financial condition will be materially adversely affected and we may be unable to continue operations.

We expect that we will need to rely on key third-party agreements, in order to be in a position to realize material revenues in the future, and we may never enter into any such agreements or realize material, ongoing future revenue. Even if we eventually generate revenues, we may never be profitable, and, if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis.

If we are unable to manage future expansion effectively, our business may be adversely impacted.

In the future, we may experience rapid growth in our business, which could place a significant strain on our operations, in general, and our internal controls and other managerial, operating and financial resources, in particular. If we are unable to manage future expansion effectively, our business would be harmed. There is, of course, no assurance that we will enjoy rapid development in our business.

If we are unable to recruit and retain key personnel, our business may be harmed.

If we are unable to attract and retain key personnel, our business may be harmed. Our failure to enable the effective transfer of knowledge and facilitate smooth transitions with regard to our key employees could adversely affect our long-term strategic planning and execution.

| 19 |

Our business plan is not based on independent market studies.

We have not commissioned any independent market studies concerning our business plans. Rather, our plans for implementing our business strategy and achieving profitability are based on the experience, judgment and assumptions of our management. If these assumptions prove to be incorrect, we may not be successful in our business operations.

Our Board of Directors may change our policies without shareholder approval.